Moving from UK to Cyprus

Quick Answer

Moving from United Kingdom to Cyprus with Non-Dom status reduces your effective tax rate from ~42-50% to approximately 5%. Cyprus applies 0% Special Defence Contribution on foreign dividends, a flat 15% corporate tax, and offers tax residency with just 60 days of physical presence per year under the 60-day rule. A double tax treaty between United Kingdom and Cyprus prevents double taxation during the transition.

Last updated: 2026-06-17

Why United Kingdom Professionals Consider Cyprus

The United Kingdom has undergone a dramatic shift in its tax landscape for high earners. Until April 2025, the non-dom regime allowed individuals not domiciled in the UK to shelter foreign income from UK tax. That regime was abolished. UK residents are now taxed on worldwide income regardless of domicile status, making the UK one of the highest-tax environments for entrepreneurs and investors in the developed world.

The personal tax burden is severe. The basic rate is 20% on income between £12,571 and £50,270. Above £50,270, the higher rate of 40% applies. Above £125,140, the additional rate of 45% kicks in. Critically, the personal allowance (£12,570) is tapered away at £2 for every £3 earned above £100,000, creating an effective 60% marginal tax rate on income between £100,000 and £125,140.

For entrepreneurs operating through a limited company, the headline corporate tax rate is 25% for profits above £250,000. Extracting that profit as dividends then attracts dividend tax: 8.75% at the basic rate, 33.75% at the higher rate, and 39.35% at the additional rate. The £500 annual dividend allowance (reduced from £2,000 in 2022) provides negligible relief.

National Insurance adds another layer. Employees pay 8% on earnings between £12,570 and £50,270, and 2% above that. Employers pay 13.8% above £9,100, and from April 2025 this threshold drops further, increasing costs for company directors paying themselves a salary.

The combined result: a UK-based entrepreneur earning £200,000 through a Ltd company will pay approximately £75,000-85,000 in total taxes, an effective rate exceeding 40%.

London and major UK cities are among the most expensive in the world. A two-bedroom flat in London costs £2,200-£4,000 per month. Childcare is consistently ranked among the most expensive in Europe. The grey skies and high cost base have pushed increasing numbers of British entrepreneurs to seek alternatives — with Cyprus emerging as the most practical within the EU.

United Kingdom Tax Burden at a Glance

| Tax type | 🇬🇧 United Kingdom |

|---|---|

| Income tax | Up to 45% (additional rate above £125,140) |

| Corporate tax | 25% (profits >£250k) / 19% (profits <£50k) |

| Capital gains tax | 10%/20% (assets), 18%/24% (property) |

| Dividend tax | 8.75% basic / 33.75% higher / 39.35% additional |

| Social contributions | 8% NI employee (£12,570–£50,270) + 2% above; 13.8% employer |

| Effective rate | ~42-50% |

Tax Comparison: United Kingdom vs Cyprus

The contrast between the UK and Cyprus is stark, particularly after the abolition of non-dom status.

On £150,000 of business revenue (approximately EUR 175,000):

United Kingdom (Ltd company): Corporate tax at 25% = £37,500 on profits. Extracting remaining £112,500 as dividends at the higher/additional rate = approximately £38,000 dividend tax. National Insurance on any salary component. Total tax burden: approximately £75,000-80,000 (50%+ effective).

Cyprus (Ltd + Non-Dom): Corporate tax at 15% = EUR 26,250. Remainder distributed as dividends with 0% income tax + 2.65% GHS contribution. Total tax: approximately EUR 9,000-10,000 (5-6% effective).

Annual saving: approximately EUR 70,000-80,000 on EUR 175,000 of business revenue.

For UK entrepreneurs who previously benefited from non-dom status, the comparison is even more striking. Pre-April 2025, a non-dom could shelter foreign income from UK tax entirely. Post-abolition, worldwide income is fully taxable. For those with significant foreign income streams, Cyprus offers the Non-Dom structure that the UK just eliminated.

Cyprus also has zero capital gains tax on the disposal of securities (shares, bonds) that are not Cyprus-land-related. In the UK, capital gains are taxed at 10%/20% (or 18%/24% for property). For entrepreneurs planning an exit, relocating to Cyprus before selling a business can eliminate a substantial CGT liability.

Interactive Tax Calculator

United Kingdom

Effective rate

46%

Est. tax: €46,000

Cyprus (Non-Dom)

Effective rate

5%

Est. tax: €5,000

Annual savings by moving to Cyprus

€41,000

Estimates based on effective rates. Consult a tax advisor for your specific situation.

Cyprus Non-Dom: ~5% effective tax

The alternative most entrepreneurs do not know about

- ✓15% corporate tax (flat, no surcharges)

- ✓0% dividend income tax (Non-Dom)

- ✓2.65% GHS on all income

- ✓No wealth tax, no inheritance tax

- ✓60-day rule for flexible tax residency

- ✓Full EU membership and treaty network

Double Tax Treaty: United Kingdom - Cyprus

The UK and Cyprus have a comprehensive double tax treaty in force (originally signed 1974, updated via protocols). Key provisions: dividends 0-15% withholding (reduced rates apply where the recipient holds at least 10% of the paying company); interest 10%; royalties 5%. The treaty provides tie-breaker rules for dual residency based on permanent home, centre of vital interests, habitual abode, and nationality. UK pension income paid to Cyprus residents is generally taxable only in Cyprus under the treaty. Capital gains on shares are generally taxable only in the state of residence of the seller. Government pensions (state sector) remain taxable in the UK. Professional advice is essential given the interaction between the treaty and the new 4-year FIG (Foreign Income and Gains) regime introduced alongside non-dom abolition.

Leaving United Kingdom: Exit Process

The UK uses the Statutory Residence Test (SRT) to determine tax residency. Becoming non-UK-resident requires careful planning:

Automatic non-residence: If you spend fewer than 16 days in the UK in a tax year (or fewer than 46 days having been UK-resident in 1 of the previous 3 years), you are automatically non-UK-resident. Most entrepreneurs must plan a clean break mid-year.

Split year treatment: The UK allows split year treatment in the year of departure. Income earned up to the date of departure is taxable in the UK; income afterwards is taxed only in Cyprus (subject to treaty provisions).

HMRC notification: Notify HMRC of your departure by completing form P85 (if you were employed) or via your Self Assessment return. You must file a final Self Assessment tax return covering the tax year of departure.

National Insurance: You stop paying UK National Insurance once you cease UK employment/self-employment. You can make voluntary Class 2/3 contributions to protect your State Pension entitlement — currently £3.45/week Class 2 or £17.45/week Class 3 (2025/26 rates). This is generally cost-effective for the future UK State Pension.

UK State Pension: Your accrued State Pension rights are preserved. You need 35 qualifying years for a full new State Pension (£221.20/week in 2025/26). If you have fewer, voluntary NI contributions during your time in Cyprus may be worthwhile.

Property: If you retain UK residential property, CGT applies to gains on disposal regardless of your residency status. UK rental income remains taxable in the UK. A Non-Resident Landlord (NRL) scheme registration is required.

Pensions: Moving pensions to Cyprus is possible via QROPS (Qualifying Recognised Overseas Pension Schemes) but requires careful analysis. The 25% Overseas Transfer Charge may apply. In most cases, leaving UK pensions in place is simpler.

UK Non-Dom Abolished: What It Means for British Entrepreneurs

The abolition of the UK non-domiciled resident regime from 6 April 2025 was one of the most significant changes to UK personal taxation in decades. For the approximately 70,000 non-doms who had been claiming the remittance basis, the change is transformative: foreign income and gains are now fully taxable in the UK in the year they arise, regardless of whether they are remitted.

The replacement system — the 4-year Foreign Income and Gains (FIG) regime — offers a temporary shelter only for new arrivals to the UK who have not been UK-resident in the previous 10 years. Existing non-doms who had been in the UK for years do not benefit from the FIG regime. Their foreign income became fully taxable from April 2025.

For these individuals, the question becomes: what is the best alternative? Cyprus offers a structural answer through its own Non-Dom regime, which works in an almost mirror-image way to the pre-2025 UK non-dom system but with important advantages.

Under the Cyprus Non-Dom regime, a person who was not Cyprus tax resident in the 20 years immediately before becoming resident can elect for Non-Dom status. This election is available for up to 17 consecutive years. While a Cyprus Non-Dom is a Cyprus tax resident and pays Cyprus corporate tax at 15% on company profits, dividend income is exempt from personal income tax entirely (subject only to a 2.65% GHS healthcare contribution). Interest income is similarly exempt from personal income tax (though subject to 30% Special Defence Contribution for domiciled residents, which Non-Doms avoid). Capital gains on the disposal of securities are exempt from both income tax and CGT.

The practical result: a British entrepreneur who relocates to Cyprus, establishes a Cyprus Ltd company, and registers as Non-Dom will pay approximately 15% corporate tax on profits (which can be lowered through legitimate expenses and structures including the Cyprus IP Box) and approximately 2.65% on dividend distributions. The effective total rate on business income distributed to the founder is approximately 5%.

For a British entrepreneur who previously sheltered £300,000 of foreign income annually under the non-dom regime and now faces full UK taxation, the annual UK tax liability has increased by approximately £120,000-135,000 (at 40-45% rates). The same income structured through a Cyprus Ltd under the Non-Dom regime would generate approximately £15,000-18,000 in total tax. The annual saving from relocating rather than remaining in a post-non-dom UK: approximately £100,000-120,000.

The logistics of the relocation for former UK non-doms are generally more complex than for a typical UK-domiciled entrepreneur. Former non-doms may have significant foreign assets, foreign company structures, and offshore trust arrangements that require careful reorganisation before establishing Cyprus residency. A clean break from the UK — meeting the SRT non-residence test — is essential before the Cyprus Non-Dom election takes full effect.

Cost of Living: United Kingdom vs Cyprus

The cost difference between the UK (particularly London and the South East) and Cyprus is dramatic:

Housing: London 2-bed £2,200-£4,000/month vs Larnaca EUR 550-750/month (savings: 70-80%) Housing: Manchester/Birmingham £1,000-£1,600/month vs Larnaca EUR 550-750/month (savings: 30-50%) Groceries: UK £400-600/month vs Cyprus EUR 250-350/month (savings: 30-40%) Dining out: UK £300-500/month vs Cyprus EUR 150-200/month (savings: 50-60%) Transport: UK £150-250/month (public) vs Cyprus EUR 100-150/month (car-needed) Childcare: UK £1,500-2,500/child/month vs Cyprus EUR 400-700/child/month (massive saving for families) Utilities: UK £200-300/month vs Cyprus EUR 100-150/month

Total monthly (single professional): UK £2,500-4,000 vs Cyprus EUR 1,400-1,900 Total monthly (family of 4): UK £6,000-9,000 vs Cyprus EUR 3,000-4,500

The childcare differential is particularly significant for British families. UK childcare costs are among the highest globally and represent a major factor in the family relocation decision. Cyprus has a developing but much more affordable childcare sector.

The weather difference is also substantial: Cyprus averages 3,400 hours of sunshine annually versus approximately 1,500 in London. The lifestyle quality — beaches, outdoor living, a genuine Mediterranean pace — is a significant factor for British expats beyond the financial calculation.

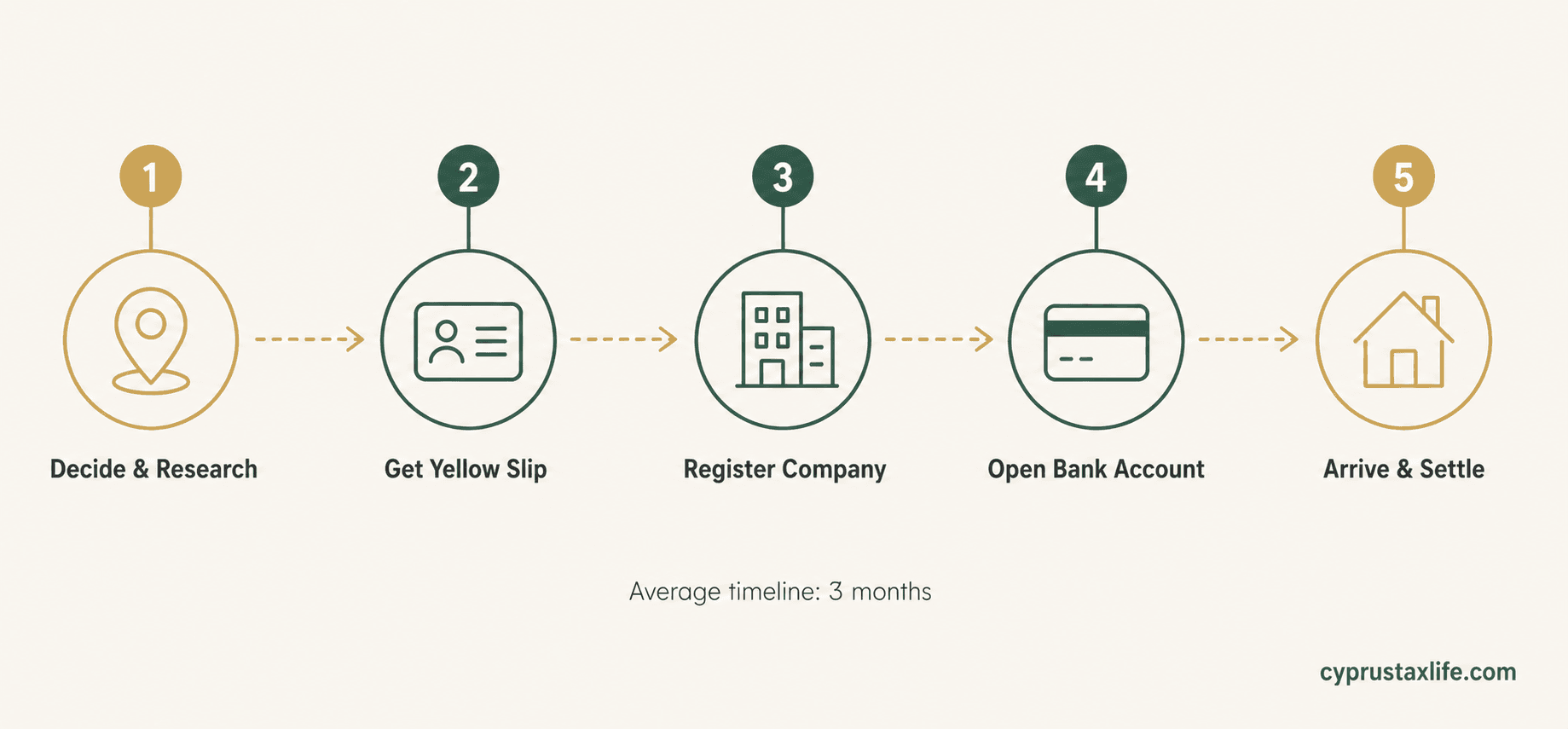

Step-by-Step Relocation Checklist

Plan your departure date carefully around the UK Statutory Residence Test (SRT)

Research Cyprus cities: Limassol (business hub), Larnaca (airport access), Paphos (lifestyle)

Set up a Cyprus Ltd company (5-7 working days, approximately EUR 2,100)

Find accommodation in Cyprus and sign a rental contract (evidence for tax residency)

Submit P85 form to HMRC or notify via Self Assessment of UK departure

File final UK Self Assessment tax return for the departure tax year

Assess voluntary NI contributions to protect UK State Pension entitlement

Register with Cyprus Tax Department to obtain Tax Identification Number (TIC)

Apply for Cyprus tax residency under 60-day or 183-day rule

Register for Non-Dom status at Cyprus Tax Department (Day 1 of residency)

Obtain your Yellow Slip (EU Settlement — note: UK citizens need to verify post-Brexit rules for Cyprus specifically)

Open a Cyprus bank account (Bank of Cyprus, Hellenic Bank, or AstroBank recommended)

Register for GHS healthcare (2.65% contribution on income)

Set up payroll structure: low salary within exempt threshold + dividends

Notify UK banks and investment platforms of Cyprus tax residency

Register UK property under Non-Resident Landlord scheme if retaining rental property

Review pension arrangements — voluntary NI contributions vs QROPS transfer

Learn more about Cyprus:

Frequently Asked Questions

Do I need to pay UK tax after moving to Cyprus?+

What happened to the UK non-dom regime?+

How many days can I spend in the UK after moving to Cyprus?+

Will I lose my UK State Pension by moving to Cyprus?+

Can I keep my UK bank accounts and investments after moving?+

What about CGT on UK property I keep?+

Do I need a visa to live in Cyprus as a British citizen post-Brexit?+

How much can I save by moving from the UK to Cyprus?+

Sources and References

- PwC Worldwide Tax Summaries — Cyprus

- KPMG Cyprus — Tax and Advisory

- EY Cyprus — Tax Services

- Cyprus Ministry of Finance (mof.gov.cy)

Effective rates are approximations for entrepreneur structures (company + low salary + dividends). Consult a qualified tax advisor before making decisions.

Free, no commitment

Moving to Cyprus or opening a company?

Tell us your situation and we'll connect you with our specialist expat advisory in Cyprus: Non-Dom tax, company setup and residency, done for you. Free consultation, no commitment.

Related Articles

![Cyprus Ltd vs Irish Ltd: Company Tax Compared [2026]](https://cdn.sanity.io/images/glqahhks/production/84e3d82538a859345d8d2447e8e097c5777fb238-1679x937.png?w=700&q=75&auto=format)

Compare a Cyprus Ltd vs an Irish Ltd on corporate tax, dividends, setup cost and substance. See which structure keeps more profit in your pocket in 2026.

Miriam Alonso

Miriam Alonso- Company & Accounting

Germany's exit tax (§6 AStG) taxes unrealised gains on shares >1% when you emigrate. Moving to Cyprus (EU): you can defer payment indefinitely. Full breakdown for German founders and investors.

Miriam Alonso- Tax Planning

- Relocation

![Why Open a Company in Cyprus? 7 Benefits [2026]](https://cdn.sanity.io/images/glqahhks/production/ab9d3315584a145746c27100aaff9e70c842959e-1679x937.png?w=700&q=75&auto=format)

Discover why entrepreneurs open a company in Cyprus: 15% tax, ~5% effective under Non-Dom, EU access, low cost. See if it is worth it for you.

Miriam Alonso- Company & Accounting