Cyprus vs Germany 2026: Tax Comparison and How to Leave Correctly

German entrepreneurs pay 30% corp tax + 26.375% dividend tax = 48-50% on distributed profits. Cyprus: ~5%. EUR 38,500 saved per year on EUR 100,000. Full 2026 comparison including Wegzugsbesteuerung exit tax guide.

Last updated: 2026-06-01

Effective tax rate comparison

~40-47%

Germany

~5%

Cyprus Non-Dom

Which Is Better For You?

Remote worker / freelancer

Cyprus wins clearly. Germany's Gewerbesteuer + Körperschaftsteuer + Soli + 26.375% dividend tax = ~48-50% on distributed profits. Cyprus: ~5%. Annual saving: ~EUR 38,500 on EUR 100,000. For any entrepreneur extracting profit, Cyprus is far superior.

Holding company / IP owner

Cyprus wins. Germany's CFC rules (Hinzurechnungsbesteuerung) can attribute foreign income back if the foreign entity earns passive income with sub-25% rate — Cyprus at 15% sits above the German threshold, but genuine substance is required. For international holdings with real Cyprus activity, Cyprus is optimal.

Retiree / passive investor

Cyprus wins. Germany has no wealth tax (abolished 1997) but social security costs are high, and German Riester/Rürup pensions become taxable at up to 100% when drawn. Foreign-source pensions received as a Cyprus Non-Dom resident are exempt from Cyprus income tax.

Crypto investor

Cyprus wins. Germany exempts crypto gains after 1 year hold, but taxes them at up to 45% + Soli (47.5%) within the year. Cyprus: 8% flat for professional traders (2026), 0% for investors. For active traders, Cyprus is dramatically better.

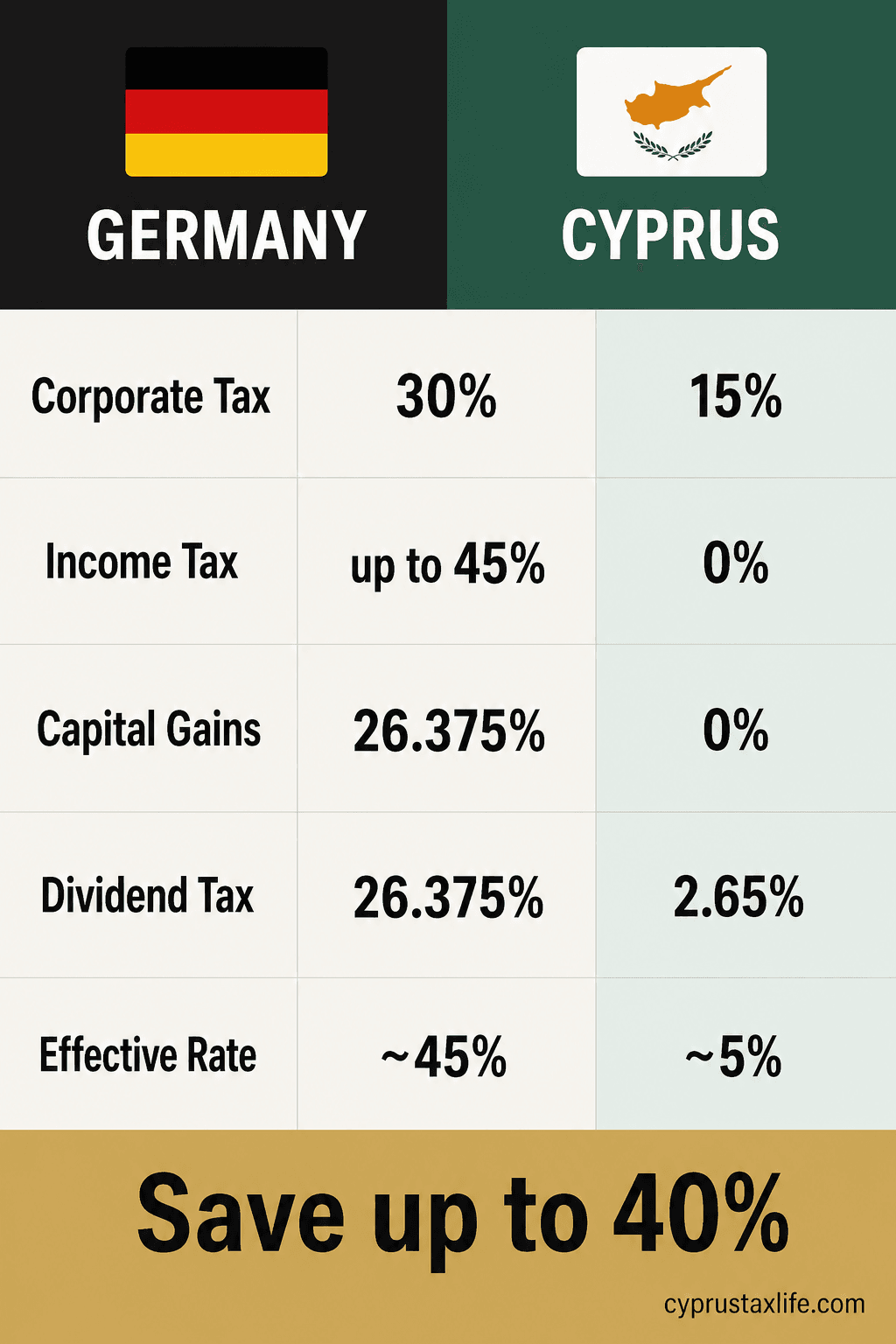

Tax Comparison: Germany vs Cyprus

| 🇩🇪 Germany | 🇨🇾 Cyprus (Non-Dom) | |

|---|---|---|

| Corporate tax | 15% + 5.5% Soli + ~14% trade tax = ~30% | 15% |

| Income tax | Up to 45% + 5.5% solidarity surcharge | 0% (dividends) |

| Capital gains tax | 25% + Soli (26.375% total) | 0% (no Cyprus property) |

| Dividend tax | 25% + Soli (26.375% total) | 0% income tax + 2.65% GHS |

| Wealth tax | None (abolished 1997) | None |

| Social contributions | ~20% employee + ~20% employer | ~4% on salary (capped) |

| Effective rate (entrepreneur) | ~40-47% | ~5% |

| VAT | 19% | 19% |

Tax Burden in Germany

Germany has one of the highest tax burdens in Europe for entrepreneurs and high earners. The income tax system is progressive with rates from 14% to 42%, with a top rate of 45% for income above EUR 277,826 (the so-called "Reichensteuer"). On top of this, the solidarity surcharge (Solidaritatszuschlag) of 5.5% applies to the income tax amount, effectively raising the top marginal rate to approximately 47.5%.

For companies, the burden is equally heavy. The corporate tax rate (Korperschaftsteuer) is 15%, but the solidarity surcharge adds 5.5% of that (0.825%), and the trade tax (Gewerbesteuer) varies by municipality, typically ranging from 14% to 17%. The combined corporate tax burden is approximately 30% in most German cities.

When profits are distributed as dividends, shareholders pay an additional 26.375% (25% capital gains tax plus solidarity surcharge). This creates a total tax burden on distributed corporate profits of approximately 48-50%.

Social security contributions are substantial: employees pay approximately 20% of gross salary (pension, health, unemployment, and care insurance), matched by the employer. Self-employed individuals in Germany must cover their own health insurance (approximately EUR 800-900/month) and can optionally contribute to the pension system.

Germany also enforces strict CFC (Controlled Foreign Corporation) rules, which can attribute foreign company income back to German shareholders if the foreign company is in a low-tax jurisdiction with an effective rate below 25%.

Why Cyprus is Better for Entrepreneurs

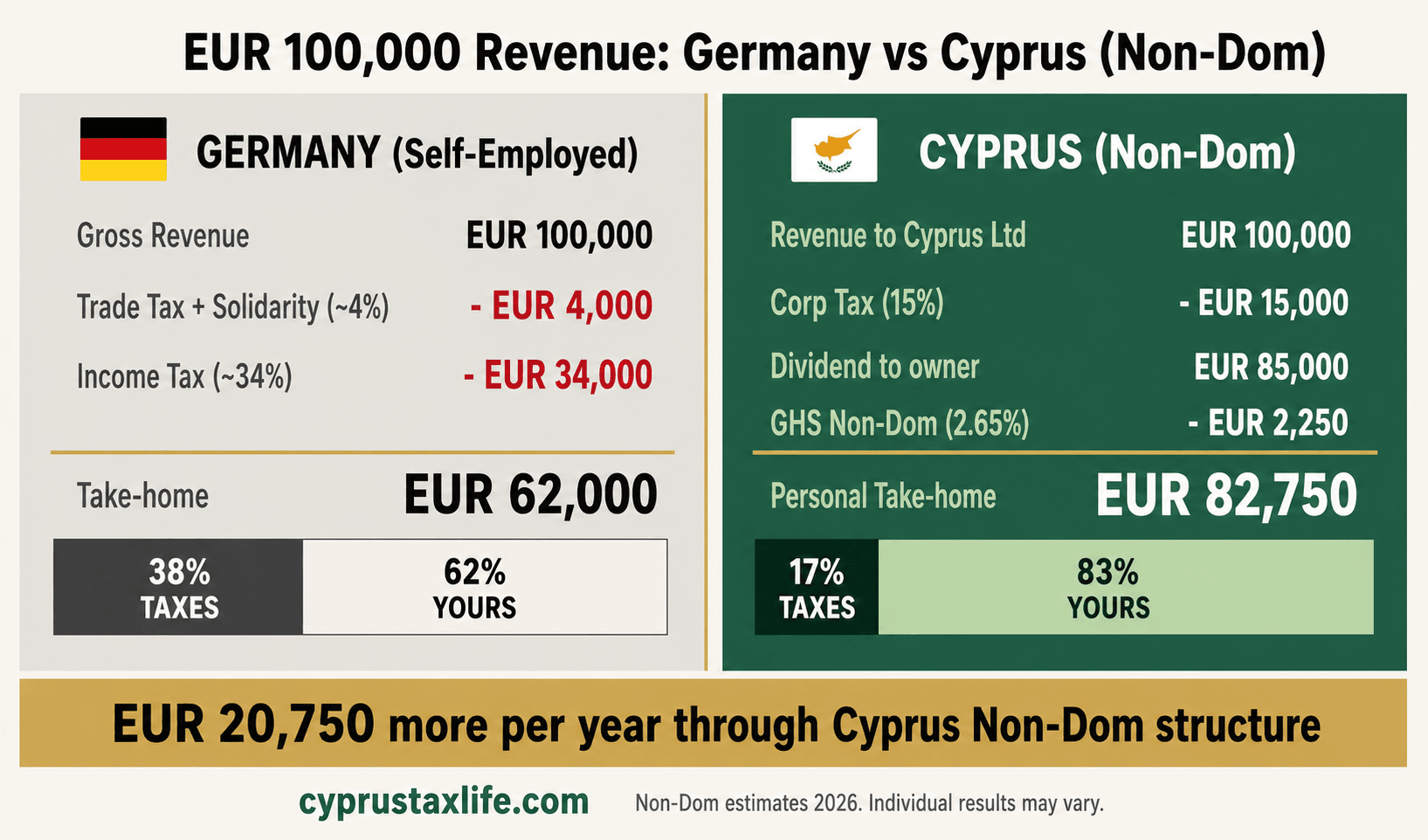

For German entrepreneurs, the contrast with Cyprus is stark. A Cyprus Ltd pays a flat 15% corporate tax with no surcharges and no trade tax. Under the Non-Dom regime, dividends from the company are exempt from income tax entirely, with only a 2.65% GHS contribution.

Using the optimized structure (Ltd company, low salary within the exempt threshold, dividends for the rest), the effective tax rate on EUR 100,000 of revenue is approximately 5%. Compare this to the 40-47% total burden in Germany, and the savings become substantial: over EUR 35,000 per year on the same revenue.

Cyprus is a fellow EU member state, which means German entrepreneurs can continue serving EU clients, maintain VAT registrations, and benefit from EU directives on parent-subsidiary distributions. The island also has a growing German-speaking community, particularly in Limassol and Paphos.

Important for German entrepreneurs: to avoid issues with German CFC rules, you must genuinely relocate your tax residency to Cyprus. This means actually living in Cyprus (or using the 60-day rule), managing your company from Cyprus, and properly deregistering in Germany (Abmeldung). Simply setting up a Cyprus company while remaining in Germany does not work and will be challenged by the Finanzamt.

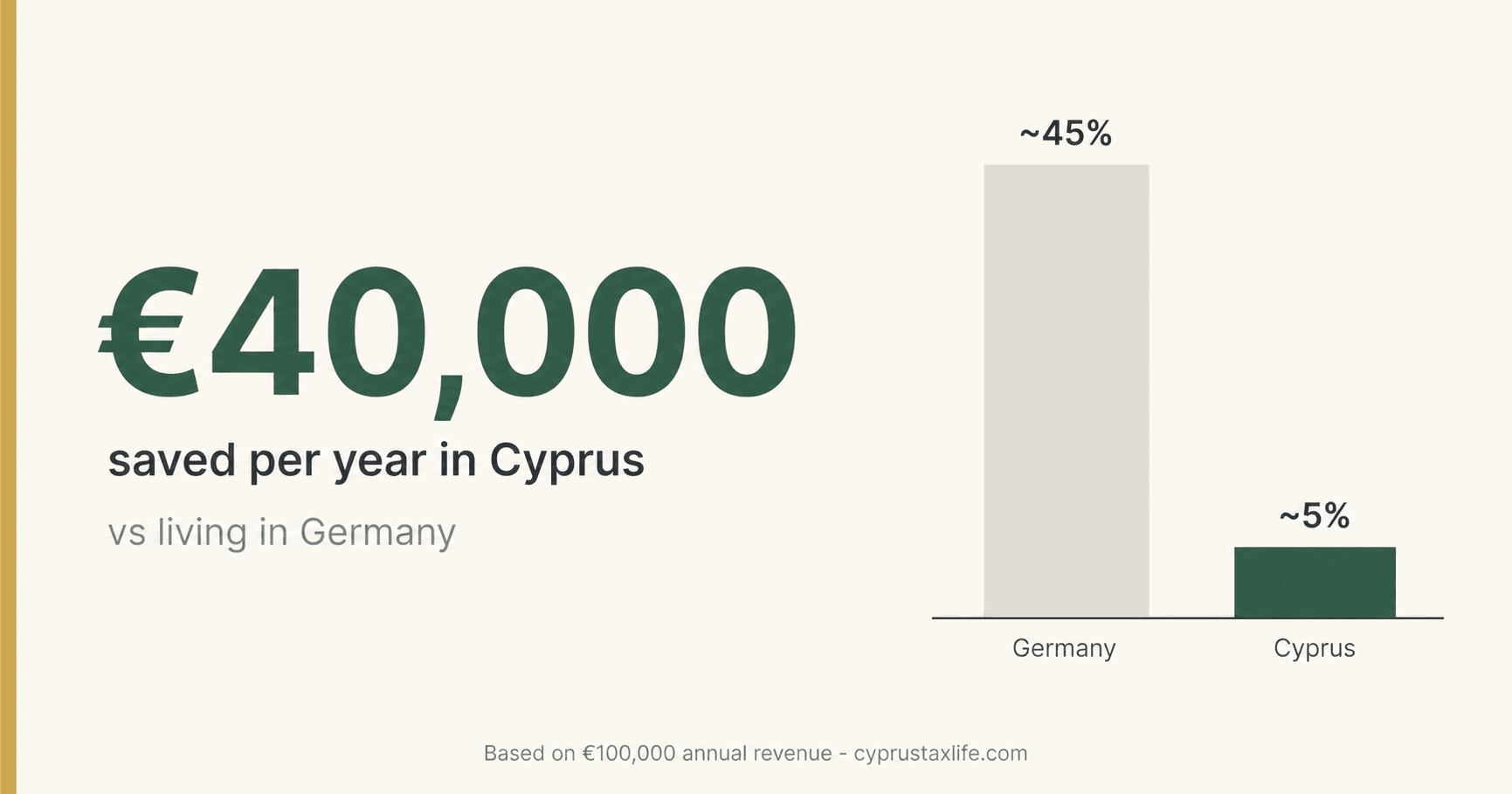

Tax Calculation: EUR 100,000

🇩🇪 Germany

🇨🇾 Cyprus (Non-Dom)

Annual savings moving to Cyprus

EUR 38,500

EUR 192,500 over 5 years

Double Tax Treaty: Germany - Cyprus

Germany and Cyprus have a double tax treaty in force since 1974 (revised in 2011). Key withholding rates: dividends 5% (if the beneficial owner holds at least 10% of capital) or 15% otherwise, interest 0%, royalties 0%. The treaty uses the OECD model and contains comprehensive tie-breaker rules based on permanent home, center of vital interests, habitual abode, and nationality. Pension income is generally taxable only in the state of residence under this treaty. Capital gains from shares are taxable in the state of residence of the seller, making Cyprus attractive since it does not tax gains on share disposals.

Exit Tax and Emigration from Germany

Germany has an exit tax (Wegzugsbesteuerung) under Section 6 AStG that triggers when a shareholder holding at least 1% of a corporation leaves German tax residency. The unrealized gains on these shares are deemed realized and taxed at the standard 26.375% rate. For moves within the EU/EEA, payment can be deferred interest-free in seven equal annual installments over seven years, with the obligation to file annual declarations. Importantly, if you return to Germany within seven years, the exit tax is reversed. If you sell the shares during the deferral period, the remaining tax becomes immediately due. Careful timing and potentially restructuring before emigration can help minimize this burden. Professional tax advice is essential for German entrepreneurs considering the move.

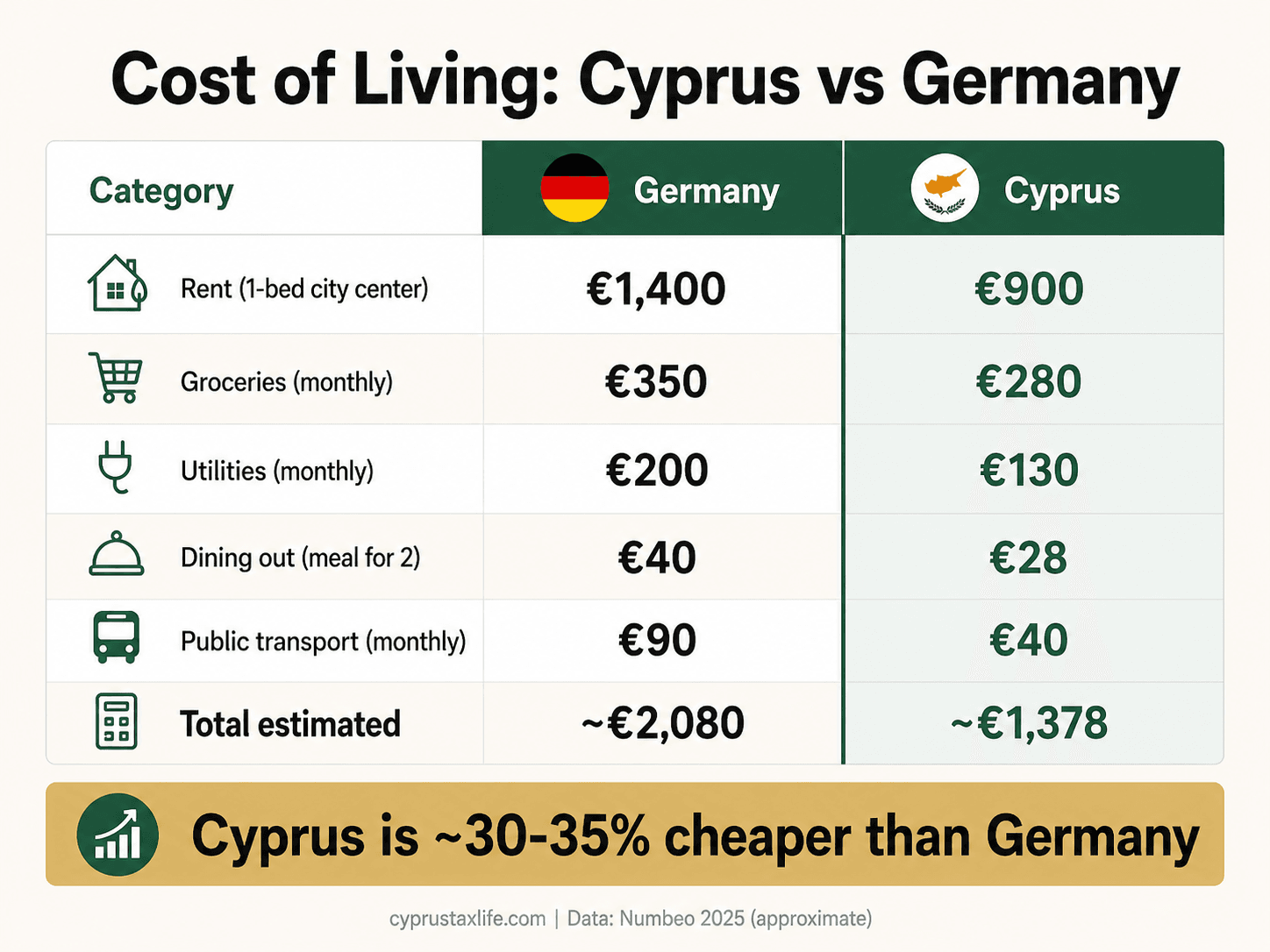

Cost of Living: Germany vs Cyprus

Cyprus offers a considerably lower cost of living compared to Germany. Rent in Larnaca averages EUR 550-750 for a 2-bedroom apartment, versus EUR 1,000-1,500 in cities like Munich, Frankfurt, or Hamburg. Groceries are approximately 25-35% cheaper, with especially notable savings on fresh produce, meat, and dining out. A restaurant meal for two costs approximately EUR 30-40 in Cyprus versus EUR 50-70 in Germany. Utilities are comparable in summer (higher electricity due to air conditioning) but lower overall annually since heating costs in winter are minimal. Car insurance and fuel are slightly cheaper. The biggest savings come from housing and dining, where Cyprus can be 40-50% less expensive than major German cities.

Practical Steps to Relocate

Deregister from Germany (Abmeldung at the Einwohnermeldeamt) - this is a legal requirement

File a final German tax return (Steuererklarung) for the year of departure

Address the exit tax (Wegzugsbesteuerung) if applicable

Set up a Cyprus Ltd company (5-7 working days, approximately EUR 2,100)

Apply for Cyprus tax residency (60-day rule or 183-day rule)

Register as Non-Dom at the Tax Department

Get your Yellow Slip (EU citizen registration)

Open a bank account in Cyprus

Register for Cyprus social insurance

Set up GHS healthcare contributions

Frequently Asked Questions

Will the German Finanzamt challenge my move to Cyprus?+

How does the German exit tax work when moving to Cyprus?+

Can I keep my German GmbH after moving to Cyprus?+

Is Cyprus considered a tax haven by Germany?+

What about German social security when moving to Cyprus?+

How does VAT work for a Cyprus company serving German clients?+

Sources and References

Tax data: PwC Worldwide Tax Summaries, KPMG Tax Guides (2025/2026), Big Four country guides, government tax authority publications. Effective rates are approximations for entrepreneur structures (company + low salary + dividends). Consult a qualified tax advisor before making decisions.

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Related Articles

![Best Holding Company [2026]: Cyprus vs 4 Rivals](https://cdn.sanity.io/images/glqahhks/production/9ec5328706d63fc458c40c9b2e7d80c38816e68f-1678x937.jpg?w=700&q=75&auto=format)

Compare Cyprus, Luxembourg, Netherlands and Malta as holding jurisdictions. Cyprus: 3% effective on dividends, 0% CGT, under EUR 7,000/year to maintain.

Miriam Alonso

Miriam Alonso- Company & Accounting

![Cyprus Withholding Tax on Dividends [2026]: 0% Guide](https://cdn.sanity.io/images/glqahhks/production/d06fdbecc2a60a7a2c152fdeaa9dc27d4c596810-1679x937.jpg?w=700&q=75&auto=format)

Learn why Cyprus charges 0% withholding on dividends to non-residents. SDC at 5% applies only to Cyprus-domiciled recipients. Includes treaty rates table.

Miriam Alonso- Tax Planning

![Cyprus Ltd vs UK Ltd [2026]: 5 Key Differences](https://cdn.sanity.io/images/glqahhks/production/e89433a9e5baf35b8c64e7bf69af332c4dce01c2-1679x937.jpg?w=700&q=75&auto=format)

Compare Cyprus Ltd vs UK Ltd: 15% vs 25% corp tax, 2.65% vs 39.35% dividend tax, and full EU access. Complete guide for British entrepreneurs in 2026.

Miriam Alonso- Company & Accounting