Cyprus vs Netherlands 2026: Tax, Box 3 and Why Dutch Entrepreneurs Leave

Dutch entrepreneurs face 49.5% income tax, Box 3 wealth tax on deemed returns, and 24.5-33% dividend tax (Box 2). Cyprus Non-Dom: ~5% effective. Full 2026 comparison including exit tax and 30% ruling vs Non-Dom.

Last updated: 2026-06-01

Effective tax rate comparison

~37-42%

Netherlands

~5%

Cyprus Non-Dom

Which Is Better For You?

Remote worker / freelancer

Cyprus wins by a wide margin. Box 2 dividend tax (24.5-33%) + 19-25.8% corporate = 37-43% effective. Cyprus: ~5%. The 30% ruling does NOT exempt Box 2 dividends — it only reduces your employment income. For any entrepreneur taking dividends, Cyprus is far better.

Holding company / IP owner

Cyprus wins. No Box 3 wealth tax on investments, no conserverende aanslag risk on future gains, IP Box at 2.5%, 65+ treaties vs Dutch WBSO regime. For holding companies, Cyprus is structurally superior.

Retiree / passive investor

Cyprus wins. Box 3 taxes your savings even when investments lose value (deemed return taxed at 36%). Cyprus has zero wealth tax. For retirees living off investment income, eliminating Box 3 alone can save tens of thousands per year.

Crypto investor

Cyprus wins. Dutch crypto is subject to Box 3 deemed returns or Box 1 income tax up to 49.5%. Cyprus: 8% flat for professional traders (2026), 0% for individual investors. Cyprus is significantly better.

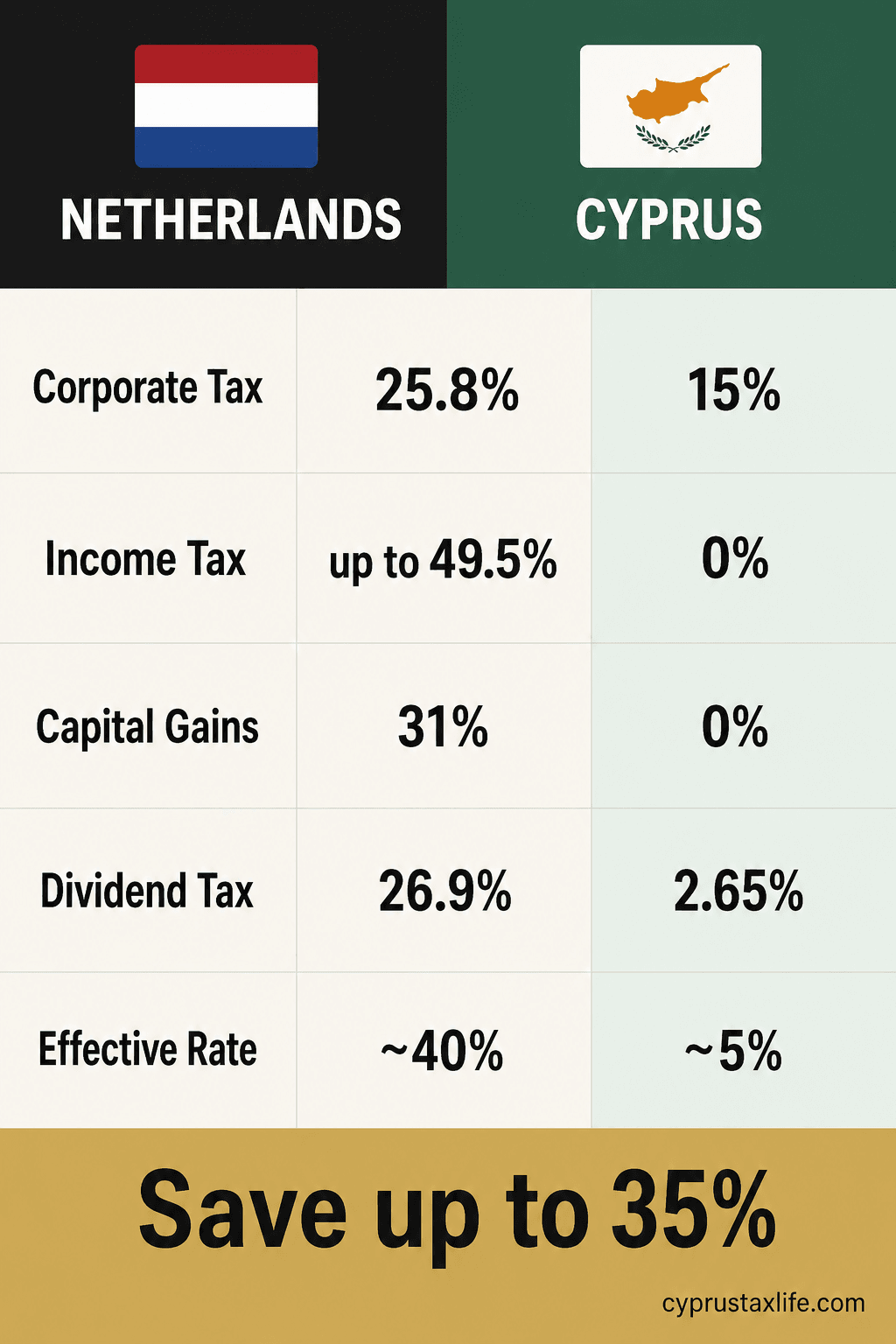

Tax Comparison: Netherlands vs Cyprus

| 🇳🇱 Netherlands | 🇨🇾 Cyprus (Non-Dom) | |

|---|---|---|

| Corporate tax | 19-25.8% | 15% |

| Income tax | Up to 49.5% | 0% (dividends) |

| Capital gains tax | Box 3: 36% on deemed return | 0% (no Cyprus property) |

| Dividend tax | 26.9% (Box 2) | 0% income tax + 2.65% GHS |

| Wealth tax | Box 3 (deemed return taxed at 36%) | None |

| Social contributions | ~27.65% on first EUR 38,098 | ~4% on salary (capped) |

| Effective rate (entrepreneur) | ~37-42% | ~5% |

| VAT | 21% | 19% |

Tax Burden in Netherlands

The Netherlands has one of the most complex tax systems in Europe, structured around three "boxes." Understanding each box is essential for any Dutch entrepreneur evaluating an international move.

**Box 1 - Inkomen uit werk en woning (Income from work and housing)**

Box 1 covers employment income, freelance income, and a deemed rental value on your primary residence (eigenwoningforfait). The rates in 2026 are 36.97% on income up to EUR 75,518 - this combined rate already includes income tax plus AOW (state pension) premiums - and 49.5% on everything above EUR 75,518.

For director-shareholders (DGA - directeur-grootaandeelhouder), the Belastingdienst mandates a minimum "gebruikelijk loon" (customary salary) of at least EUR 56,000 in 2026. This salary must be processed through Box 1 before any dividends can be distributed. The DGA cannot simply skip a salary to avoid Box 1 - the tax authority will impute one.

**Box 2 - Aanmerkelijk belang (Substantial interest - 5%+ shareholding)**

Box 2 applies to dividends and capital gains from shareholdings of 5% or more in a company. The rates since 2024 are 24.5% on the first EUR 67,000 of Box 2 income per taxpayer and 33% on everything above EUR 67,000. For couples filing jointly, each partner has their own EUR 67,000 bracket, giving a combined low-rate threshold of EUR 134,000.

Combined with the corporate tax at the BV level (19% on the first EUR 200,000, 25.8% above), the total effective burden on distributed profits typically reaches 37-43% - and often higher for large earners.

**Box 3 - Sparen en beleggen (Savings and investments - deemed return wealth tax)**

Box 3 does not tax your actual investment returns. Instead, the Belastingdienst calculates a "forfaitair rendement" (deemed return) on your net assets and taxes that deemed return at 36%. The deemed return rates for 2026 are approximately 5.88% for investment assets and 1.44% for bank deposits and savings.

Example: a taxpayer with EUR 500,000 in investments (minus the heffingvrij vermogen exempt threshold of approximately EUR 57,000) faces a deemed return of roughly EUR 26,050, taxed at 36%, resulting in EUR 9,378 in Box 3 tax - regardless of whether those investments actually earned anything or even lost value.

The Box 3 system was declared unconstitutional by the Dutch Supreme Court in December 2021 (the Kerstarrest ruling) precisely because taxing deemed returns can exceed actual returns. The system has been under reform ever since and remains in legal uncertainty as of 2026, with proposals to switch to actual return taxation. This regulatory instability is itself a risk factor for high-net-worth Dutch taxpayers.

Social security contributions add another 27.65% on income up to EUR 38,098, covering AOW, Anw, and Wlz. Self-employed individuals also face ZVW (health insurance) contributions of approximately 5.32%.

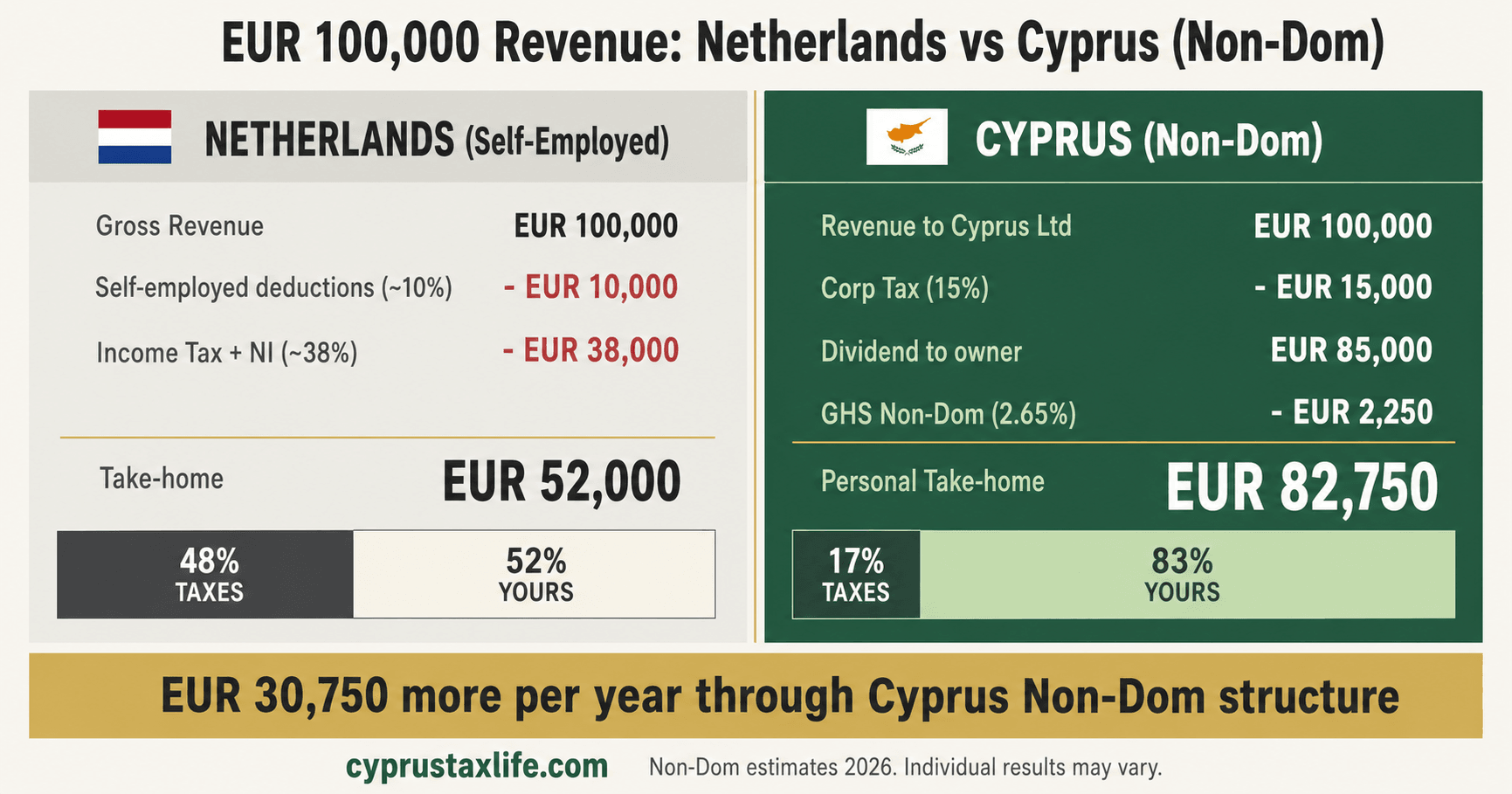

Why Cyprus is Better for Entrepreneurs

Cyprus offers a dramatically simpler and more favorable tax environment for entrepreneurs. Under the Non-Dom regime, which is available to anyone who was not a tax resident of Cyprus for 17 of the 20 years before relocating, dividends received are completely exempt from income tax. The only charge on dividends is the 2.65% GHS (General Healthcare System) contribution.

The standard corporate tax rate is 15% flat, with no progressive brackets or surcharges. There is no wealth tax, no inheritance tax, and capital gains tax only applies to immovable property located in Cyprus. For an entrepreneur billing EUR 100,000 through a Cyprus Ltd company, the effective tax rate drops to approximately 5%, compared to 37-42% in the Netherlands.

Cyprus is a full EU member state, which means Dutch entrepreneurs maintain access to the single market, can invoice EU clients without complications, and benefit from EU freedom of movement. The 60-day rule makes it possible to become a Cyprus tax resident while spending only 60 days per year on the island, provided you do not spend more than 183 days in any other single country.

**The 30% Ruling vs Cyprus Non-Dom - A Critical Comparison**

The Dutch "30% ruling" (30%-regeling) is often mentioned as the primary tool for internationally mobile professionals. It allows qualifying expats hired from abroad to receive 30% of their salary free of Dutch income tax. However, since 2024 the benefit has been restructured and significantly reduced:

- Months 1-20: 30% of salary is tax-exempt - Months 21-40: 20% of salary is tax-exempt - Months 41-60: 10% of salary is tax-exempt - Total maximum duration: 5 years (60 months)

Additionally, since 2024 the ruling is capped at a maximum salary of EUR 246,000 (the "Balkenendenorm"), meaning the maximum exempt amount is EUR 73,800. For anyone earning above that ceiling, the ruling provides no additional benefit.

The Cyprus Non-Dom status is fundamentally different and superior for entrepreneurs in several key ways:

- No income ceiling - the exemption applies to all dividend income regardless of amount - No expiry - Non-Dom status lasts 17 years from the date of first Cyprus tax residency - No employer sponsorship required - you control your own company - No requirement to have been recruited from abroad - founders and entrepreneurs qualify - Dividends are fully exempt - the 30% ruling does NOT exempt dividends from Box 2 taxation, which always applies at 24.5-33%

For a Dutch freelancer or entrepreneur, the 30% ruling is largely irrelevant anyway: it only applies to employment income (not entrepreneurial profits), it requires a formal employer-employee relationship, and it still leaves all Box 2 dividend income fully taxed. The ruling was designed for high-earning employees relocated by multinationals - not for independent business owners. Cyprus Non-Dom, by contrast, is specifically designed for business owners and investors.

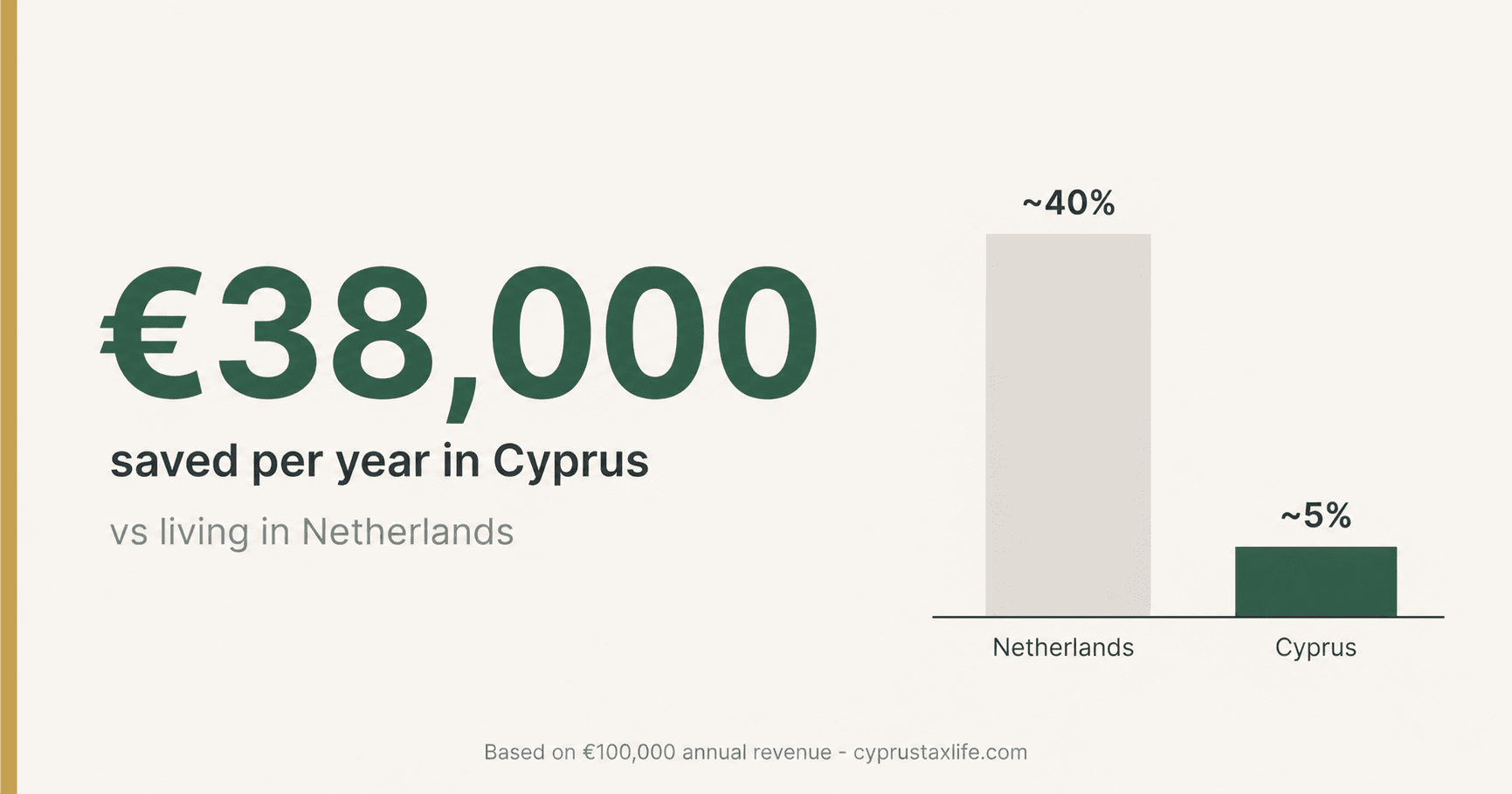

Tax Calculation: EUR 100,000

🇳🇱 Netherlands

🇨🇾 Cyprus (Non-Dom)

Annual savings moving to Cyprus

EUR 35,200

EUR 176,000 over 5 years

Double Tax Treaty: Netherlands - Cyprus

The Netherlands and Cyprus have a comprehensive double tax treaty that has been in force since 1981. Key provisions include withholding tax rates of 0% on dividends paid between companies (if the beneficial owner holds at least 5% of capital), 0-15% on dividends to individuals, 0% on interest payments, and 0% on royalties. The treaty contains tie-breaker rules for dual residency situations based on permanent home, center of vital interests, habitual abode, and nationality. Dutch entrepreneurs planning a move should ensure they clearly establish their center of vital interests in Cyprus to avoid any dual residency disputes.

Exit Tax and Emigration from Netherlands

The Netherlands imposes an exit tax (conserverende aanslag) on unrealized capital gains when a substantial shareholder (5%+ stake) emigrates. This covers deemed disposal of shares in the BV. The tax assessment is issued but payment can be deferred for 10 years (within EU/EEA moves) under certain conditions, requiring annual declarations. After 10 years, the assessment is forgiven. If you sell shares within the 10-year period, the deferred tax becomes due. Important: the exit tax does not apply to Box 3 assets, only to Box 2 (substantial interest) holdings.

**How the conserverende aanslag works in practice:**

The Belastingdienst issues the conserverende aanslag automatically when processing the M-form (formulario de emigracion / emigration form), which you are required to file as a departing taxpayer. The assessment is calculated on the unrealized gain in your BV shares at the date of departure. For large assessments, the Belastingdienst can require a bank guarantee (bankgarantie) before granting deferral - this means you may need to pledge liquid assets as security for the deferred tax liability.

The exit tax also applies at the corporate level when a BV changes its place of effective management from the Netherlands to another country. If you relocate to Cyprus and the management of your Dutch BV moves with you, the BV itself can be subject to a separate corporate-level exit charge on unrealized gains at the company level (the "eindafrekening"). This is distinct from the personal conserverende aanslag on your shares.

**Strategic consideration - selling before emigrating:**

Some Dutch entrepreneurs choose to sell their BV shares before emigrating rather than triggering the conserverende aanslag. By selling while still a Dutch tax resident, the gain is taxed as Box 2 income at the known rates (24.5-33%), without the administrative burden of annual declarations to maintain the deferral. This approach can be preferable if the gain is substantial and the Box 2 rate is expected to increase in the future. Careful timing and professional tax advice are essential before finalizing any decision.

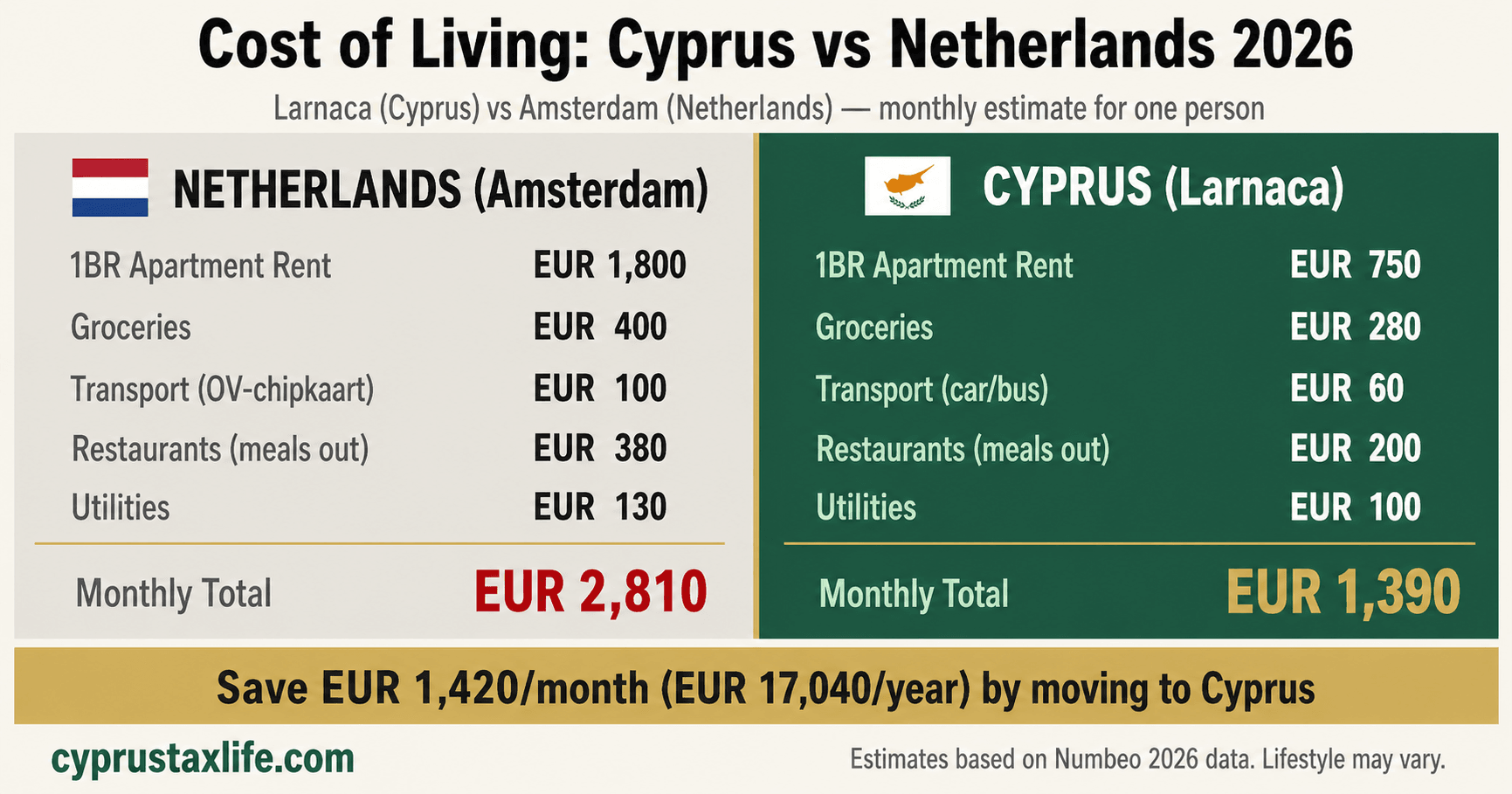

Cost of Living: Netherlands vs Cyprus

Cyprus is significantly cheaper than the Netherlands in most categories. Rent in Larnaca or Limassol averages EUR 550-800 for a 2-bedroom apartment, compared to EUR 1,200-1,800 in Amsterdam or Rotterdam. Groceries are approximately 20-30% cheaper. Dining out costs roughly half of Dutch prices. However, some imported goods and electronics can be similar or slightly more expensive. Healthcare through the GHS system costs only 2.65% of income (1.7% for employees), compared to the mandatory Dutch health insurance of approximately EUR 130/month plus employer contributions. Overall, a single professional can expect monthly expenses of EUR 1,500-2,000 in Cyprus versus EUR 2,500-3,500 in a major Dutch city.

Practical Steps to Relocate

Establish your Cyprus company (Ltd) - takes approximately 5-7 working days, costs around EUR 2,

Apply for tax residency under the 60-day rule or the standard 183-day rule

Register for Non-Dom status at the Tax Department

Obtain your Yellow Slip (EU citizen registration)

Open a Cyprus bank account

Notify the Dutch tax authorities (Belastingdienst) of your emigration using the M-form

Deregister from the BRP (municipal registration)

File your final Dutch tax return

Address the conserverende aanslag if you hold a substantial interest in a Dutch BV

Set up your payroll structure in Cyprus (low salary + dividends)

Frequently Asked Questions

Do I still need to pay Dutch taxes if I move to Cyprus?+

What happens to my Dutch BV after moving to Cyprus?+

Is the Box 3 wealth tax avoidable by moving to Cyprus?+

How does the 30% ruling compare to Cyprus Non-Dom?+

Can I use the Cyprus 60-day rule as a Dutch citizen?+

What about healthcare in Cyprus vs the Netherlands?+

What is Box 3 and does Cyprus have an equivalent?+

My 30% ruling is expiring soon. Should I move to Cyprus?+

Sources and References

Tax data: PwC Worldwide Tax Summaries, KPMG Tax Guides (2025/2026), Big Four country guides, government tax authority publications. Effective rates are approximations for entrepreneur structures (company + low salary + dividends). Consult a qualified tax advisor before making decisions.

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Related Articles

![Best Holding Company [2026]: Cyprus vs 4 Rivals](https://cdn.sanity.io/images/glqahhks/production/9ec5328706d63fc458c40c9b2e7d80c38816e68f-1678x937.jpg?w=700&q=75&auto=format)

Compare Cyprus, Luxembourg, Netherlands and Malta as holding jurisdictions. Cyprus: 3% effective on dividends, 0% CGT, under EUR 7,000/year to maintain.

Miriam Alonso

Miriam Alonso- Company & Accounting

![Cyprus Withholding Tax on Dividends [2026]: 0% Guide](https://cdn.sanity.io/images/glqahhks/production/d06fdbecc2a60a7a2c152fdeaa9dc27d4c596810-1679x937.jpg?w=700&q=75&auto=format)

Learn why Cyprus charges 0% withholding on dividends to non-residents. SDC at 5% applies only to Cyprus-domiciled recipients. Includes treaty rates table.

Miriam Alonso- Tax Planning

![Cyprus Ltd vs UK Ltd [2026]: 5 Key Differences](https://cdn.sanity.io/images/glqahhks/production/e89433a9e5baf35b8c64e7bf69af332c4dce01c2-1679x937.jpg?w=700&q=75&auto=format)

Compare Cyprus Ltd vs UK Ltd: 15% vs 25% corp tax, 2.65% vs 39.35% dividend tax, and full EU access. Complete guide for British entrepreneurs in 2026.

Miriam Alonso- Company & Accounting