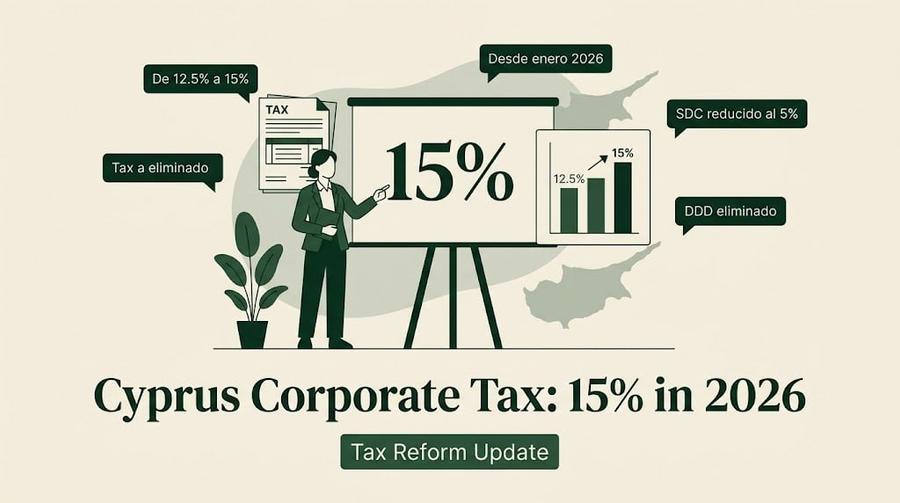

Cyprus Corporate Tax 15% in 2026: What Changed

The Cyprus Parliament approved a comprehensive tax reform package on 22 December 2025, raising the corporate income tax rate from 12.5% to 15% for all Cyprus-resident companies. The new rate applies to fiscal years beginning on or after 1 January 2026.

What Changed and When

For fiscal years ending before 31 December 2025, the headline corporate tax rate remains 12.5%. Companies with a calendar year fiscal period will first pay the 15% rate on their 2026 income, when they file their 2026 tax return.

The rate increase is not solely a Pillar Two requirement. Large multinational groups with global consolidated revenues above EUR 750 million were already subject to a separate Domestic Minimum Top-Up Tax (DMTT) effective from 2025. The 15% headline rate now applies to all Cyprus-resident companies regardless of size.

What Else Changed in the Reform Package

The December 2025 legislation introduced several additional changes:

- The Special Defence Contribution (SDC) on actual dividend distributions drops from 17% to 5% for distributions paid from profits earned from 1 January 2026.

- The Deemed Dividend Distribution (DDD) mechanism, which previously imposed SDC on undistributed profits retained over two years, is abolished for periods from 2026 onwards.

- Stamp duty is abolished on most commercial transactions.

- The carry-forward period for tax losses is extended from 5 to 7 years.

- The 120% R&D super-deduction is extended until 31 December 2030.

What Stays the Same

The reform preserved Cyprus's core tax advantages:

- The IP Box regime remains operational. The effective rate moves from 2.5% to 3% as a mechanical result of the higher headline rate - the underlying 80% notional deduction is unchanged.

- The Notional Interest Deduction (NID) on new equity contributions is unchanged.

- The participation exemption on dividends from EU-resident subsidiaries is unchanged.

- Non-Dom status for individual shareholders is unchanged. Dividends to Non-Dom shareholders remain exempt from SDC.

What This Means in Practice

A standard Cyprus trading company with EUR 500,000 of taxable profit will pay EUR 75,000 in corporate tax from 2026, compared to EUR 62,500 under the old rate. For a Non-Dom shareholder, the effective combined rate on distributed profits remains approximately 5% (corporate tax plus 2.65% GESY on dividends, with SDC exempt under Non-Dom status).

Sources: KPMG Tax News Flash, EY Global Tax Alert, PwC Cyprus Tax Reform Update - all published January 2026.

![Cyprus Ltd vs Irish Ltd: Company Tax Compared [2026]](https://cdn.sanity.io/images/glqahhks/production/84e3d82538a859345d8d2447e8e097c5777fb238-1679x937.png?w=700&q=75&auto=format)

![Cyprus vs Malta Company Formation [2026]](https://cdn.sanity.io/images/glqahhks/production/97db89d0ce729a9e931d09bc1522631faa6c3474-1679x937.png?w=700&q=75&auto=format)