Quick Answer

Cyprus is a leading EU holding company jurisdiction due to its 0% withholding tax on dividends paid to foreign shareholders and participation exemption on dividends received from subsidiaries. Capital gains on the disposal of shares in subsidiaries are fully exempt. Combined with 65+ tax treaties and the EU Parent-Subsidiary Directive, Cyprus holding companies face no tax on dividend flows in most structures.

Cyprus Holding Company: Why It's Europe's Top Choice

Cyprus combines 0% withholding tax on dividends paid out, 0% capital gains tax on share disposals, 15% corporate tax, and 60+ tax treaties into one of the most efficient holding structures in the EU.

Last updated:

0% Withholding Tax on Dividends to Non-Residents: How It Works

Cyprus imposes zero withholding tax on dividends paid by a Cyprus company to non-resident shareholders, with no minimum ownership threshold and no double tax treaty required. This applies whether the shareholder is an individual or a foreign holding company, and whether they are EU or non-EU resident.

Compare this to the EU average withholding rate of 15-25% on outbound dividends. Ireland charges 25% (dividend withholding tax), Netherlands 15% (reduced by treaty), Luxembourg 15%. In practice this means that a Cyprus holding company can distribute 100% of after-tax profits to its shareholders without any further tax leakage at the Cyprus level.

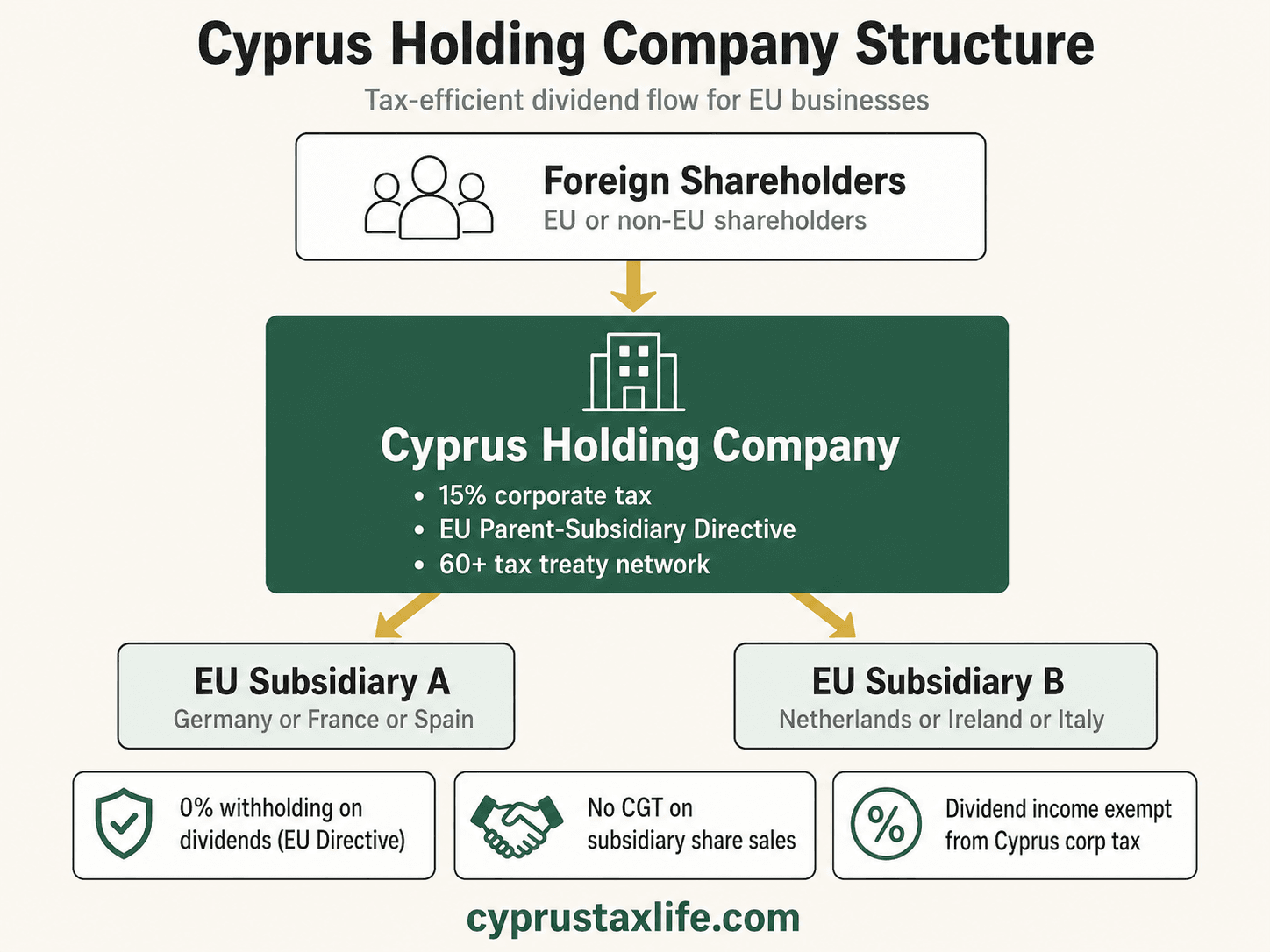

Typical Cyprus Holding Structure

- Cyprus HoldCo receives dividends from operating subsidiaries, 0% tax under participation exemption (if conditions met)

- Cyprus HoldCo distributes to shareholder (individual or foreign HoldCo), 0% WHT

- Total Cyprus-level tax leakage on dividend flow: 0%

- Capital gains on sale of Cyprus HoldCo shares: 0% (unless underlying assets are Cyprus real estate)

Substance Requirements for Non-Dom Shareholders

For the Cyprus Non-Dom regime to apply to the individual shareholder, they must qualify as Cyprus tax resident (minimum 60 days/year under the 60-Day Rule) and must not be domiciled in Cyprus. Non-Dom shareholders pay 2.65% GHS on dividends received, there is no income tax, no SDC and no further withholding at source.

Cyprus vs Other EU Holding Jurisdictions

Ireland: Strong treaty network but 25% DWT; requires substantive management activity. Netherlands: 0% under participation exemption but 15% on qualifying distributions without treaty; substance requirements are strict. Luxembourg: 15% WHT on dividends; reduced under treaty but complex anti-avoidance rules. Cyprus: 0% WHT on all outbound dividends; participation exemption requires only that the subsidiary is not primarily a Cyprus real estate company; relatively low substance requirements (resident director, board minutes, economic activity).

Key Facts 2026

| Dividend withholding tax to non-residents | 0% |

| Participation exemption on incoming dividends | Yes (conditions: 1%+ holding, not passive investment) |

| Capital gains on share disposal | 0% |

| Corporate tax rate | 15% |

| Double tax treaties | 65+ countries |

| EU Parent-Subsidiary Directive | Applies - 0% WHT on intra-EU dividends |

| Minimum substance | Board meetings in Cyprus, local directors, management decisions |

| IP Box compatible | Yes - 2.5% on qualifying IP income held by the holding company |

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Frequently Asked Questions

What is the withholding tax on dividends paid from a Cyprus holding company?

Is there capital gains tax when selling shares in a Cyprus company?

What is the participation exemption in Cyprus?

Does a Cyprus holding company need substance?

Can non-residents own a Cyprus holding company?

How does the Cyprus holding company combine with Non-Dom status?

What is the corporate tax rate for a Cyprus holding company in 2026?

How long does it take to set up a Cyprus holding company?

What is the notional interest deduction (NID) in Cyprus and how does it reduce corporate tax?

How does the Cyprus IP Box work and what intellectual property qualifies?

Does Cyprus have transfer pricing rules and what documentation is required?

What are the real annual costs to run a Cyprus holding company?

Can a Cyprus holding company hold shares in a UAE or Indian subsidiary tax-efficiently?

Related Guides

Sources

Cyprus Companies Law (Cap. 113). Cyprus Income Tax Law - participation exemption provisions. 2026 Cyprus Tax Reform. Updated: April 2026.

Dividend Participation Exemption: Full Conditions and How the 80% Rule Works

Cyprus applies a dividend participation exemption that exempts qualifying dividend income from corporate tax. The mechanics work as follows: 80% of qualifying dividends received by a Cyprus company are exempt from the 15% corporate tax, resulting in a maximum effective tax rate of 3% on that income (15% × 20%). In practice, most holding structures are designed so that dividends flow through a Cyprus HoldCo that qualifies fully for this exemption, meaning the effective burden is minimal even before factoring in the Non-Dom overlay at shareholder level.

To qualify for the exemption, the dividend must be received from a company in which the Cyprus HoldCo holds at least 1% of the share capital. There is no minimum holding period requirement, the 1% threshold is the primary gateway. Crucially, the exemption is not automatic: it is denied if the subsidiary is tax-resident in a jurisdiction with a corporate tax rate below 6.25% (i.e., half of Cyprus's 12.5% historical rate, note that the reference threshold has not yet been updated to reflect the 2025 rate increase to 15%, so practitioners verify case by case with the Tax Department). Dividends from subsidiaries in EU member states, the UK, UAE, and most OECD jurisdictions clear this test with no difficulty.

The anti-avoidance carve-out is the second condition: the exemption is denied if more than 50% of the paying entity's income derives from investment income (interest, royalties, dividends) AND that income was taxed at a low effective rate at source. This is the 'passive income originating from investments' test. A Cyprus HoldCo receiving dividends from an operating company, one that makes and sells goods or delivers services, is almost never caught by this rule. The risk arises only in artificially layered holding chains where a sub-HoldCo at an intermediate level collects purely passive investment returns.

Practical scenario: A founder incorporates a Cyprus HoldCo that owns 100% of a German GmbH generating EUR 1 million profit. The GmbH pays EUR 850,000 in dividends after German corporate tax. Under the participation exemption, 80% of EUR 850,000 (EUR 680,000) is exempt. The remaining 20% (EUR 170,000) is subject to Cyprus corporate tax at 15%, yielding a Cyprus-level tax of EUR 25,500, an effective rate of 3% on the gross dividend received. At shareholder level, if the founder is Non-Dom, dividends distributed from the Cyprus HoldCo are subject to only 2.65% GHS (capped at EUR 180,000 annual GHS base), meaning dividends above EUR 180,000 at shareholder level bear zero further tax.

Cyprus IP Box: Holding Intellectual Property at a 3% Effective Rate

Cyprus operates an OECD-compliant IP Box (also called the Innovation Box) that provides an 80% exemption on qualifying IP income. With the standard corporate rate at 15%, the effective tax rate on qualifying IP profits is 3% (15% × 20%). Qualifying income includes royalties, licensing fees, gains from the disposal of qualifying IP assets, and income embedded in the price of goods or services where the value is attributable to the underlying IP. This makes Cyprus one of the most competitive IP holding locations in the EU.

Qualifying intellectual property under the Cyprus IP Box must be a patented invention, a copyrighted software program, or a utility model, not simply a trademark or brand. The nexus approach (mandated by OECD BEPS Action 5 and adopted in Cyprus law) means the exemption scales with the proportion of qualifying R&D expenditure incurred by the Cyprus holding company relative to overall expenditure on developing that IP. If the Cyprus entity outsourced all R&D to a related party abroad, the nexus fraction is low and the exemption is reduced proportionally. Companies that conduct genuine R&D in Cyprus, or outsource R&D only to unrelated third parties, can achieve the full 80% exemption.

A common structure: a tech founder sets up a Cyprus company that commissions software development from a third-party agency in Eastern Europe (unrelated party, so fully qualifying spend). The Cyprus company holds the copyright to the resulting software and licenses it to clients globally. Revenue of EUR 500,000/year flows into the Cyprus entity. After allowable expenses of EUR 100,000, net IP profit is EUR 400,000. The 80% exemption shelters EUR 320,000; only EUR 80,000 is taxable at 15%, generating a tax bill of EUR 12,000, an effective rate of 3%. The remaining EUR 388,000 after tax is distributable as a dividend, and a Non-Dom shareholder pays only 2.65% GHS on the dividend (capped at EUR 180,000 GHS base), making the combined rate extraordinarily low.

The IP Box also applies to capital gains on the disposal of qualifying IP assets. If the Cyprus holding company sells its software copyright or patent portfolio, 80% of the gain is exempt and only 20% is taxed at 15%. This is distinct from Cyprus's general CGT exemption (which applies to shares, not IP directly), and it specifically covers the disposal of the IP asset itself, a critical planning point when founders structure an exit through an IP holding company rather than a share sale.

Notional Interest Deduction: Tax-Free Returns on Equity Capital

Cyprus introduced the Notional Interest Deduction (NID) in 2015 to provide relief on equity financing equivalent to the deductibility that debt financing enjoys. The NID allows a Cyprus company to deduct a notional interest charge on 'new equity' introduced from January 1, 2015 onward. The deduction reduces taxable income at the corporate level, and in a holding company context it can effectively bring the corporate tax liability close to zero on profits up to the NID ceiling.

The NID rate is set annually at the 10-year government bond yield of the country where the new equity is invested plus a 3% premium, subject to a floor equal to the Cyprus 10-year government bond yield plus 3%. For practical purposes, the rate for equity invested in Cyprus operations has historically ranged between 4.5% and 6.5%. For example, if a Cyprus HoldCo receives EUR 2 million in equity and the applicable NID rate is 5%, the company can deduct EUR 100,000 per year from taxable income, a permanent annual deduction for as long as that equity remains in the company.

There is a critical cap on the NID: the deduction cannot exceed 80% of the company's taxable income in any given year (calculated before the NID deduction itself). This prevents the NID from creating a tax loss, though unused NID cannot be carried forward. In a holding company structure where a founder capitalises a Cyprus HoldCo with EUR 5 million of equity capital and the entity earns EUR 300,000 in dividends and royalties annually, the NID on EUR 5 million at 5% would be EUR 250,000, but it is capped at 80% of EUR 300,000, so EUR 240,000. The effective taxable income becomes EUR 60,000 and the tax bill EUR 9,000, an effective rate of 3% on EUR 300,000 gross income.

The NID and IP Box can be stacked in some configurations, though professional advice is essential to ensure the interaction is properly documented and no anti-avoidance provisions under the General Anti-Avoidance Rule (GAAR) are triggered. The NID is particularly powerful for founders who inject cash into a Cyprus holding company to fund downstream investments, since each fresh equity injection creates a new NID base that generates ongoing deductions for the life of the structure.

Cyprus as EU Gateway for Non-EU Subsidiaries: Structure and Treaty Network

Cyprus has an extensive double tax treaty network covering 68 countries, including Russia, Ukraine, India, China, South Africa, and all EU member states. For founders operating businesses in emerging markets, a Cyprus HoldCo serves as the EU-incorporated treaty-protected intermediary that receives dividends, royalties, and capital gains from subsidiaries in high-risk or high-withholding-tax jurisdictions and then re-distributes to shareholders in a tax-efficient manner. The combination of the participation exemption, CGT exemption on shares, and zero withholding tax on outbound dividends to Non-Dom shareholders makes Cyprus structurally superior to Luxembourg or the Netherlands for founders who are themselves relocating.

A typical structure for an Indian-origin founder: Indian OpCo (Pvt Ltd) → Cyprus HoldCo → Non-Dom founder in Cyprus. Under the India-Cyprus Double Tax Treaty (updated in 2016), withholding tax on dividends from India to Cyprus is 10%. The Cyprus HoldCo receives the dividend, applies the participation exemption (80% exempt), pays up to 3% effective corporate tax in Cyprus, and then distributes to the founder with only 2.65% GHS. Compare this to routing via a Dutch holding company, where the founder would need to pay Dutch personal income tax on distributions (box 2 rate is 24.5% for qualifying shareholdings above EUR 67,000 threshold in 2024) after having relocated to the Netherlands. Cyprus delivers the same EU-flag structure at a fraction of the ongoing tax cost.

For subsidiaries in the UAE (0% corporate tax), the UAE-Cyprus double tax treaty applies and dividends from UAE entities to Cyprus face zero UAE withholding tax. This creates a common clean structure: UAE OpCo (FZCO or LLC) → Cyprus HoldCo → Non-Dom founder. The Cyprus holding company holds the UAE shares, and any Cyprus-level corporate tax is minimised through the participation exemption. Capital gains on selling the UAE entity's shares are fully exempt from both CGT and corporate tax in Cyprus (shares disposal is outside the Cyprus CGT net entirely, and gains on disposal of securities, including shares, are explicitly exempt under the Income Tax Law).

Transfer pricing is a live consideration in all these structures. Cyprus adopted OECD-aligned transfer pricing rules effective from January 1, 2022. Intra-group transactions above EUR 750,000 per category per year require a Cyprus Local File. Transactions above EUR 5 million (goods) or EUR 1 million (services/royalties) per category per year also require a Master File. The Cyprus HoldCo must price intra-group loans, management services, and IP licences at arm's length, with contemporaneous documentation. Failure to maintain the required file exposes the entity to a EUR 5,000 penalty plus potential profit adjustments. In practice, a well-maintained HoldCo with a local accountant and at least a basic benchmarking report is fully compliant.

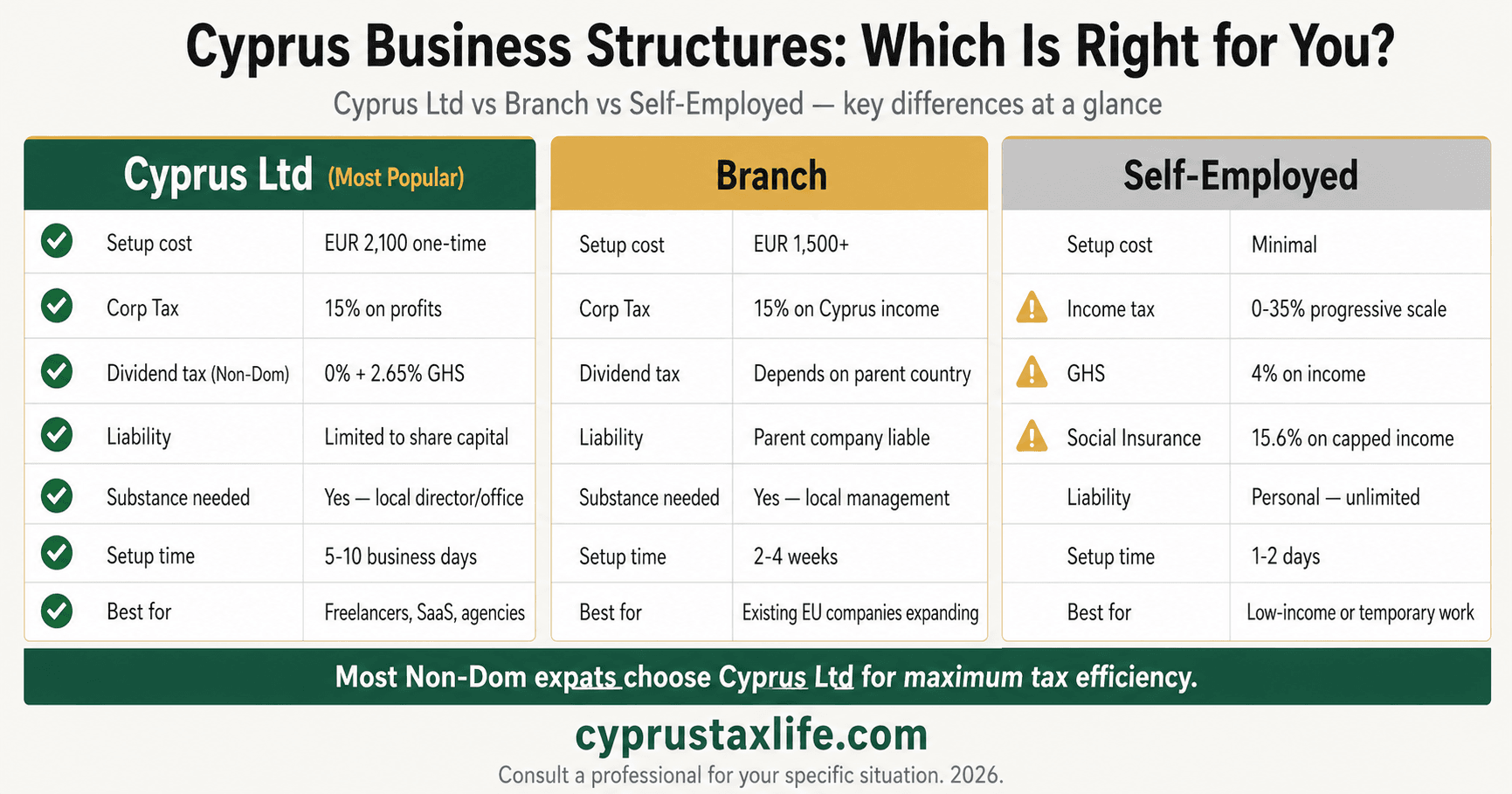

Setting Up and Running a Cyprus Holding Company: Costs, Substance, and Timelines

Incorporation of a Cyprus private limited company (Ltd) takes 5 to 10 business days through the Registrar of Companies when filed electronically by a licensed service provider. The Registrar fee is EUR 105 for a standard company with EUR 1,000 share capital. Professional fees for incorporation, including drafting the Memorandum and Articles, registered office for one year, nominee director (if needed for substance purposes), and company secretarial setup, typically range from EUR 1,500 to EUR 3,500 depending on complexity. Shelf companies (pre-incorporated entities with clean history) are available for EUR 1,800 to EUR 2,500 and can be transferred to the new owner's control within 24 hours.

Annual running costs for a Cyprus holding company with no employees are modest: registered office and company secretary EUR 600-1,200/year; annual return and statutory filings EUR 400-800/year; audit (mandatory for all Cyprus companies) EUR 1,500-4,000/year depending on transaction volume; accounting and bookkeeping EUR 800-2,000/year; annual levy to the government EUR 350/year. A lean holding company with straightforward share ownership and dividend pass-through can therefore be maintained for EUR 3,500 to EUR 7,000/year all-in, making it cost-effective even for structures holding assets worth EUR 100,000 or more.

Substance requirements have become materially more demanding since the EU Anti-Tax Avoidance Directives (ATAD I and II) and the EU Blacklist pressure on Cyprus tightened in 2019-2021. A Cyprus holding company that wishes to claim treaty benefits and resist challenge must demonstrate: (1) genuine decision-making conducted in Cyprus, board meetings held in Cyprus with a majority of Cyprus-resident directors, (2) proper books and records maintained in Cyprus, (3) a Cyprus bank account through which dividend and investment flows pass, and (4) at least one director with the knowledge and authority to independently manage the entity's affairs. The use of purely nominee directors signing resolutions from abroad is increasingly scrutinised and is no longer sufficient for a company claiming meaningful economic substance.

For founders who have relocated to Cyprus under the Non-Dom regime, substance is naturally satisfied: they are the controlling shareholder and director, they live in Cyprus, and board decisions are taken in Cyprus. For non-resident shareholders using a Cyprus HoldCo purely as an intermediary, a more deliberate substance programme is needed, engaging a local management company, appointing at least one independent Cypriot director with genuine oversight responsibilities, and ensuring management and control (the test used in most double tax treaties) demonstrably points to Cyprus. The cost of a professional independent director with real oversight duties ranges from EUR 2,000 to EUR 6,000 per year, which remains a small fraction of the tax savings achieved by the structure.

Related Guides

Best Holding Company Jurisdiction: Cyprus vs 4 EU Rivals [2026]

Cyprus Withholding Tax on Dividends to Non-Resident Shareholders

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Free newsletter

What do you want to hear about?

No spam. Unsubscribe any time.