Quick Answer

Non-Dom residents in Cyprus pay 0% Special Defence Contribution (SDC) on dividends. The only charge is a 2.65% GHS contribution, capped at EUR 4,770 per year on income up to EUR 180,000. Domiciled residents pay 17% SDC plus 2.65% GHS on dividends. Non-Dom status applies automatically to most foreign nationals for up to 17 years.

Cyprus Dividend Tax: 0% Rate for Non-Dom Residents

One of the biggest advantages of taxes in Cyprus: Non-Dom residents pay just 2.65% on dividends, with no income tax or SDC. Here is the complete breakdown with real numbers.

Last updated:

Dividend Tax: Cyprus vs Your Country — Side by Side

Select your country and dividend amount to compare what you'd actually keep.

| Country | Dividend tax rate | Tax on your dividends | Net you keep |

|---|---|---|---|

| United Kingdom | 38.1% | EUR 38,100 | EUR 61,900 |

| Cyprus Non-Dom | ~5% effective* | EUR 5,000 | EUR 95,000 |

*Cyprus Non-Dom effective rate: 2.65% GHS on dividends (no income tax, no SDC for non-domiciled). Corporate tax at company level is separate. Comparison rates are standard personal dividend tax rates for 2025/26. Individual circumstances may vary.

Key Facts 2026

| Non-Dom dividend income tax | 0% (fully exempt from SDC) |

| Non-Dom GHS on dividends | 2.65% only |

| GHS annual cap | EUR 4,770 (applied when income exceeds EUR 180,000) |

| Standard resident: SDC | 5% SDC on dividends (reduced from 17% in 2026 reform) |

| Standard resident: total rate | 5% SDC + 2.65% GHS = 7.65% |

| Non-resident withholding | 0% |

| EUR 50k dividends (Non-Dom) | EUR 1,325 GHS tax |

| EUR 100k dividends (Non-Dom) | EUR 2,650 GHS tax |

| EUR 200k+ dividends (Non-Dom) | EUR 4,770 GHS tax (capped) |

Free, no commitment

Moving to Cyprus or opening a company?

Tell us your situation and we'll connect you with our specialist expat advisory in Cyprus: Non-Dom tax, company setup and residency, done for you. Free consultation, no commitment.

Get personalised guidance on Non-Dom status, company formation, and your specific tax situation from an experienced Cyprus tax advisor.

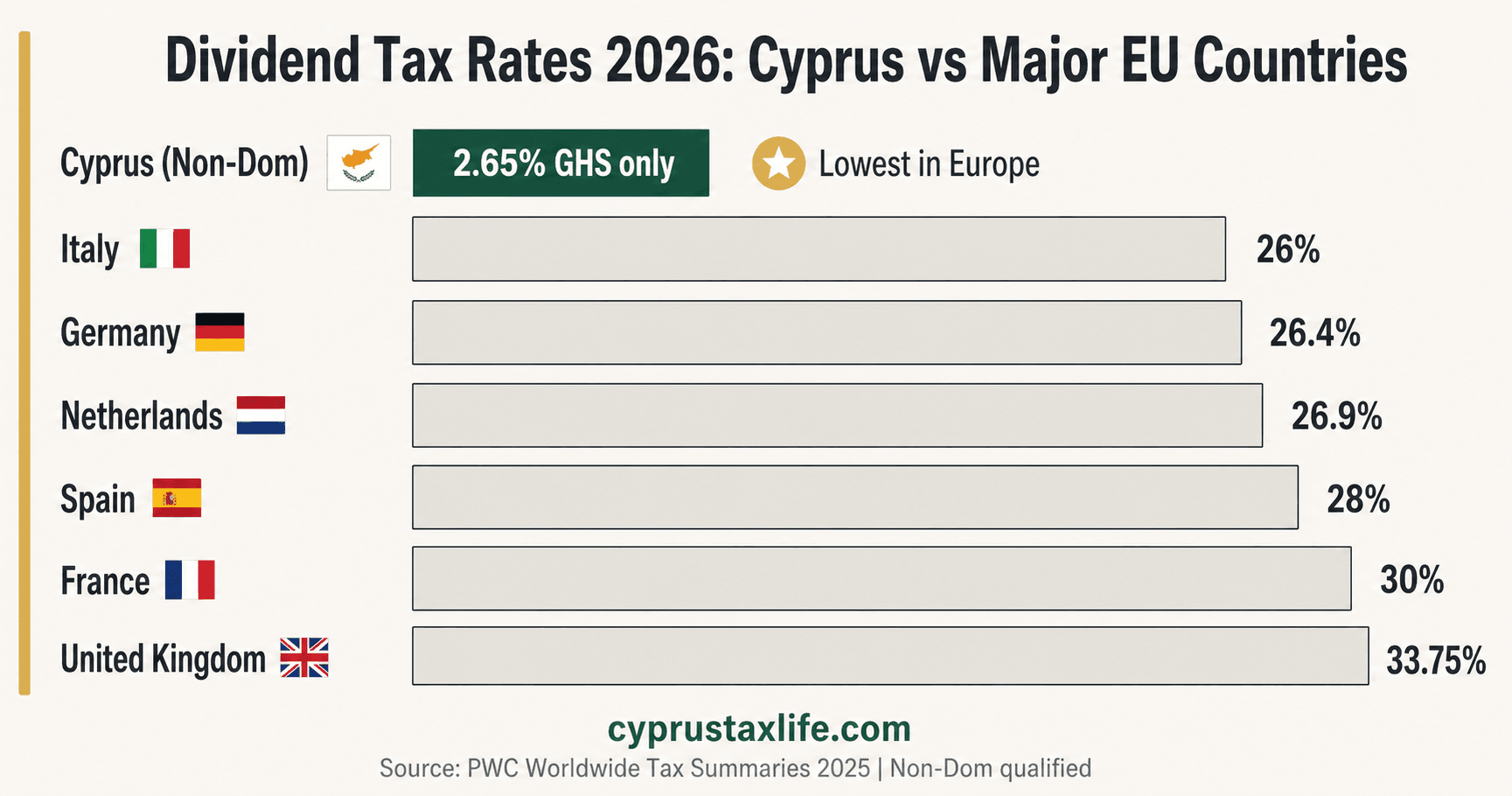

Dividend Tax Rates: Cyprus vs Other EU Countries (2026)

| Country | Dividend Tax Rate | Notes |

|---|---|---|

| Cyprus (Non-Dom) | 2.65% | GHS contribution only, 0% income tax on dividends |

| Bulgaria | 5% | Flat rate withholding tax |

| Estonia | 20% | Taxed at distribution (CIT level), 0% if retained |

| Spain | 19-28% | Progressive rate on savings income |

| Germany | 26.375% | Kapitalertragsteuer (25%) + Solidaritätszuschlag (5.5%) |

| Netherlands | 26.9% | Box 2 tax on substantial holdings |

| Portugal | 28% | Flat withholding rate (NHR ended 2024) |

| France | 30% | Prelevement Forfaitaire Unique (PFU) flat tax |

| UK | up to 39.35% | Higher rate (33.75%) + additional rate (39.35%) |

| Ireland | 51% | Income tax (40%) + USC (8%) + PRSI (4%) |

Cyprus Non-Dom rate applies for up to 17 years. Rates shown for tax residents receiving domestic or foreign dividends. Sources: PwC Worldwide Tax Summaries, KPMG Tax Rates Online, updated 2026.

Dividend Tax at a Glance

- 2.65%

- Total dividend tax with Non-Dom

- 0%

- Income tax on dividends

- €1,325/year

- Tax on €50K annual dividends

- ~15%

- Effective total tax rate on €100K income

How Cyprus Compares to Other Countries

Effective dividend tax rates on 50,000 EUR in dividends (assuming corporate profits already taxed):

- Cyprus (Non-Dom): 2.65% = 1,325 EUR

- Spain: 19-23% = 9,500-11,500 EUR (progressive rates)

- Portugal: 28% flat = 14,000 EUR

- United Kingdom: 8.75-39.35% = 4,375-19,675 EUR

- Germany: ~26.4% = 13,188 EUR (includes solidarity surcharge)

The Cyprus dividend tax rate with Non-Dom status is the lowest in the EU by a significant margin, making it the most attractive jurisdiction for dividend-based income structures.

EU's Lowest Dividend Tax

At just 2.65%, Cyprus Non-Dom offers the most favorable dividend taxation among all EU member states.

What Is the Optimal Salary and Dividends Split in Cyprus?

The standard compensation approach for directors of a Cyprus Ltd combines a modest salary with dividend distributions.

Salary component

- Employee Social Insurance contribution: 8.8% of salary

- Employer Social Insurance contribution: 8.8% of salary

- GHS on salary: 2.65% (employee) + 2.90% (employer)

- Income tax on salary: 0% on the first 19,500 EUR

Dividend component

- Corporate tax already paid: 15% on company profits

- Cyprus dividend tax (Non-Dom): only 2.65% GHS

- No additional income tax on dividends

- No Social Insurance on dividends

Why Low Salary?

Social Insurance applies to salary but not dividends. A modest salary covers GESY and pension contributions. Remaining profits are distributed as dividends at only 2.65%.

Want to optimize your dividend tax structure?

We can introduce you for free to specialist advisors who work with Non-Dom residents on dividend tax planning in Cyprus.

Looking to optimize your dividend tax? We can introduce you for free to specialist advisors in Cyprus who work with Non-Dom residents and foreign shareholders.

What Business Expenses Can You Deduct in Cyprus?

Every legitimate expense reduces your taxable profit. 5,000 EUR in expenses saves 750 EUR in corporate tax.

Professional Services

- Accounting, annual audit, and bookkeeping

- Legal and tax advisory fees

- Company secretary and registered office services

Office and Technology

- Office rent or co-working space membership

- Laptops, monitors, peripherals

- Software licenses and SaaS subscriptions

- Internet and mobile phone bills

Travel and Development

- Business flights and accommodation

- Local transport and fuel for business use

- Meals during business travel

- Training courses and conferences

Other Deductions

- Marketing, advertising, website costs

- Business insurance (incl. health insurance for directors)

- Bank charges and payment processing fees

- Professional memberships and subscriptions

How Do Consultancy Fees Work Through a Cyprus Ltd?

When your Cyprus Ltd invoices clients for consultancy services, the income flows through the company and is eventually distributed as dividends.

The effective tax on consultancy fees:

- Corporate tax: 15%

- Dividend tax (Non-Dom): 2.65% on the after-tax distribution

Combined effective rate: approximately 14.8%. This makes the Cyprus dividend tax structure one of the most competitive in the EU for professional services income.

Effective Rate: ~14.8%

Consultancy income through a Cyprus Ltd is taxed at 15% corporate + 2.65% on distribution.

Can You Invoice Up to 15,600 EUR Without VAT in Cyprus?

In addition to salary and dividends, it is possible to invoice clients directly as an individual. Below 15,600 EUR annual invoicing, there is no obligation to register for VAT.

Directors who take a modest salary of around 10,000 EUR can invoice an additional 9,000-9,500 EUR personally and pay zero income tax on it. The only charge is the 2.65% GHS contribution.

Example

A director earning 10,000 EUR salary who invoices 9,000 EUR personally:

- Total personal income: 19,000 EUR

- Income tax: 0 EUR (within the 19,500 EUR tax-free bracket)

- VAT: not applicable (below 15,600 EUR threshold)

- GHS on personal invoices: approximately 239 EUR

Important Considerations

Services must be genuine and distinct from company work. Income must be declared in the personal annual tax return. Consult an accountant for correct setup.

What Are the Legal Requirements to Distribute Dividends?

All conditions must be satisfied before distributing dividends from your Cyprus Ltd.

Distributable Profits Required

The company must have accumulated profits after covering any losses before a dividend can be declared.

Board Resolution + Solvency

A board resolution must be passed approving the distribution, and the company must remain solvent afterward.

GHS Withholding (2.65%)

The 2.65% GHS must be withheld and remitted to the Tax Department. Your accountant handles this as part of the annual package.

Interim vs Final Dividends

Cyprus allows interim dividends (during the year) and final dividends (after annual accounts). Most small companies use interim dividends for regular income.

Frequently Asked Questions

Do I pay income tax on dividends in Cyprus?

Dividends are not subject to personal income tax in Cyprus. They are only subject to SDC (0% for Non-Dom) and GHS (2.65%).

Can I distribute dividends monthly?

Yes, you can distribute interim dividends monthly as long as your company has sufficient projected profits and remains solvent. The frequency is entirely flexible, so monthly, quarterly, or any other schedule is permitted under Cyprus law.

What if my company has no profits?

If your company has no profits, you cannot distribute dividends because doing so would constitute an illegal distribution and create personal liability for directors. Learn more in our company formation guide.

What is the dividend tax rate in Cyprus for Non-Dom residents?

Dividend tax for Non-Dom residents in Cyprus is 2.65% (the GHS contribution). No income tax, SDC, or withholding tax applies to dividend distributions. Combined with the 15% corporate tax rate, this creates an effective rate of approximately 5% on corporate earnings distributed as dividends.corporate tax on company profits, the effective total tax rate on business income distributed as dividends is approximately 14.8%.

Do I need Non-Dom status to benefit from low dividend tax in Cyprus?

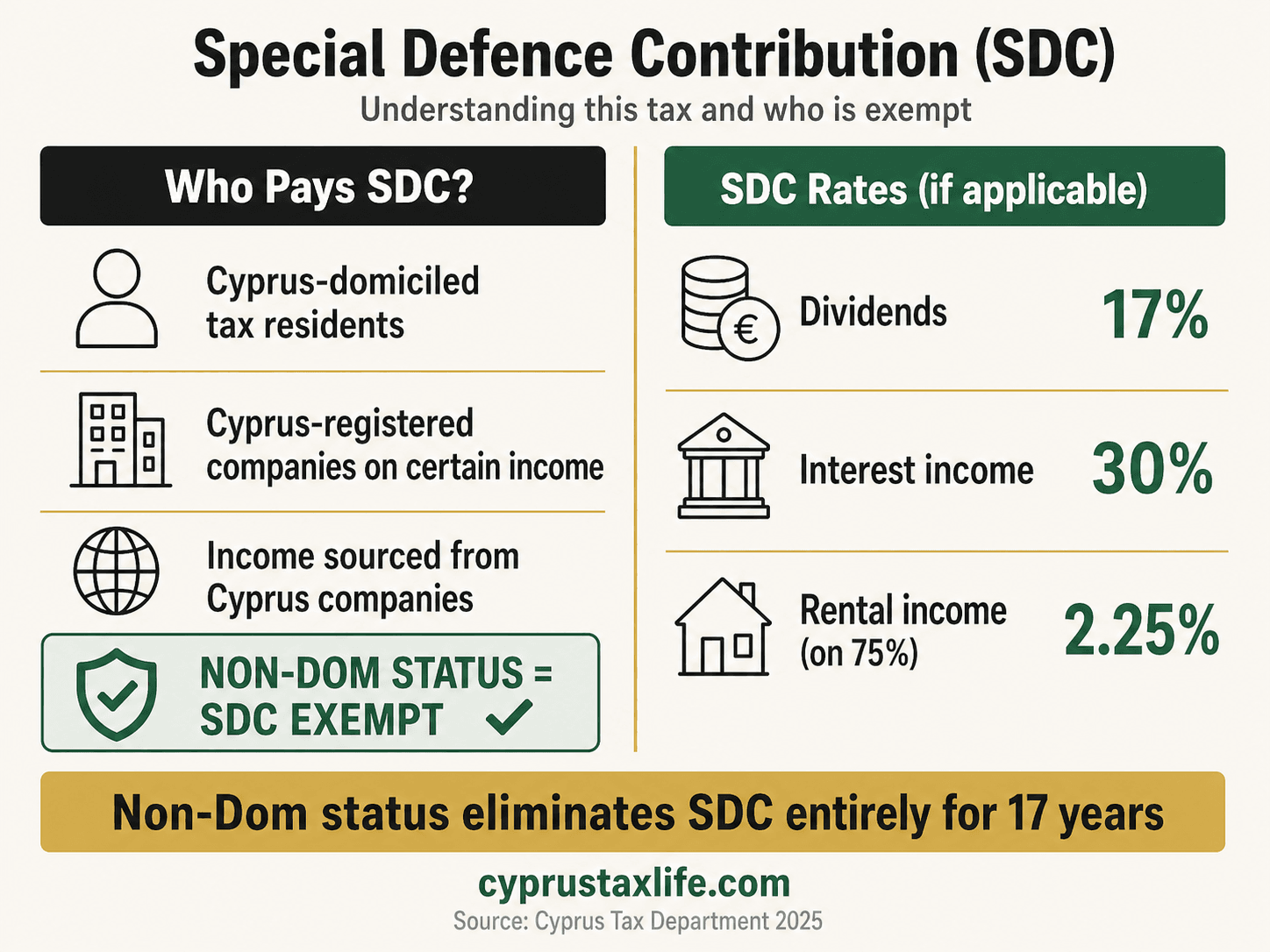

No, Non-Dom status is not required. Domiciled Cyprus tax residents pay 7.65% total (5% SDC plus 2.65% GHS) on dividends from 2026 profits onwards, down from 19.65% previously. Pre-2026 profits remain taxed at 17% SDC for domiciled residents. Non-Dom status eliminates SDC entirely, lowering the effective rate to 2.65% GHS on all dividends, but standard domiciled rates are already competitive.

What is SDC (Special Defence Contribution) on dividends in Cyprus?

SDC on dividends is 0% for non-domiciled residents and 5% for domiciled residents on profits earned from 1 January 2026 onwards. Pre-2026 profits distributed before 31 December 2031 remain taxed at 17% SDC for domiciled residents. Non-doms enjoy complete SDC exemption regardless of profit year.

What is the GHS cap on dividends in Cyprus?

The maximum GHS contribution on dividends is EUR 4,770 per year, calculated as 2.65% on the first EUR 180,000 of annual income. Once you exceed EUR 180,000 in total income, the GHS contribution cap applies and no further GHS is due on additional dividends.

How much tax do I actually pay on dividends as a Non-Dom in Cyprus? Give me examples.

You pay only 2.65% GHS on dividends as a Cyprus Non-Dom, capped at EUR 4,770 yearly. On EUR 50,000 dividends: EUR 1,325 tax. On EUR 100,000: EUR 2,650. On EUR 200,000+: EUR 4,770 (the maximum, since GHS base caps at EUR 180,000). You owe zero income tax and zero SDC on dividend income.

What is the 4 year rule for dividends in Cyprus?

Cyprus companies must distribute at least 70% of after-tax accounting profits within 2 years of tax year-end, or undistributed amounts become deemed dividends. For Non-Dom shareholders, only 2.65% GHS applies (SDC exemption covers deemed dividends). Domiciled shareholders pay the applicable SDC rate (5% for post-2026 profits) plus 2.65% GHS on deemed amounts.

Is there withholding tax on dividends in Cyprus?

Cyprus does not impose withholding tax on dividends paid to individual shareholders, whether Cyprus tax residents, non-residents, or foreign shareholders. From 2026, a 5% withholding tax applies only on dividends paid by a Cyprus company to associated companies in jurisdictions with a corporate tax rate below 7.5% (low-tax or blacklisted jurisdictions). This does not affect dividends paid to individual shareholders.

How does Cyprus dividend tax compare to other EU countries?

Cyprus offers the lowest individual dividend tax in the EU at 2.65% GHS for Non-Dom residents, compared to Germany 25%, France 30%, Italy 26%, Spain 19-28%, Portugal 28%, Netherlands 15% withholding plus income tax, and UK 8.75-39.35%. Bulgaria charges 5% flat and Malta achieves 5-6% effective rate through imputation refunds. No other EU country provides a sub-3% effective rate without complex structures.

How does the 2026 Cyprus tax reform affect dividend tax?

From 1 January 2026, Cyprus reduced SDC on dividends from 17% to 5% for domiciled residents on profits earned that date forward. Non-Dom residents remain exempt from SDC and pay only 2.65% GHS on all dividends. The reform also imposed 5% withholding tax on dividends to companies in jurisdictions with corporate tax below 7.5%, though individual shareholders are unaffected.

How can I reduce my dividend tax liability legally in Cyprus?

The primary legal mechanism is Non-Dom status, which eliminates the 17% SDC on dividends entirely. A Non-Dom resident pays only 2.65% GHS (capped at EUR 4,770/year). To qualify, establish Cyprus tax residency via the 60-day rule or 183-day rule, and confirm you are not domiciled in Cyprus. A specialist Cyprus tax advisor can verify your eligibility and structure the arrangement correctly.

Are there specialist advisors for Cyprus dividend tax optimization?

Yes. Several Cyprus-based accounting and tax advisory firms specialize in dividend tax structuring for Non-Dom residents and foreign shareholders in Cyprus companies. We work with vetted specialists in this area and can provide a free introduction to the right advisor for your situation.

Want this reviewed for your situation?

Book a 1-on-1 call with someone who has relocated to Cyprus and set up a company — Non-Dom, residency, company formation and real numbers.

The standalone Cyprus Dividend Tax Calculator lets you compare Non-Dom (2.65% GESY only, capped at EUR 4,770) versus domiciled (5% SDC under the 2026 reform) scenarios side by side for any dividend amount.

Frequently Asked Questions

What changed for dividend tax in Cyprus with the 2026 reform?

For non-domiciled residents, nothing changed: dividends remain subject only to 2.65% GHS (GESY) and are fully exempt from income tax and Special Defence Contribution (SDC). The effective rate on dividends for a non-dom remains 2.65%.

For domiciled Cyprus residents (those who have lived in Cyprus for 17 or more of the past 20 years), the SDC rate on dividends increased from 17% to 17.5%. This affects a small minority of long-term residents who no longer qualify for non-dom status. The corporate tax rate from which dividends are distributed increased from 12.5% to 15%, affecting pre-distribution profit but not the SDC or income tax treatment at shareholder level.

Free, no commitment

Moving to Cyprus or opening a company?

Tell us your situation and we'll connect you with our specialist expat advisory in Cyprus: Non-Dom tax, company setup and residency, done for you. Free consultation, no commitment.

Related resources

Dividend scenarios

Real before/after dividend tax for 5 country profiles

Dividend tax for SaaS founders

How Cyprus SaaS companies pay themselves and minimise dividend tax

Dividend tax for creators

YouTube, Substack and creator income — dividend vs salary split in Cyprus

Dividend tax for freelancers

Contractor dividend strategy: Cyprus Ltd + Non-Dom = lowest EU effective rate

Cyprus vs UK dividend tax

UK abolished its Non-Dom regime — Cyprus charges 2.65% where UK charges 33%+

Rental income & SDC

Non-Dom residents are fully exempt from SDC on rental income too

Free newsletter

What do you want to hear about?

No spam. Unsubscribe any time.