Moving from the Netherlands to Cyprus

Quick Answer

Moving from Netherlands to Cyprus with Non-Dom status reduces your effective tax rate from ~40-52% to approximately 5%. Cyprus applies 0% Special Defence Contribution on foreign dividends, a flat 15% corporate tax, and offers tax residency with just 60 days of physical presence per year under the 60-day rule. A double tax treaty between Netherlands and Cyprus prevents double taxation during the transition.

Last updated: 2026-05-29

Why Netherlands Professionals Consider Cyprus

The Netherlands has traditionally been seen as a business-friendly country, but the tax environment for entrepreneurs and company owners has become increasingly challenging. The Box 2 tax rate on dividends from substantial holdings (5%+) has risen to 26.9% in 2024, up from 26.25% in 2022. For company owners who rely on dividend distributions from their BV (besloten vennootschap), this is a significant increase.

The personal income tax in Box 1 reaches 49.5% for the highest bracket. Box 3 (the wealth tax on deemed investment returns) has been a source of controversy: Dutch taxpayers are taxed on a deemed return of approximately 6% on assets above EUR 57,000, regardless of actual returns. When actual investment returns are negative or below the deemed rate, taxpayers still pay tax. This system has been challenged in Dutch courts and is under ongoing revision, but it continues to create a tax burden on savings and investments.

For BV owners, the combined burden of Vennootschapsbelasting (VPB, Dutch corporate income tax at 25.8% on profits above EUR 200,000) plus Box 2 tax (26.9%) results in an effective combined rate of approximately 45% on profits distributed as dividends from large companies.

Amsterdam, Rotterdam, and other major Dutch cities are also among the most expensive places in Europe for housing. Rental prices in Amsterdam rival those of London and Paris. Many Dutch entrepreneurs making international comparisons find that Cyprus offers a dramatically better tax position within the EU, with no Box 2, no Box 3 wealth tax, and a simple 15% corporate rate.

Netherlands Tax Burden at a Glance

| Tax type | 🇳🇱 Netherlands |

|---|---|

| Income tax | Up to 49.5% (Box 1 earned income) |

| Corporate tax | 15% up to EUR 200K profit, 25.8% above |

| Capital gains tax | 36% on deemed return (Box 3) or 26.9% on substantial holdings (Box 2) |

| Dividend tax | 26.9% (Box 2 for 5%+ shareholders) |

| Social contributions | ~27.65% employer + ~17.9% employee (combined) |

| Effective rate | ~40-52% |

Tax Comparison: Netherlands vs Cyprus

On EUR 100,000 of business revenue:

Netherlands (BV + dividends, above EUR 200K bracket): VPB at 25.8% = EUR 25,800. Remaining EUR 74,200 as dividends at 26.9% = EUR 19,960. Total approximately EUR 45,760 (45.8% effective).

Netherlands (BV + dividends, up to EUR 200K bracket): VPB at 15% = EUR 15,000. Remaining EUR 85,000 as dividends at 26.9% = EUR 22,865. Total approximately EUR 37,865 (37.9% effective).

Cyprus (Ltd + Non-Dom): Corporate tax at 15% = EUR 15,000. Low salary plus dividends at 0% income tax + 2.65% GHS. Total approximately EUR 5,000 (5% effective).

Annual savings: approximately EUR 33,000-41,000.

The Box 3 wealth tax compounds the comparison for those with significant assets. A Dutch entrepreneur with EUR 500,000 in savings pays approximately EUR 10,000-12,000 per year in Box 3 taxes. Cyprus has no wealth tax, no deemed return taxation. The total annual benefit for a Dutch entrepreneur with significant assets can easily exceed EUR 50,000 per year.

Interactive Tax Calculator

Netherlands

Effective rate

45%

Est. tax: €45,000

Cyprus (Non-Dom)

Effective rate

5%

Est. tax: €5,000

Annual savings by moving to Cyprus

€40,000

Estimates based on effective rates. Consult a tax advisor for your specific situation.

Cyprus Non-Dom: ~5% effective tax

The alternative most entrepreneurs do not know about

- ✓15% corporate tax (flat, no surcharges)

- ✓0% dividend income tax (Non-Dom)

- ✓2.65% GHS on all income

- ✓No wealth tax, no inheritance tax

- ✓60-day rule for flexible tax residency

- ✓Full EU membership and treaty network

Double Tax Treaty: Netherlands - Cyprus

The Netherlands and Cyprus have a double tax treaty in force. Key provisions: dividends 0% (if the beneficial owner is a company holding at least 25% of the capital) or 15% otherwise, interest 0%, royalties 0%. For individual shareholders, the 15% treaty rate typically applies, though often overridden by domestic law or the EU Free Movement provisions. The Netherlands has CFC rules and anti-dividend stripping provisions. Dutch tax authorities are known for their active enforcement of substance requirements for corporate structures. For individuals genuinely relocating to Cyprus, the treaty provides clear tie-breaker rules based on permanent home and center of vital interests.

Leaving Netherlands: Exit Process

The Netherlands has a generally straightforward exit process for individuals:

BRP deregistration: You must deregister from the BRP (Basisregistratie Personen) at your municipality. This is done by submitting a departure form (vertrekmelding) to your local gemeente. The deregistration should be done shortly before or at the time of departure.

Belastingdienst notification: Notify the Dutch tax authority (Belastingdienst) of your change of address and tax residency. In the year of departure, you must file an M-form (Migrant form) tax return, which covers the period of Dutch residency.

No individual exit tax: The Netherlands does not impose an exit tax on unrealized capital gains on shares for individual taxpayers (unlike at the corporate level). This is a significant advantage.

Box 3 wealth tax: This ceases to apply from the date you are no longer a Dutch tax resident. However, Dutch real estate remains subject to Dutch Box 3 tax even after departure.

Healthcare: Your Dutch statutory health insurance (zorgverzekering) ends upon deregistration. You will transition to the Cyprus GHS. Any overpaid zorgtoeslag (healthcare allowance) may need to be repaid.

AWBZ/WLZ: Your entitlement to long-term care insurance benefits ends. Accrued pension rights in AOW (state pension) are preserved under EU coordination rules.

Conserverende Aanslag: The Dutch Exit Tax Explained

When a Dutch BV (besloten vennootschap) shareholder with a substantial interest (aanmerkelijk belang — 5%+) emigrates from the Netherlands, the Dutch tax authority (Belastingdienst) can issue a Conserverende Aanslag (protective assessment) on the unrealized dividend gain (fictief regulier voordeel) attributable to retained earnings in the BV. This is the Dutch version of an exit tax, and it catches many Dutch entrepreneurs off-guard when planning their relocation.

How the Conserverende Aanslag works: upon emigration, the Belastingdienst assesses a notional dividend equal to the retained earnings (winstreserves) of the BV that have not yet been distributed. This is treated as if the company had paid out all its retained profits as a dividend on the day of departure. The Box 2 rate of 26.9% applies. For a BV with EUR 300,000 in retained earnings, the assessed Conserverende Aanslag would be EUR 300,000 × 26.9% = EUR 80,700.

Crucially, the Conserverende Aanslag is not immediately payable. For moves to other EU or EEA member states - including Cyprus - the payment is deferred indefinitely as long as the shares are not disposed of and the taxpayer does not move to a non-EU/EEA country. The Belastingdienst places a lien (recht van hypotheek or pandrecht) on your assets as security for the deferred amount. There is no interest charged on the deferred Conserverende Aanslag during the deferral period.

The deferral ends and the Conserverende Aanslag becomes immediately due in full if: you sell or transfer the BV shares, you move from Cyprus to a country outside the EU or EEA, or the BV distributes the retained earnings that formed the basis of the assessment. This last point is particularly important: if you later decide to distribute those historic retained earnings from the Dutch BV after moving to Cyprus, the Conserverende Aanslag triggers.

Practical implications: many Dutch entrepreneurs who move to Cyprus and wind down their BV gradually find that distributing the retained earnings is the final step that triggers the Conserverende Aanslag payment. The tax owed is the same as it would have been in the Netherlands (26.9% of the distributed retained earnings assessed on departure). The Cyprus-Netherlands double tax treaty generally does not provide relief because the Conserverende Aanslag is assessed under Dutch domestic law on the Dutch company's retained earnings, not on current Cyprus-source income.

Planning strategy: entrepreneurs who are aware of the Conserverende Aanslag before departure often structure their BV exit more carefully - for example, distributing retained earnings as dividends to the entrepreneur while still Dutch-resident (paying the current 26.9% Box 2 tax at that time), thereby reducing the basis of any future Conserverende Aanslag. This is an area where pre-departure Dutch tax advice is essential, as the decisions made in the 12-24 months before emigration significantly affect the total tax outcome.

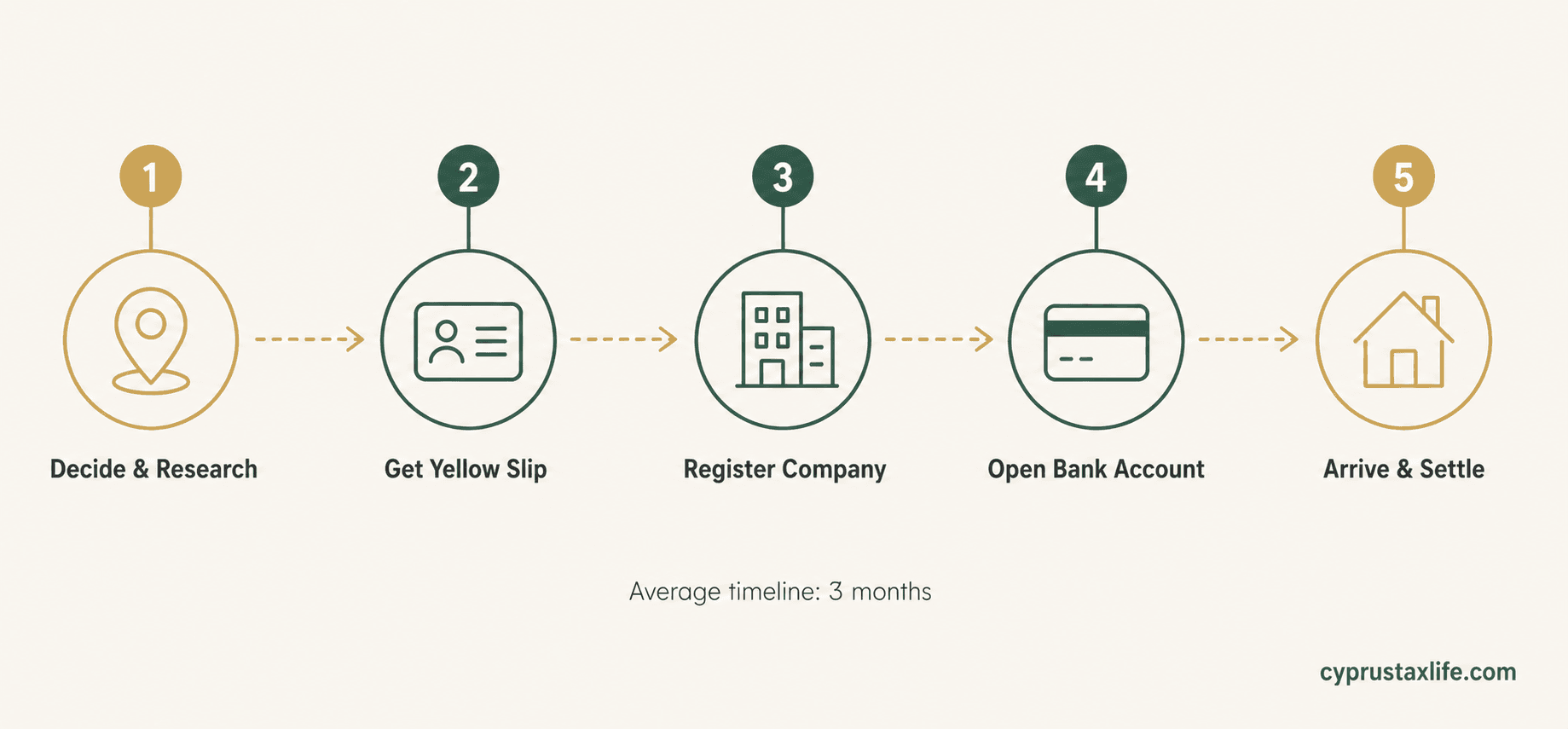

Timeline: Moving from the Netherlands to Cyprus Step by Step

Month 0 (planning phase): Consult a Dutch tax advisor to assess Conserverende Aanslag exposure. Calculate unrealized retained earnings in your BV. Decide whether to distribute pre-departure dividends to reduce the basis. Begin researching Cyprus cities — Limassol and Larnaca are the most popular for Dutch expats.

Month 1-2: Set up your Cyprus Ltd (approximately 5-7 working days to incorporate once documents are submitted). Sign a rental contract in Cyprus — the rental contract is required for the Yellow Slip application and Tax Department registration. Open a Cyprus bank account (Bank of Cyprus or Hellenic Bank recommended; bring passport, rental contract, company documents, and proof of source of funds).

Month 2-3: File the vertrekmelding (departure notification) at your Dutch gemeente. This deregisters you from the BRP (Basisregistratie Personen). Notify the Belastingdienst of your departure — request the M-form (Migrant form) for tax filing. Cancel your Dutch zorgverzekering (health insurance) — coverage ends on the date your BRP registration lapses. Apply for the GHS in Cyprus.

Month 3-4: Apply for your Yellow Slip at the Cyprus Migration Department with your EU passport, rental contract, and proof of sufficient means or employment. File for Cyprus tax residency at the Tax Department — bring TIC application form, passport, rental contract, and the company documents. Apply for Non-Dom status simultaneously — a simple declaration at the same office.

Month 4-6: Set up the payroll structure in Cyprus: low salary (within the EUR 22,000 tax-free threshold) plus dividends from the Cyprus Ltd. File the M-form with the Belastingdienst covering your Dutch income up to the departure date. Begin annual Non-Dom GHS contribution payments.

Month 6 and beyond: Manage any remaining Dutch BV obligations. If the Dutch BV continues to hold assets, consult annually with a Dutch tax advisor to ensure the Conserverende Aanslag deferral conditions remain met. Under the Netherlands-Cyprus double tax treaty, income earned through your Cyprus Ltd from clients worldwide is taxable only in Cyprus (the state of residence).

Cost of Living: Netherlands vs Cyprus

The Netherlands, especially the Randstad (Amsterdam, Rotterdam, The Hague, Utrecht), is one of Europe's most expensive regions:

Housing: Amsterdam EUR 1,600-2,800 rent vs Larnaca EUR 550-750 (savings: 65-75%). Rotterdam EUR 1,200-2,000. Utrecht EUR 1,200-1,800. Groceries: Netherlands EUR 350-450 vs Cyprus EUR 250-350 (savings: 25-35%) Dining out: Netherlands EUR 250-350 vs Cyprus EUR 150-200 (savings: 40%) Transport: Netherlands EUR 100-150 vs Cyprus EUR 100-150 (comparable, but cycling infrastructure in NL makes it cheaper for commuters) Utilities: Netherlands EUR 200-280 vs Cyprus EUR 100-150 (significantly less heating needed)

Total monthly: Netherlands EUR 2,800-3,800 vs Cyprus EUR 1,400-1,900

The climate shift from the Dutch "grey skies" culture to the Mediterranean is often cited by Dutch expats in Cyprus as a major quality-of-life improvement. The Netherlands averages about 1,680 hours of sunshine per year, compared to Cyprus's 3,400+. Dutch expats in Cyprus frequently comment on the improvement in mental wellbeing alongside the financial benefits.

Step-by-Step Relocation Checklist

Research Cyprus cities, particularly Limassol and Larnaca

Set up a Cyprus Ltd company (approximately EUR 2,100)

Find accommodation in Cyprus and sign a rental contract

File a vertrekmelding (departure notification) at your Dutch gemeente

Notify the Belastingdienst of your departure and new address

File an M-form (Migrant form) tax return for the year of departure

Cancel your Dutch zorgverzekering (health insurance) upon departure

Apply for Cyprus tax residency (60-day or 183-day rule)

Register for Non-Dom status at the Cyprus Tax Department

Obtain your Yellow Slip (EU citizen registration)

Open a Cyprus bank account

Register for GHS healthcare

Set up payroll structure in Cyprus (low salary + dividends)

Review any Dutch DigiD and digital service arrangements

Frequently Asked Questions

What is the Dutch Box 2 tax and how does it affect me?+

What is the Dutch Box 3 wealth tax?+

Does the Netherlands have an exit tax?+

What happens to my Dutch AOW pension after moving?+

Can I keep my Dutch BV after moving to Cyprus?+

Sources and References

- PwC Worldwide Tax Summaries — Cyprus

- KPMG Cyprus — Tax and Advisory

- EY Cyprus — Tax Services

- Cyprus Ministry of Finance (mof.gov.cy)

Effective rates are approximations for entrepreneur structures (company + low salary + dividends). Consult a qualified tax advisor before making decisions.

Free, no commitment

Moving to Cyprus or opening a company?

Tell us your situation and we'll connect you with our specialist expat advisory in Cyprus: Non-Dom tax, company setup and residency, done for you. Free consultation, no commitment.

Related Articles

Germany's exit tax (§6 AStG) taxes unrealised gains on shares >1% when you emigrate. Moving to Cyprus (EU): you can defer payment indefinitely. Full breakdown for German founders and investors.

Miriam Alonso

Miriam Alonso- Tax Planning

- Relocation

Canada's departure tax treats you as having sold your worldwide assets the day you stop being a tax resident. What is caught, what is exempt, how to defer it, and what the cost-base reset means for where you go next.

![Countries With No Property Tax [2026]: The Real Cost](https://cdn.sanity.io/images/glqahhks/production/6f7ea0efceed8a692ad7c3785efa8baaf4d1e208-1679x937.jpg?w=700&q=75&auto=format)

Compare countries with no property tax and the stamp duty they charge instead. See the 10-year holding cost that makes Cayman pricier than Portugal.

Miriam Alonso