Quick Answer

The Cyprus IP Box regime taxes qualifying intellectual property income at an effective rate of approximately 2.5% corporate tax. An 80% deduction applies to net profit from qualifying IP assets including patents, software, and know-how developed by the company. The regime is OECD-compliant under the modified nexus approach and has no sunset clause.

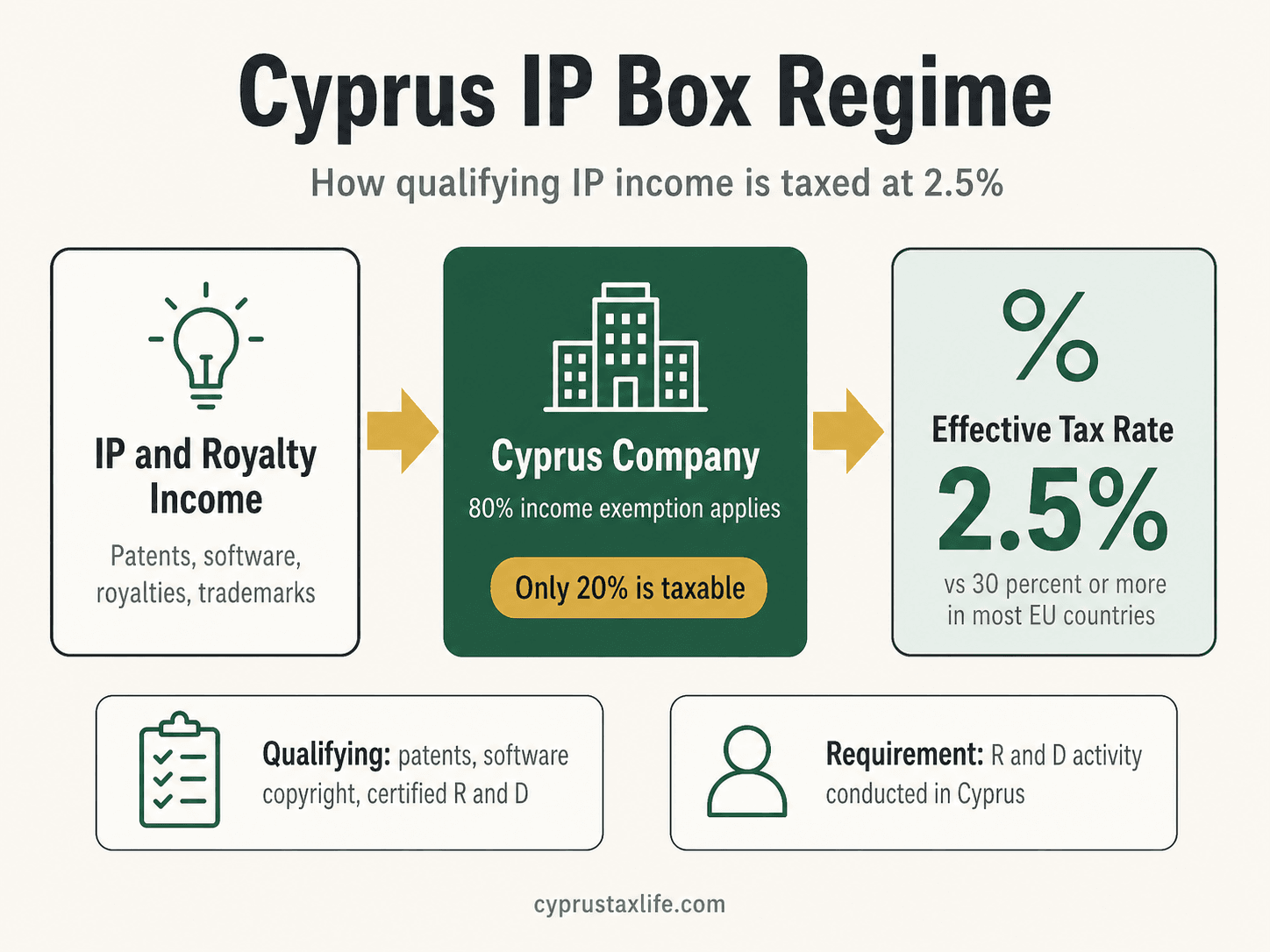

Cyprus IP Box: 2.5% Tax on Intellectual Property Income

Cyprus's IP Box regime offers an 80% exemption on qualifying income from intellectual property, reducing the effective corporate tax rate to just 2.5%. One of the most competitive IP regimes in the EU.

Last updated:

What Is the Cyprus IP Box Regime?

The Cyprus IP Box (Intellectual Property Box) is a preferential tax regime that reduces the effective corporate tax rate on qualifying IP income from 15% to just 2.5%. It does this by granting an 80% exemption on net income derived from qualifying intellectual property assets, meaning only 20% of that income is subject to the standard 15% corporate tax.

The regime has been in place since 2012 and was updated in 2016 to comply with OECD BEPS Action 5 (the modified nexus approach). It applies to income generated from the exploitation, licensing or sale of qualifying IP, making it one of the most competitive IP regimes in the European Union.

Which IP Assets Qualify for the Cyprus IP Box?

The following categories of intellectual property qualify for the 80% income exemption:

Patents and patentable inventions, covering registered patents, utility models and exclusive licences for patents. Copyrighted software, all software developed in-house or through outsourced R&D, including SaaS products, applications and algorithms. Other IP assets meeting the OECD nexus criteria, provided the IP was not acquired from a related party without significant in-house development.

Notably, trademarks, brand names and customer lists do not qualify for the IP Box. The regime is designed for functional, technical IP rather than marketing IP. Software is the most commonly used qualifying category in practice, making the Cyprus IP Box particularly attractive for technology companies, SaaS businesses and software developers.

How the IP Box 80% Exemption and Nexus Ratio Work

The qualifying income is calculated using the nexus ratio: the proportion of R&D expenditure incurred directly by the company (or outsourced to unrelated parties) relative to total R&D expenditure including acquired IP costs. In practice, for most early-stage tech companies that develop their IP internally, the nexus ratio is close to 100%, meaning the full 80% exemption applies.

Example: A Cyprus SaaS company earns €500,000 net IP income per year. With a 100% nexus ratio, 80% (€400,000) is exempt, leaving €100,000 subject to 15% corporate tax, an effective IP income tax of just €15,000, or 3% of gross revenue on that income stream.

Cyprus IP Box vs Other EU Regimes

Compared to other European IP Box regimes, Cyprus offers one of the lowest effective rates. The Netherlands innovation box offers a 9% effective rate; Luxembourg's IP regime applies a 20% exemption for a lower effective rate than Cyprus; Ireland's Knowledge Development Box applies a 6.25% rate. At 2.5%, Cyprus has the most competitive rate among mainstream EU jurisdictions for IP income.

An additional advantage is the combination with the Cyprus Non-Dom dividend regime: IP income taxed at the corporate level at 2.5%, then distributed as dividends to a Non-Dom shareholder who pays only 2.65% GHS, resulting in a combined effective rate of approximately 5% on IP-generated income.

How the Cyprus IP Box Works

80% of qualifying IP income is deducted from taxable income, leaving only 20% subject to the standard 12.5% corporate tax rate. The arithmetic is straightforward: 20% × 12.5% = 2.5% effective tax rate on qualifying IP profits.

Qualifying income types covered by the IP Box include: royalties from licensing IP to third parties or related parties; income embedded in the price of products or services where the value is attributable to the underlying IP; gains from the disposal of qualifying IP assets; and income from insuring or financing qualifying IP. This broad definition means SaaS subscription revenue, per-seat software licence fees, patent royalties, and gains from selling a patent portfolio all potentially qualify.

The deduction applies at the corporate entity level — the company files its tax return and claims the 80% deduction on the relevant income line. There is no separate application form for routine IP Box usage; however, the company must maintain documentation showing that the IP asset is a qualifying asset (patent, copyright-protected software, or utility model) and that the income is properly attributable to that asset.

What IP Qualifies for the Cyprus IP Box?

Qualifying assets: patents registered in any jurisdiction; software protected by copyright, including SaaS products and mobile applications; non-obvious, useful, and novel inventions meeting the patentability threshold even if not yet formally patented; and utility models. The category of copyright-protected software is particularly valuable because it covers almost all commercial software products without requiring formal registration.

Non-qualifying assets: trademarks, service marks, and brand names; marketing-related intangibles such as customer lists and distribution agreements; designs (including registered industrial designs); and business methods that are not embodied in patentable technology. The exclusion of trademarks is OECD-mandated under the Modified Nexus Approach — the IP Box is designed to reward R&D-intensive activity, not brand value accumulation.

If a product bundles qualifying IP (e.g., patented technology embedded in a hardware device) with non-qualifying elements (branding, distribution), an income split is required to isolate the portion attributable to the qualifying IP. In practice, for pure software companies and patent-licensing entities, the entire net income from the relevant revenue stream typically qualifies.

The Modified Nexus Requirement

The Cyprus IP Box follows the OECD Modified Nexus Approach mandated by BEPS Action 5. This means the percentage of IP income eligible for the 80% deduction scales with the proportion of qualifying R&D expenditure incurred by the Cyprus entity relative to total R&D expenditure on developing that IP.

The nexus formula is: Nexus % = (Qualifying R&D expenditure / Total R&D expenditure) × 100. Qualifying expenditure includes: direct R&D costs incurred by the Cyprus company itself; R&D contracted out to unrelated third-party contractors (regardless of where the contractor is based). Non-qualifying expenditure includes: amounts paid to acquire the IP from a related or unrelated party (acquisition costs); R&D outsourced to related-party companies in any jurisdiction.

Example: A Cyprus company develops software in-house spending €200,000/year on salaries and third-party tools (qualifying), and pays a related offshore entity €50,000 for part of the R&D (non-qualifying). Total R&D = €250,000. Nexus % = 200,000 / 250,000 = 80%. The 80% nexus ratio is then multiplied by the qualifying income to arrive at the eligible amount. If net IP income is €500,000, only €400,000 (80%) enters the IP Box and receives the 80% deduction. Tax: €400,000 × 20% × 12.5% = €10,000 on the nexus-eligible portion, plus €100,000 × 12.5% = €12,500 on the non-nexus portion. Total: €22,500 on €500,000 = 4.5% blended rate.

For companies where all R&D is done in-house in Cyprus or contracted to unrelated third parties, the nexus ratio is 100% and the full 80% deduction applies to all qualifying IP income.

IP Box + Non-Dom = Maximum Tax Efficiency

The Cyprus IP Box applies at the corporate level. When the company shareholder is a Cyprus tax resident with Non-Dom status, dividends distributed from the IP Box company are subject to 0% income tax and only 2.65% GHS (General Healthcare System contribution, capped at an annual GHS base of €180,000). This creates one of the most efficient structures available in the EU for IP-intensive businesses.

Example: SaaS founder with €500,000/year in software licensing income. Without Cyprus IP Box (hypothetical high-tax country): 25% corporate tax on €400,000 net profit = €100,000 corporate tax; then 30% dividend tax on €300,000 net = €90,000. Total: €190,000 on €500,000 = 38% combined rate. With Cyprus IP Box + Non-Dom: Company pays 2.5% effective on €400,000 net IP profit = €10,000 corporate tax. Remaining €390,000 distributed as dividend. Non-Dom owner: 0% income tax + 2.65% GHS on dividends up to €180,000 cap = €4,770. Total tax: €14,770 on €500,000 gross = approximately 3% combined effective rate.

The GHS cap of €180,000 applies to all GHS-subject income in aggregate per year. For founders receiving large dividends, contributions above that base are exempt. This cap makes the Non-Dom + IP Box combination particularly powerful at higher income levels where the GHS contribution becomes proportionally negligible.

Key Facts 2026

| Effective tax rate on qualifying IP income | ~2.5% |

| Exemption on qualifying net profit | 80% |

| Corporate tax on remaining 20% | 15% |

| Qualifying assets | Patents, software copyright, plant variety rights, similar IP |

| Non-qualifying (excluded) | Trademarks, brands, marketing intangibles, know-how |

| OECD nexus requirement | R&D expenditure must be by the qualifying company |

| Effective rate vs EU competitors | Cyprus 2.5% vs Netherlands 9% vs Luxembourg 6.8% |

| Combined with Non-Dom | Dividends still at 2.65% GHS only |

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Get personalised guidance on Non-Dom status, company formation, and your specific tax situation from an experienced Cyprus tax advisor.

Cyprus IP Box: NEXUS Ratio - Worked Example (3 Scenarios)

The NEXUS approach limits the IP Box benefit to income proportional to genuine R&D activity. Outsourcing development to related parties reduces the benefit significantly.

| Variable | A - All R&D in-house | B - Mixed (50% in-house) | C - Mostly outsourced |

|---|---|---|---|

| Qualifying IP income | €500,000 | €500,000 | €500,000 |

| Qualifying R&D costs (in-house / unrelated) | €200,000 | €100,000 | €20,000 |

| Total R&D costs (incl. related-party outsourcing) | €200,000 | €200,000 | €200,000 |

| NEXUS ratio | 100% (200/200) | 50% (100/200) | 10% (20/200) |

| Qualifying profit (income x 80% exemption) | €400,000 | €400,000 | €400,000 |

| Exempt profit (qualifying x NEXUS) | €400,000 | €200,000 | €40,000 |

| Taxable profit remaining | €100,000 | €300,000 | €460,000 |

| Corporation tax at 15% | €15,000 (3% effective) | €45,000 (9% effective) | €69,000 (13.8% effective) |

Takeaway: The 2.5% effective rate (Scenario A) requires all R&D to be performed by the Cyprus company itself or contracted to unrelated third parties. Related-party outsourcing (e.g. to a parent company) does not qualify for the enhanced NEXUS ratio and will push the effective rate toward 15%.

Frequently Asked Questions

What is the effective tax rate under the Cyprus IP Box?

Does software qualify for the Cyprus IP Box?

Is the Cyprus IP Box OECD compliant?

Do trademarks and brands qualify for the Cyprus IP Box?

What is the nexus ratio and how does it affect the IP Box benefit?

Can a non-Cyprus resident own a Cyprus IP Box company?

Is there a minimum substance requirement for the Cyprus IP Box?

How does the Cyprus IP Box compare to the Netherlands innovation box?

Who qualifies for the Cyprus IP Box?

Does the Cyprus IP Box apply to SaaS software?

Is the Cyprus IP Box OECD compliant?

Can I transfer IP from my current company to a Cyprus company to use the IP Box?

Related Guides

Sources

Cyprus Income Tax Law - Article 9B (IP Box provisions). OECD BEPS Action 5 modified nexus approach. Cyprus Tax Department guidance on qualifying IP assets. Updated: April 2026.

Our Cyprus IP Box Calculator lets you model your effective rate based on your qualifying IP income and nexus ratio, and compare it against other EU IP Box regimes including Luxembourg (5.2%), Ireland (6.25%) and the Netherlands (9%).

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Free newsletter

What do you want to hear about?

No spam. Unsubscribe any time.