Quick Answer

The Cyprus 60-day rule allows foreign nationals to become Cyprus tax residents with a minimum of 60 days physical presence per year. To qualify, you must spend no more than 183 days in any single other country, maintain a permanent residence in Cyprus, and have a business connection or employment in Cyprus. When combined with Non-Dom status, the effective tax rate on dividends drops to approximately 2.65%.

60 Day Rule Cyprus: Tax Residency Without Living Full-Time

Cyprus allows tax residency with just 60 days of physical presence per year, one of the most flexible rules among taxes in Cyprus that attracts remote workers worldwide.

Last updated:

60-Day Rule Eligibility Checker

Tick each condition you meet to see if you qualify for Cyprus tax residency under the 60-day rule.

Key Facts 2026

| Minimum days in Cyprus | 60 days per tax year |

| Maximum days in any single other country | 183 days per tax year |

| Cyprus permanent home required | Yes (owned or rented) |

| Business or employment in Cyprus required | Yes (Cyprus-based entity) |

| Not tax resident in any other country | Yes (in the same tax year) |

| Result | Full Cyprus tax resident status |

| Compatible with Non-Dom | Yes - combine for 0% dividend tax |

| Tax year | 1 January to 31 December |

| Standard 183-day rule alternative | Yes - can use either rule |

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Get personalised guidance on Non-Dom status, company formation, and your specific tax situation from an experienced Cyprus tax advisor.

60-Day Rule at a Glance

- 60days

- Minimum physical presence required

- 5

- Conditions that must all be met

- 2017

- Year the rule was introduced

- <183days

- Cannot spend this many days elsewhere

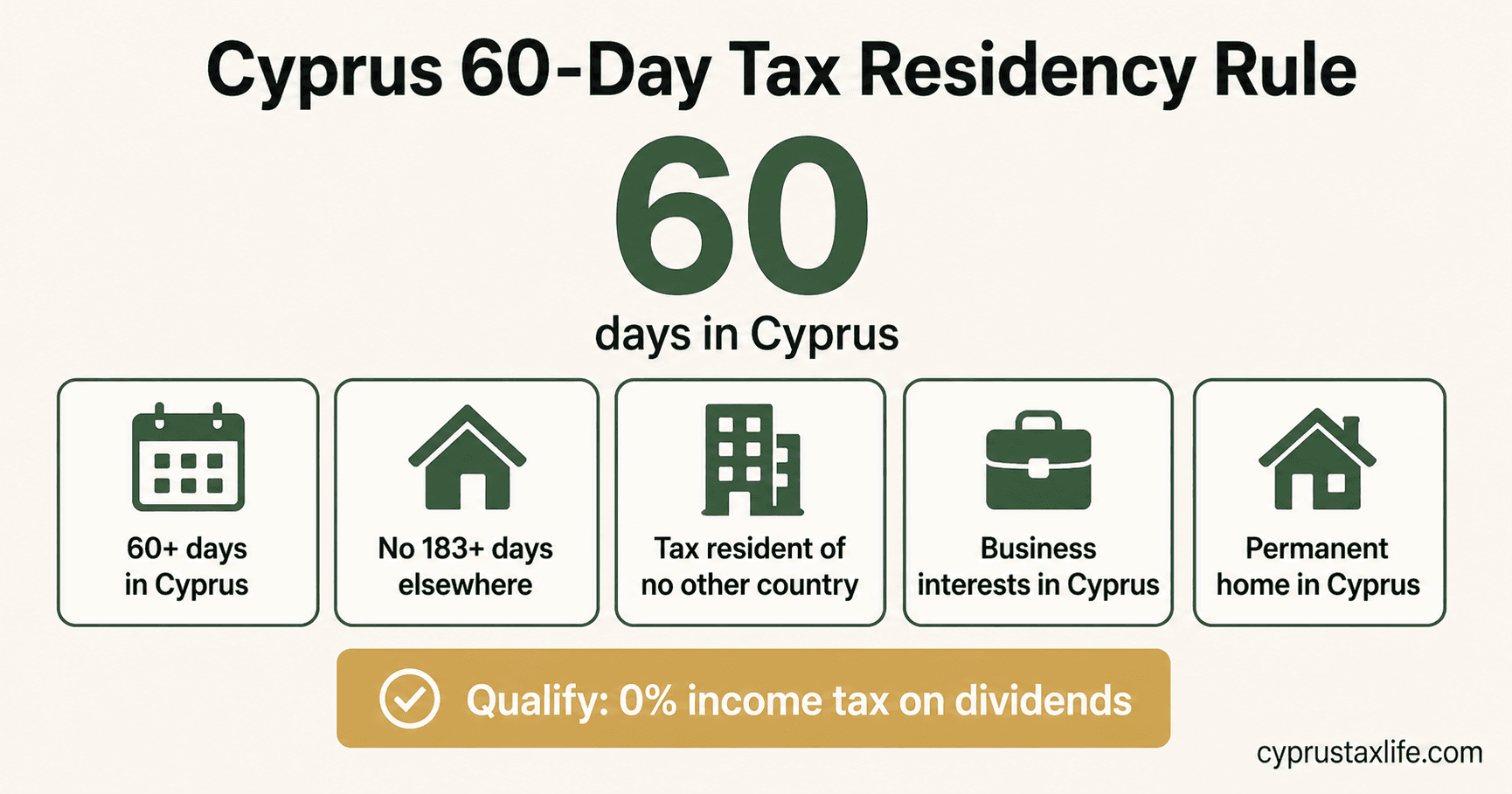

What Is the 60-Day Rule?

The 60-day rule is an alternative path to Cyprus tax residency that allows qualifying individuals to become tax residents with just 60 days of physical presence per year, instead of the standard 183 days.

Introduced in 2017, this rule makes Cyprus one of the most flexible jurisdictions in the EU for international professionals, digital nomads, and business owners who travel frequently.

Under standard international tax rules, you become a tax resident by spending 183 or more days in a country. Cyprus offers an alternative: if you meet specific conditions, you can qualify with only 60 days.

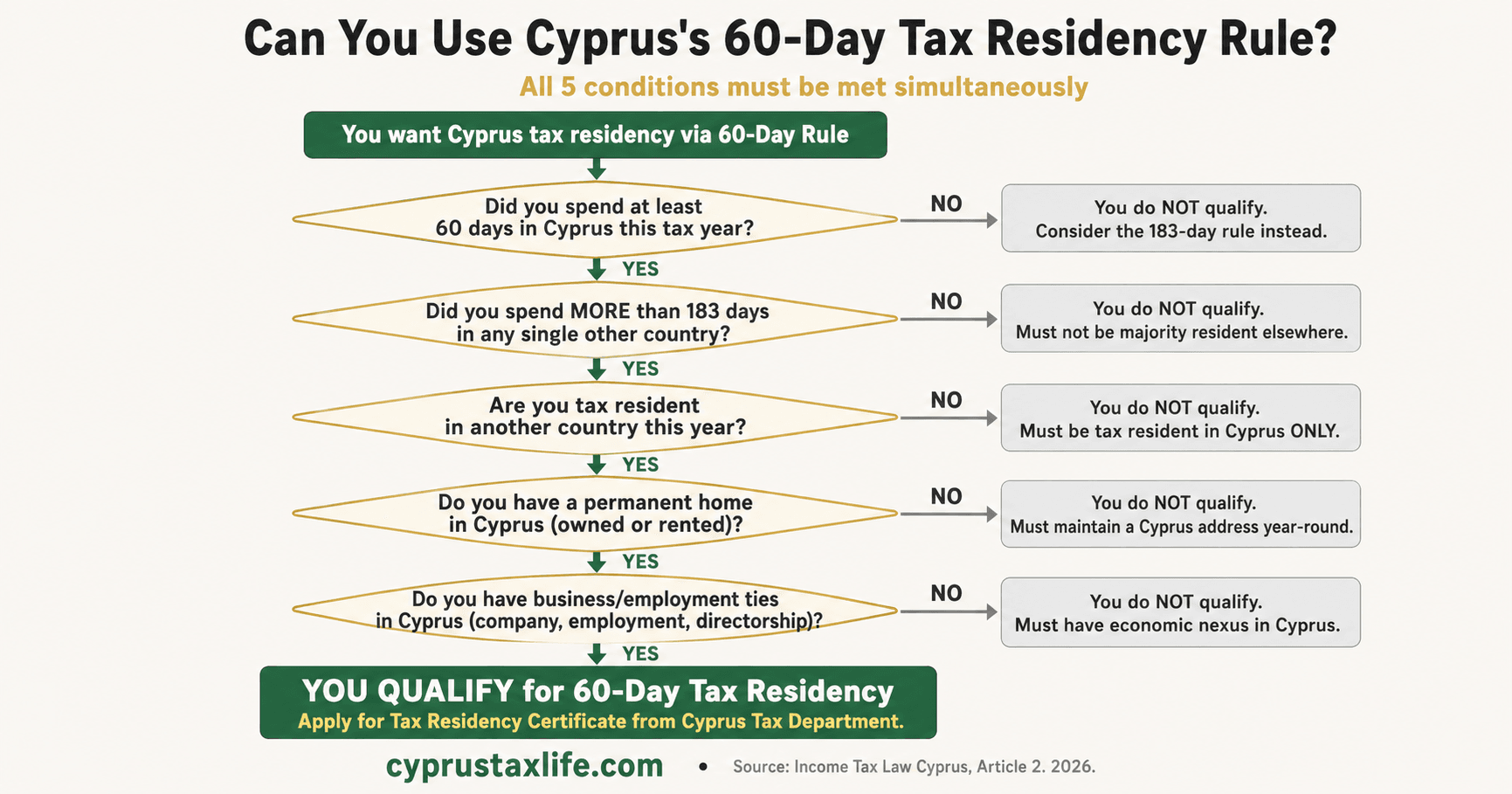

What Are the Requirements for the 60-Day Rule?

To qualify under the 60-day rule, all five conditions must be satisfied in the same calendar year.

Spend at least 60 days in Cyprus

Physically present for a minimum of 60 days during the tax year (January 1 to December 31). Days of arrival and departure each count as one day.

Not be a tax resident of any other country

Do not spend 183 or more days in any other single country. Spread your time to avoid triggering tax residency elsewhere.

Have a business connection to Cyprus

Be a director of a Cyprus company, be employed by a Cyprus-registered company, or own a business registered in Cyprus.

- Director of a Cyprus Ltd (most common)

- Employee of a Cyprus-registered company

- Owner of a Cyprus-registered business

Maintain a permanent residence in Cyprus

Own or rent a property in your name. A formal rental contract is sufficient. The property must be available year-round.

Not be employed outside Cyprus

No employment with a non-Cyprus company. However, being a director of your own Cyprus company and working remotely for clients abroad is acceptable.

What Documentation Do You Need for the 60-Day Rule?

To prove compliance with the 60-day rule, maintain the following:

- Rental contract or property deed in your name

- Company registration certificate (Cyprus Ltd)

- Director appointment documents

- Yellow slip (MEU1/MEU3 immigration certificate)

- Travel records: flight tickets, boarding passes, passport stamps

- Utility bills or bank statements showing activity in Cyprus

Keep Everything

The Tax Department may request proof of your 60+ days at any time. Organized records prevent problems during audits.

Have questions about your situation?

Every case is different. Get personalized guidance for your specific tax and relocation needs.

Our guides cover the essentials, but every situation is different. Professional advisors in Cyprus can help you set up the optimal structure for your specific circumstances.

Is the 60-Day Rule Right for You?

The 60-day rule is designed for specific profiles. Check which category fits your situation.

Ideal Candidates

- Remote workers with a Cyprus LtdServing international clients through your own company while maintaining flexibility.

- Digital nomadsWant tax residency without being tied to one location year-round.

- Frequent business travelersNeed an EU tax base but travel most of the year.

- Couples from high-tax countriesWant flexibility while benefiting from Cyprus tax advantages.

Not the Best Fit

- Employed by a foreign companyThe 60-day rule requires no employment with non-Cyprus companies.

- Spending 183+ days in another countryThat country may claim you as tax resident regardless of Cyprus arrangements.

- No business connection to CyprusA directorship, employment, or business ownership in a Cyprus entity is required.

What Mistakes Should You Avoid with the 60-Day Rule?

These errors can invalidate your 60-day rule claim and create tax problems.

Too Many Days Abroad

Spending 183+ days in any single country makes you tax resident there, even if you meet the 60-day requirement in Cyprus.

No Rental Contract

Living with friends or in an Airbnb does not satisfy the permanent residence requirement. You need a formal lease in your name.

Not Tracking Travel Days

Keep boarding passes, flight confirmations, and passport stamps. The Tax Department may ask for proof of your 60+ days.

No Cyprus Business Connection

You must be a director, employee, or owner of a Cyprus-registered entity. Remote work alone is not sufficient.

How Do the 60-Day Rule and Non-Dom Work Together?

The most tax-efficient setup for international professionals combines three elements:

- 60-day rule establishes Cyprus tax residency with minimal physical presence

- Non-Dom status eliminates SDC on dividends and interest (automatic for non-Cypriots)

- Cyprus Ltd provides low corporate tax (15%) with dividend distributions at only 2.65%

Together, these create one of the most tax-efficient frameworks available in the EU for self-employed professionals and remote workers.

Cyprus 60-Day Rule in 2026: What Actually Changed

The 60-day rule itself has not changed in 2026. The five conditions set out in Section 2 of the Income Tax Law (as amended by Law 119(I)/2017) remain intact. What changed in 2026 is not the residency rule but the tax rates that apply once you qualify: corporate tax rose from 12.5% to 15% under OECD Pillar Two, and the Special Defence Contribution (SDC) rate on dividends for domiciled residents was reduced from 17% to 5%. For Non-Dom residents, SDC remains 0%.

The official source for the 60-day rule requirements is the Cyprus Tax Department (Ministry of Finance). The legal basis is Section 2(2) of the Income Tax Law (Cap. 297) as amended by Law 119(I)/2017, which introduced the alternative 60-day residency test.

Cyprus 60-Day Rule: Full Requirements for 2026

All of the following must be met in the same calendar year: (1) At least 60 days of physical presence in Cyprus. The day of arrival counts; the day of departure does not. (2) You are NOT a tax resident in any other country during that year. (3) You do not spend more than 183 days in any single other country. (4) You maintain a permanent residence in Cyprus - either owned property or a long-term rental agreement available for your use throughout the year. (5) You have a business activity, employment contract, or directorship in a Cyprus tax-resident company that remains active at the end of the tax year.

60-Day Rule vs 183-Day Rule in 2026: Which Should You Choose?

The 60-day rule is designed for internationally mobile professionals who cannot or do not want to spend more than half the year in any single country. It offers Cyprus tax residency with only 60 days of presence. The 183-day rule requires spending more than 183 days per year in Cyprus but has fewer conditions. Both rules give access to the same Non-Dom benefits, including 0% SDC on worldwide dividends and interest for up to 17 years.

Practically, the 60-day rule suits entrepreneurs running businesses internationally, investors who travel frequently, and professionals with clients in multiple countries. The 183-day rule suits retirees, employees of Cyprus companies, and anyone who intends to make Cyprus their primary base of operations.

How Are Days Counted for the Cyprus 60-Day Rule?

Day of arrival in Cyprus counts as a day in Cyprus. Day of departure from Cyprus does not count. A full day in Cyprus means physically present at midnight local time. Days of travel outside Cyprus during which you return the same day count as days in Cyprus. The Tax Department counts calendar days, not working days. Keeping a travel log with boarding passes and hotel receipts is the safest approach for borderline cases.

Frequently Asked Questions

Can I work remotely for clients while using the 60-day rule?

You can work remotely for international clients through your Cyprus Ltd company while using the 60-day rule. The restriction applies only to employment by a non-Cyprus company, not to serving foreign clients directly.

Do weekends and holidays count toward the 60 days?

Yes, weekends and public holidays count toward the 60 days. Any day you are physically present in Cyprus counts, including partial days (arrival and departure days each count as one full day).

What happens if I only spend 59 days in Cyprus?

Spending 59 days in Cyprus disqualifies you from tax residency under the 60-day rule that year. You must reach either 60 consecutive days or 183 days total to qualify as tax resident in Cyprus for that calendar year.

Can my spouse also use the 60-day rule?

Both spouses can qualify under the 60-day rule if each independently meets all five conditions, since each person is assessed individually.

Do I need to notify the Tax Department about the 60-day rule?

Yes, you must declare your 60-day rule residency status during tax registration and annual filing. Your tax advisor can submit this notification as part of your standard tax compliance process.

Has the Cyprus 60-day tax residency rule changed in 2026?

What are the Cyprus 60-day tax residency rule requirements for 2026?

Are there any updates to the Cyprus 60-day rule I should know about before applying in 2026?

How are days counted for the Cyprus 60-day rule?

Days are counted from arrival (inclusive) to departure (exclusive). Your arrival day counts as a day in Cyprus; your departure day does not. Transit days through Cyprus without stopping do not count. Keep boarding passes, hotel receipts, and entry stamps to prove your days if the tax authority questions your position.

What counts as permanent residence in Cyprus for the 60-day rule?

A property where you have the right to live qualifies as permanent residence, whether owned, rented, or made available to you. It need not be your only residence. A standard one-year rental contract typically satisfies this requirement.

What happens if I do not meet any Cyprus tax residency rule?

You are not a Cyprus tax resident if you meet neither the 183-day nor the 60-day rule in that year. Tax liability shifts to your country of stronger ties or where you spent most time. Highly mobile individuals may face gaps in tax residency that some jurisdictions treat as taxable presence. Consult a local tax advisor if this applies to you.

What is the difference between the 60-day rule and the 183-day rule?

The 183-day rule makes you a tax resident by spending over 183 days in Cyprus annually with no other conditions. The 60-day rule requires only 60+ days in Cyprus but adds four conditions: you must not be tax resident elsewhere, not exceed 183 days in any other country, conduct business or hold a director role in Cyprus, and maintain permanent residence here. The 60-day rule suits frequent travellers; the 183-day rule is simpler.

Does the 60-day rule give the same tax benefits as the 183-day rule?

No, the 60-day rule and 183-day rule follow different tax frameworks. The 60-day rule qualifies you for the Non-Dom regime with preferential rates (~5% effective on foreign income). The 183-day rule establishes standard tax residency. Both give access to the Non-Dom regime once you qualify, but the 60-day route is specifically designed for that preferential treatment, while 183-day residency follows the standard residency path.

Do I need to register with the Cyprus Tax Department if I use the 60-day rule?

Registration with the Cyprus Tax Department and obtaining a Tax Identification Code (TIC) are mandatory even if you use the 60-day rule. You must file an annual tax return and typically register through a local accountant or tax advisor with proof of meeting the 60-day conditions.

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Related resources

Tax residency rules table

183-day and 60-day rule side by side with all conditions

Case studies using 60-day rule

How real entrepreneurs structured their residency

Moving from the UK

UK-specific residency steps: timing, CGT window, pension implications

Moving from Germany

German exit tax, Wegzugsteuer, and the 60-day rule checklist

Non-Dom status guide

What you can claim once you are a Cyprus tax resident under 60-day rule

Tax residency FAQ

6 Q&As on day counting, permanent home, and business nexus

Free newsletter

What do you want to hear about?

No spam. Unsubscribe any time.