Quick Answer

Cyprus Non-Dom status exempts qualifying residents from SDC on worldwide dividends (0% vs 5% for regular residents), interest (0% vs 30%), and rental income (0% for all residents from 2026). The only remaining tax on dividend income for Non-Doms is 2.65% GHS. Rental income remains subject to standard income tax (0-35%) regardless of Non-Dom status. Non-Dom duration: 17 years, renewable.

Non-Dom Status in Cyprus: What It Is and Why It Matters

The Cyprus Non-Domiciled status is a cornerstone of taxes in Cyprus, exempting qualifying residents from Special Defence Contribution on dividends, interest, and rental income. Understanding the Cyprus non domiciled status rules is essential for anyone considering relocation.

Last updated:

Non-Dom Tax Savings Calculator

See how much less tax you'd pay on dividends under Cyprus Non-Dom status.

*Cyprus Non-Dom effective rate = 2.65% GHS on dividends + ~15% corporate tax already paid at company level. Rates are indicative. Individual circumstances may vary.

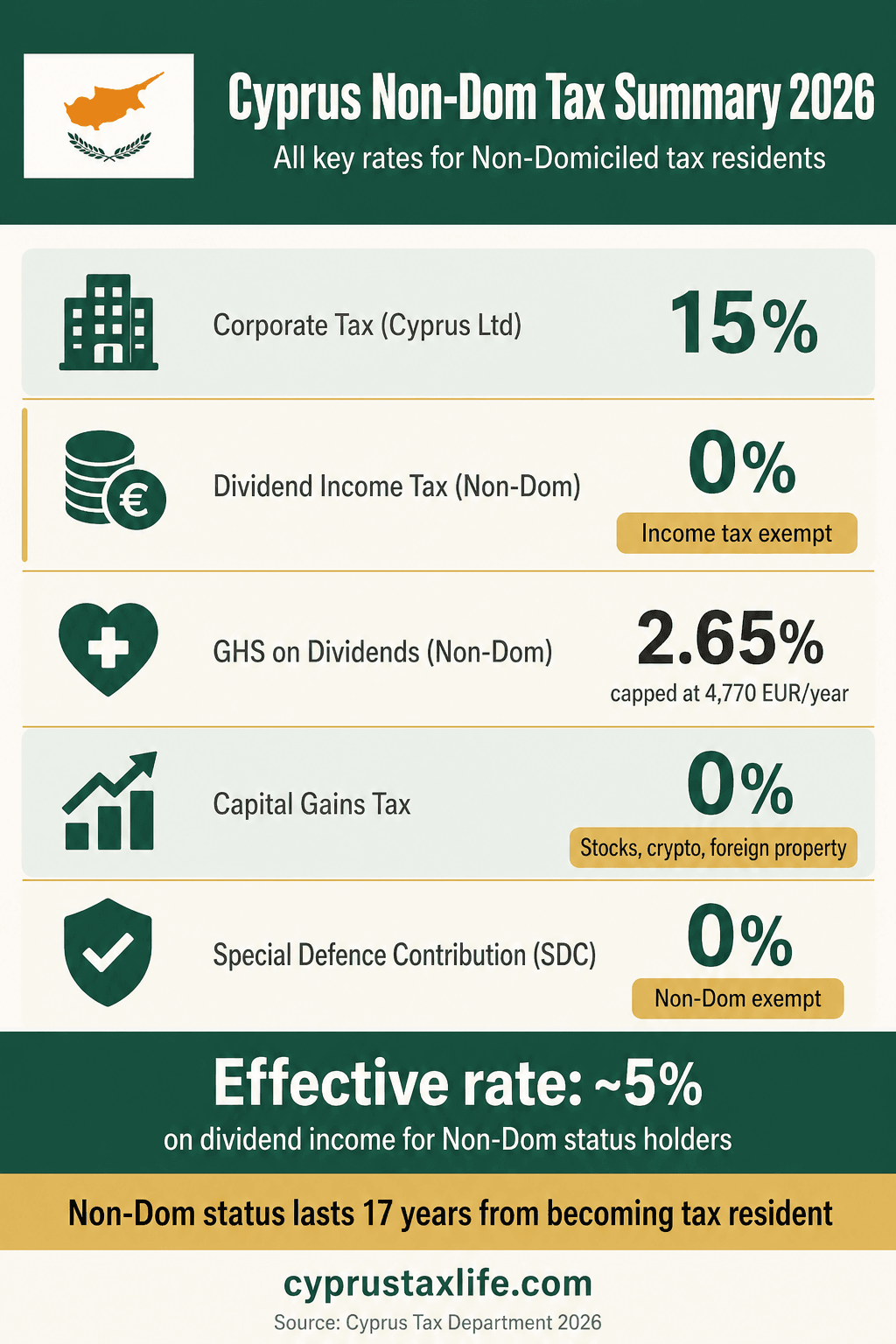

Key Facts 2026

| Status duration | 17 years from date of acquisition |

| Dividend income tax | 0% (Non-Dom exempt from SDC/Defence contribution) |

| GHS on dividends | 2.65% only |

| GHS annual cap | EUR 4,770/year (max income base EUR 180,000) |

| Capital gains on shares | 0% |

| Inheritance tax | 0% |

| Minimum days in Cyprus | 60/year (under 60-day rule) or 183/year (standard) |

| Eligibility | Not Cyprus tax resident in 17 of the preceding 20 years |

Free, no commitment

Moving to Cyprus or opening a company?

Tell us your situation and we'll connect you with our specialist expat advisory in Cyprus: Non-Dom tax, company setup and residency, done for you. Free consultation, no commitment.

Get personalised guidance on Non-Dom status, company formation, and your specific tax situation from an experienced Cyprus tax advisor.

Non-Dom vs Domiciled vs Non-Resident: Tax Comparison (2026)

| Income Type | Non-Dom | Domiciled | Non-Resident |

|---|---|---|---|

| Dividends | 2.65% GHS only | 5% SDC + 2.65% GHS | 0% |

| Interest | 2.65% GHS only | 30% SDC + 2.65% GHS | 0% |

| Rental Income | Income tax (0-35%) | Income tax (0-35%) | Income tax (0-35%) |

| Capital Gains (securities) | 0% | 0% | 0% |

| Employment | 0-35% progressive | 0-35% progressive | 0-35% progressive |

| Effective Rate (dividend focus) | ~5% | ~15-20% | 0% (no Cyprus tax) |

SDC = Special Defence Contribution. GHS = General Healthcare System. Non-Dom exemption lasts up to 17 years. Source: Cyprus Tax Department, updated 2026.

Non-Dom at a Glance

- 0%

- SDC on dividends with Non-Dom

- 17years

- Maximum duration of Non-Dom status

- 2.65%

- Only GHS contribution on dividends

- €2,200

- Total tax residency setup cost

What Is Non-Dom Status?

Non-Domiciled status is a legal classification under Cyprus tax law. It is separate from tax residency. A person can be a tax resident of Cyprus but not domiciled there.

You are considered non-domiciled if:

- You were not born in Cyprus (your domicile of origin is elsewhere)

- You have not lived in Cyprus for 17 or more years out of the last 20

In practice, virtually every foreigner who moves to Cyprus automatically qualifies for Non-Dom status.

Automatic for Foreigners

Non-Dom is not something you apply for separately. It is determined automatically based on your domicile of origin when you register as a tax resident.

What Does Non-Dom Save You?

The main benefit is exemption from the Special Defence Contribution (SDC). Without Non-Dom status, Cyprus tax residents pay SDC on passive income:

- Dividends: 5% SDC

- Interest income: 30% SDC

- Rental income: 3% SDC (on 75% of gross rent)

With Non-Dom status, all of these rates drop to 0%. The only remaining contribution is the GHS levy of 2.65% on dividends and interest.

Example: 50,000 EUR in Dividends

- With Non-Dom: 0% SDC + 2.65% GHS = 1,325 EUR total tax

- Without Non-Dom: 5% SDC + 2.65% GHS = 3,825 EUR total tax

Annual savings: 2,500 EUR on dividends alone.

Only 2.65% on Dividends

Non-Dom status eliminates the 5% SDC on dividends. The only remaining charge is the 2.65% GHS healthcare contribution.

Not sure where you stand? Use the Cyprus Non-Dom Eligibility Checker to get a quick answer based on your specific situation.

Have questions about your situation?

Every case is different. Get personalized guidance for your specific tax and relocation needs.

Our guides cover the essentials, but every situation is different. Professional advisors in Cyprus can help you set up the optimal structure for your specific circumstances.

How Do You Get Non-Dom Status in Cyprus?

The entire process, including immigration registration and tax setup, costs approximately 2,200 EUR through a professional advisor.

Immigration Registration

Obtain your yellow slip (MEU1/MEU3 certificate) from the Civil Registry and Migration Department.

- EU citizens: MEU1 form

- Non-EU citizens: MEU3 form

Tax Number (TIN)

Apply for a Tax Identification Number at the local Tax Department. Required for all tax filings.

Non-Dom Declaration

Submit the declaration of domicile status as part of your tax registration, confirming your domicile of origin is outside Cyprus.

Health Insurance

Register with GESY (the national health system) or obtain private insurance to complete your residency setup.

How Long Does Non-Dom Last?

Non-Dom status lasts for a maximum of 17 years from the date you first become a tax resident of Cyprus. After 17 years of continuous tax residency, you are considered domiciled and will start paying SDC on passive income.

For most expatriates, 17 years provides more than enough planning horizon.

17 Year Window

Starts from your first year as a Cyprus tax resident. No renewal needed during this period.

What Taxes Do You Still Pay Under Non-Dom?

Non-Dom only exempts you from SDC. These taxes still apply.

Employment Income (PAYE)

Salary is still taxed at progressive rates: 0% up to €19,500, then 20-35% on higher amounts.

Corporate Tax

Your company still pays 15% corporate tax on net profits. Non-Dom is a personal, not corporate, benefit.

GHS Healthcare Levy

The 2.65% GHS contribution still applies to dividends, interest, salary, and other income.

Social Insurance

Both employer and employee Social Insurance contributions still apply to salary payments.

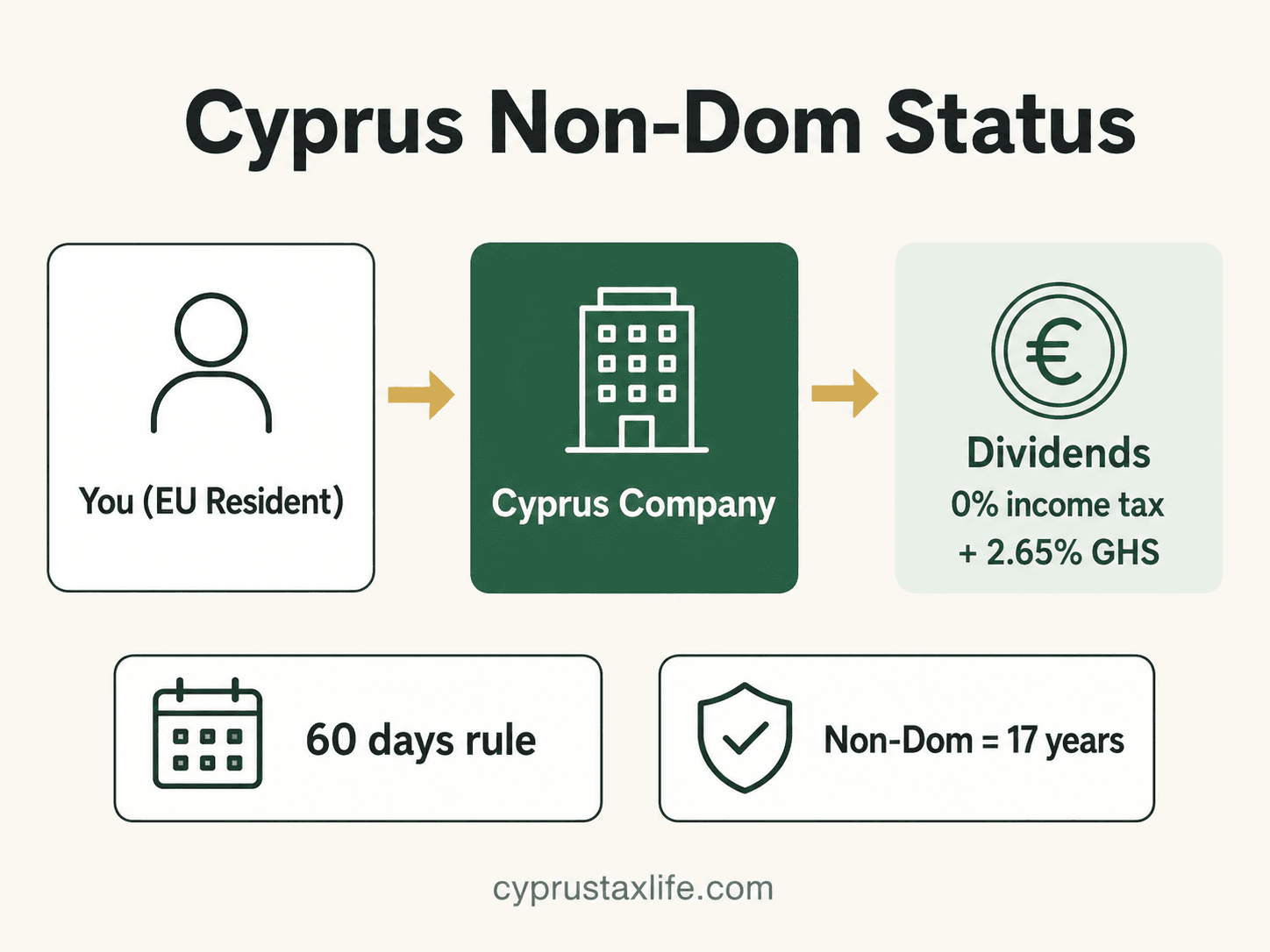

How Do Non-Dom and the 60-Day Rule Work Together?

The most tax-efficient setup for international professionals combines:

- 60-day rule for tax residency with minimum physical presence in Cyprus

- Non-Dom status for SDC exemption on dividends and interest

- Cyprus Ltd company with low salary + dividend distribution

This combination allows professionals to maintain a mobile lifestyle while benefiting from one of the lowest effective tax rates in the EU.

Download the Full Non-Dom Guide as PDF

Free , no email required. Includes all tax rates, examples, qualification criteria, and the EU regime comparison.

Frequently Asked Questions

Do I need to apply separately for Non-Dom status?

Yes, you declare your domicile status during tax registration. Non-Dom status is determined by your domicile of origin at that point, not through a separate application.

Can I lose Non-Dom status?

Yes, after 17 years of continuous tax residency in Cyprus, Non-Dom status automatically expires. You can also voluntarily end it by changing your domicile before the 17-year period ends.

Does Non-Dom apply to salary income?

No. Non-Dom exempts you from SDC on foreign-sourced investment income only, not salary. You pay full SDC on employment income regardless of Non-Dom status. Non-Dom provides no tax relief on wages or salaries earned in Cyprus or abroad.dividends, and interest income. Employment income remains subject to normal PAYE income tax rates.

Is Non-Dom available to EU and non-EU citizens?

Non-Dom status is available to both EU and non-EU citizens. Qualification depends on domicile of origin, not nationality or EU citizenship. Any foreigner not born in Cyprus can qualify.

How much does the Non-Dom setup cost?

Non-Dom registration costs approximately EUR 2,500-3,500 in professional fees, plus EUR 500-1,000 for government filings and documentation. The full tax residency setup including immigration advice runs EUR 4,000-6,000 total depending on complexity and service provider.yellow slip, TIN, Non-Dom declaration, and health insurance) costs approximately 2,200 EUR through a professional advisor.

What are the Cyprus tax rates for foreigners with Non-Domiciled status?

Non-Domiciled (Non-Dom) status in Cyprus provides an effective tax rate of approximately 5% on total income. Dividends face 2.65% GHS only, with zero SDC. Interest income is SDC-exempt. Salary income uses standard brackets (0% to 22,000 EUR). Corporate profits are taxed at 15%. This regime applies to qualifying foreign residents and offers significant EU tax advantages for eligible individuals.dividend tax guide for detailed calculations.

How does the Cyprus Non-Domiciled status differ from other EU tax regimes?

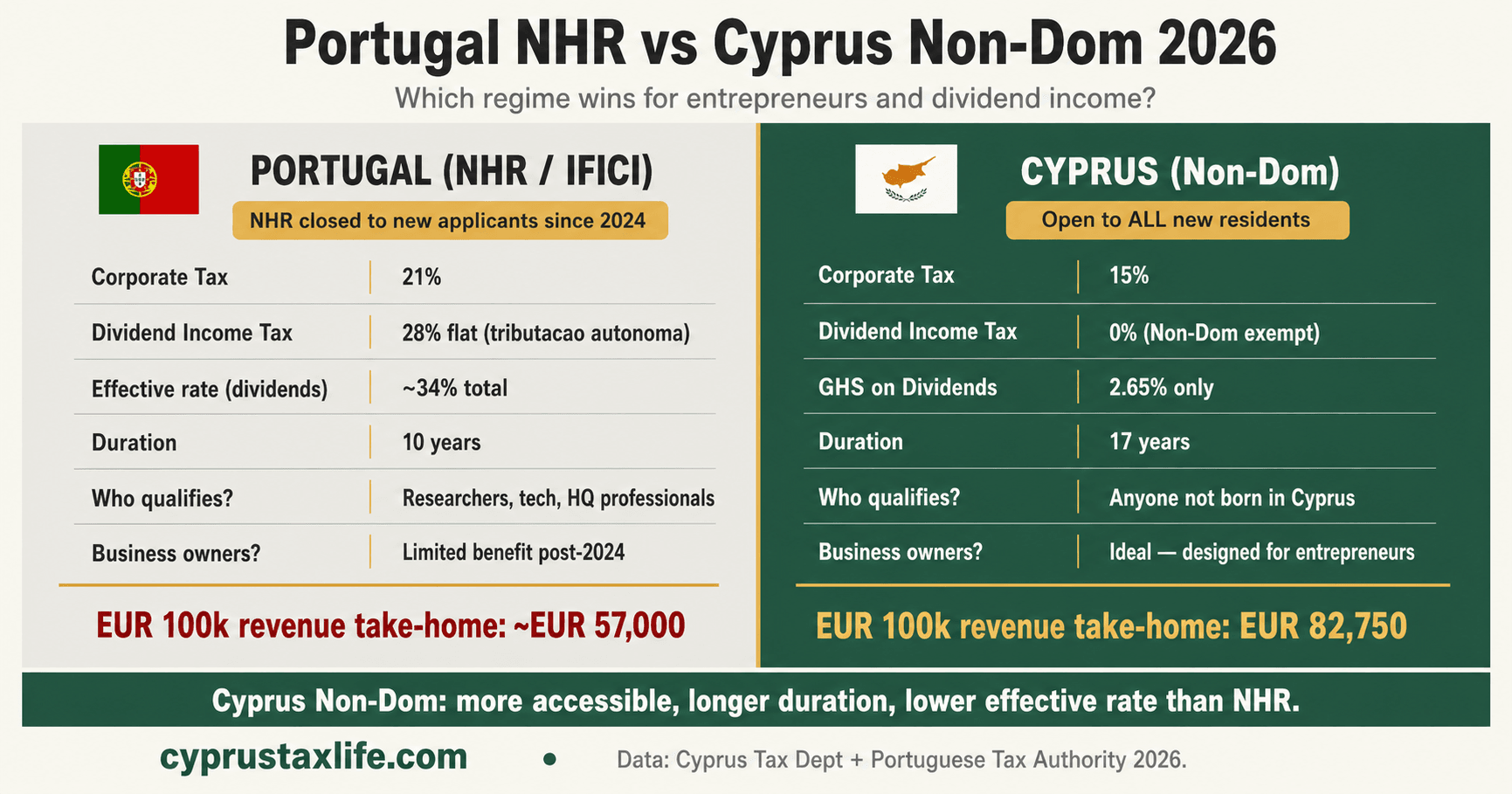

Cyprus Non-Dom status requires no minimum income or wealth requirement, unlike Portugal's ended NHR, Italy's flat tax (EUR 200,000 minimum), or Greece's regime (EUR 100,000 minimum). It's automatic for most foreigners, free to obtain, and lasts up to 17 years. Any foreigner not previously domiciled in Cyprus qualifies for preferential tax rates under this regime.

How long does it take to obtain Non-Dom status in Cyprus?

There is no separate application for Non-Dom status. You obtain it automatically when you register as a Cyprus tax resident and meet the domicile requirements. The key step is registering at the Tax Department and receiving your TIC (Tax Identification Number), which typically takes 2 to 4 weeks.

Does Cyprus Non-Dom status affect my home country tax obligations?

No, Cyprus Non-Dom status only affects your Cyprus tax liability. Your home country tax obligations depend on that country's residency rules and its double tax treaty with Cyprus. Consult tax advisors in both jurisdictions before relocating to ensure compliance.

Can I use Cyprus Non-Dom status if I have a UK Ltd, US LLC, or foreign company?

**Yes.** Cyprus Non-Dom residents pay no income tax or SDC on foreign company dividends, regardless of incorporation location. Only the 2.65% GHS contribution applies (capped at EUR 4,770 annually). This covers UK Ltd, US LLC, and all other foreign structures, making Cyprus ideal for existing business owners.

What is the 17-year limit for Cyprus Non-Dom status?

You can benefit from Cyprus Non-Dom status for a maximum of 17 consecutive years. After this period, you're deemed to have acquired domicile of choice in Cyprus and lose the exemption. This rarely affects most expats in practice.

Is rental income also tax-free under Cyprus Non-Dom status?

Rental income in Cyprus is taxable under progressive rates (0% up to EUR 22,000, then up to 35%) for all residents, including Non-Doms. The 3% SDC on rental income was abolished from 1 January 2026. GHS contributions of 2.65% apply on rental income up to the EUR 180,000 cap. Non-Dom status does not exempt rental income from taxation.

What happens to my Non-Dom status if I leave Cyprus and return later?

Your Non-Dom clock pauses when you leave Cyprus; the 17-year maximum only counts years as a tax resident. If you return, the domicile of origin test resets and you may re-qualify as Non-Dom, depending on your domicile history. Seek specialist advice before any exit.

Do I qualify for Non-Dom status if I only spend 60 days in Cyprus?

No, 60 days alone is insufficient for Non-Dom status. You must spend at least 183 days in Cyprus during the tax year to establish tax residency and qualify for Non-Dom benefits. The 60-day rule applies only to other tax residency scenarios, not Non-Dom eligibility.

To use the 60-day rule you must: spend at least 60 days in Cyprus during the tax year, not be tax resident in any other country (i.e. not spend more than 183 days elsewhere), maintain a permanent home in Cyprus (owned or rented), and have a business or employment connection to Cyprus.

Once you are a Cyprus tax resident under either the 183-day or 60-day rule, you can apply for Non-Dom status if you have not been domiciled in Cyprus for at least 17 of the last 20 years.

Can I combine Non-Dom status with the 50% salary exemption?

No, you cannot combine Non-Dom status with the 50% salary exemption. Non-Dom residents are taxed on worldwide income at approximately 5% effective rate, while the 50% exemption applies only to regular residents. You must choose one regime: either Non-Dom status for all income, or regular residency with the 50% salary exemption on employment income only.

The 50% salary exemption applies to individuals who earn more than EUR 55,000 per year and were not tax residents of Cyprus in the 3 years prior to starting employment there. It exempts half of your employment income from personal income tax for up to 17 years.

Non-Dom status, on top of that, exempts you from the Special Defence Contribution (SDC) on dividends (17%) and interest (30%). So if you draw dividends from your Cyprus company in addition to a salary, you pay 0% SDC on those dividends.

The two benefits are independent and fully compatible. You can receive both simultaneously if you meet the conditions for each.

Want this reviewed for your situation?

Book a 1-on-1 call with someone who has relocated to Cyprus and set up a company — Non-Dom, residency, company formation and real numbers.

Does Cyprus Tax Worldwide Income?

Cyprus taxes all individuals who establish tax residency here on their worldwide income. This is the standard rule: once you spend 183 days or qualify under the 60-day rule, your global earnings fall within the Cyprus tax net.

However, Non-Dom status significantly changes the outcome for passive income. Under Non-Dom, dividends, interest, and rental income from foreign sources are exempt from Special Defence Contribution (SDC). From 2026, SDC on dividends for domiciled residents is 5%. Non-Dom residents pay 0% SDC and only 2.65% GHS (capped at EUR 180,000 of income), bringing the effective rate on foreign passive income to approximately 5% overall.

Income Tax Still Applies to Employment and Pensions

Non-Dom status does not exempt employment income or pension income from Cyprus progressive income tax. Salaries, freelance fees, and foreign pensions are taxed at 0% up to EUR 22,000, then 20% to 35% on higher bands. The Non-Dom advantage applies exclusively to investment income: dividends, interest, and (pre-2026) rental income from abroad.

Cyprus vs Worldwide Taxation Countries

Unlike the United States, which taxes its citizens on worldwide income regardless of residence, Cyprus follows a residency-based system. Only tax residents are subject to Cyprus tax. Non-residents pay Cyprus tax only on Cyprus-source income such as rental income from Cyprus property or employment carried out in Cyprus.

Use our Cyprus Dividend Tax Calculator to see your exact net income as a Non-Dom dividend recipient. If you plan to take a salary instead of dividends, the Cyprus Salary Calculator shows your take-home pay after the progressive income tax brackets.

2026 Reform: What the SDC Rate Cut Means for Non-Dom Residents

Cyprus reduced the Special Defence Contribution (SDC) rate on dividends from 17% to 5% effective 1 January 2026. For Non-Dom residents, this change is irrelevant: Non-Dom status provides a full SDC exemption (0%) regardless of the rate applying to domiciled residents.

The reform actually widens the Non-Dom advantage for anyone comparing options. Previously, domiciled residents paid 17% SDC on dividends. From 2026, they pay 5%. Non-Dom residents continue to pay 0%. If you become domiciled after 17 years, the SDC you will face drops from 17% to 5% — a meaningful reduction in the long-term tax cost of staying in Cyprus.

No action is required from current Non-Dom residents. The SDC exemption is automatic and continues for the remainder of your 17-year window.

Frequently Asked Questions

How do I apply for non-domicile status in Cyprus?

Non-dom status is not a separate application - it is determined automatically based on your domicile of origin and years of Cyprus tax residency. If neither parent was domiciled in Cyprus, your domicile of origin is not Cyprus, and you automatically qualify as non-domiciled for the first 17 years of Cyprus tax residency.

There is no separate form to submit. When you register as a Cyprus tax resident (TIC registration at the Tax Department), you declare your domicile status on your annual tax return (IR1). Your tax adviser will note your non-dom status so the SDC exemption on dividends and interest is correctly applied from year one.

What is the difference between non-resident and non-domiciled in Cyprus?

These are two distinct legal concepts. Non-resident means you spend insufficient time in Cyprus to be a tax resident (under 60 days under the 60-day rule, or under 183 days under the standard rule). Non-residents pay Cyprus tax only on Cyprus-source income such as rental income from Cyprus property.

Non-domiciled means you are a Cyprus tax resident but your domicile of origin is not Cyprus. Non-doms pay Cyprus income tax on worldwide earned income but are exempt from SDC on dividends and interest, meaning dividends are effectively taxed only at 2.65% GESY. You must first be a Cyprus tax resident to benefit from non-dom status.

Does Cyprus tax worldwide income?

What Is Cyprus Non-Dom Status? (Plain Language Guide)

Cyprus Non-Domiciled (Non-Dom) status is a tax classification available to people who move to Cyprus and become tax residents here, provided they were not born in Cyprus and have not lived here for most of their life. Non-Dom is not a visa, it is a tax status that you acquire automatically once you are a Cyprus tax resident and have not been tax resident in Cyprus for 20 of the last 25 years before applying.

The main benefit: Non-Dom residents pay zero Special Defence Contribution (SDC) on dividends and interest. SDC is 17% for domiciled Cyprus residents, meaning Non-Doms save 17 percentage points on dividend income. Combined with the 2.65% GHS contribution, Non-Doms pay a total of 2.65% on dividends vs 19.65% for domiciled residents.

Who Qualifies for Cyprus Non-Dom Status?

- Not born in Cyprus and both parents are non-Cypriot

- Have not been Cyprus tax resident for 20 or more of the last 25 years

- Are currently a Cyprus tax resident (via 183-day rule or 60-Day Rule)

- Have not acquired a Cyprus domicile of origin or choice

In practice, almost every foreigner who relocates to Cyprus qualifies for Non-Dom status in their first year of residency, and can maintain it for up to 17 years.

Non-Dom vs Regular Cyprus Tax Resident

A regular Cyprus tax resident (domiciled) pays: income tax at 0-35% on employment, 5% SDC on dividends, 2.65% GHS on dividends. A Non-Dom Cyprus tax resident pays: income tax at 0-35% on employment (same), 0% SDC on dividends (exempted), 2.65% GHS on dividends. The savings are entirely on passive income, dividends, interest and rental income are where Non-Dom makes the difference.

How to Apply for Non-Dom Status

Non-Dom status is declared on your annual income tax return (IR1). You tick the Non-Dom checkbox on the form. There is no separate application or certificate, the status is self-reported and verified by the Tax Department when processing your return. Keep supporting evidence: passport (showing non-Cypriot nationality), rental agreement or property title, and prior years' tax returns from your previous country of residence showing you were not Cyprus tax resident.

Free, no commitment

Moving to Cyprus or opening a company?

Tell us your situation and we'll connect you with our specialist expat advisory in Cyprus: Non-Dom tax, company setup and residency, done for you. Free consultation, no commitment.

Related resources

Non-Dom case studies

Before/after numbers for German, UK, Spanish, Dutch, US entrepreneurs

Non-Dom for freelancers

How contractors and independent consultants structure their taxes in Cyprus

Non-Dom for SaaS founders

Optimal structure for SaaS and digital product revenue under Non-Dom

Cyprus vs UK post-Non-Dom

UK abolished its Non-Dom regime — what Cyprus offers instead

Cyprus vs Germany

~5% effective rate in Cyprus vs 48%+ in Germany for entrepreneurs

Cyprus vs Spain

5% Cyprus Non-Dom vs 54% autonomo — the numbers side by side

Free newsletter

What do you want to hear about?

No spam. Unsubscribe any time.