Cyprus vs France 2026: Tax Comparison for French Entrepreneurs

France's PFU (30% on dividends) + 25% corp tax = 47.5% effective on distributed profits. Cyprus Non-Dom: ~5%. EUR 42,500 saved per year. Full comparison including IFI wealth tax, exit tax and CSG/CRDS guide.

Last updated: 2026-06-01

Effective tax rate comparison

~42-50%

France

~5%

Cyprus Non-Dom

Which Is Better For You?

Remote worker / freelancer

Cyprus wins by the largest margin in Europe. France: 25% corp + 30% PFU on dividends = 47.5% effective. Cyprus: ~5%. Annual saving: EUR 42,500 on EUR 100,000. Plus: no IFI real estate wealth tax, no CSG/CRDS (17.2%) on investment income, no ISF concerns.

Holding company / IP owner

Cyprus wins. France's CFC rules can challenge structures without genuine substance. For companies with real Cyprus activity, Cyprus outperforms on all metrics: 15% vs 28% combined corporate, 0% vs 30% on dividends, IP Box at 2.5% vs France's own IP Box (10%) which is less favourable.

Retiree / passive investor

Cyprus wins for investment income. France's IFI (real estate wealth tax) at 0.5-1.5% on net real estate above EUR 1.3M is a recurring burden. Cyprus has no wealth tax. For dividend income, Non-Dom exemption beats France's 30% PFU every year.

Crypto investor

Cyprus wins. France taxes crypto gains at 30% PFU (flat). Cyprus: 8% flat for professional traders (2026), 0% for individual investors. Cyprus is significantly better.

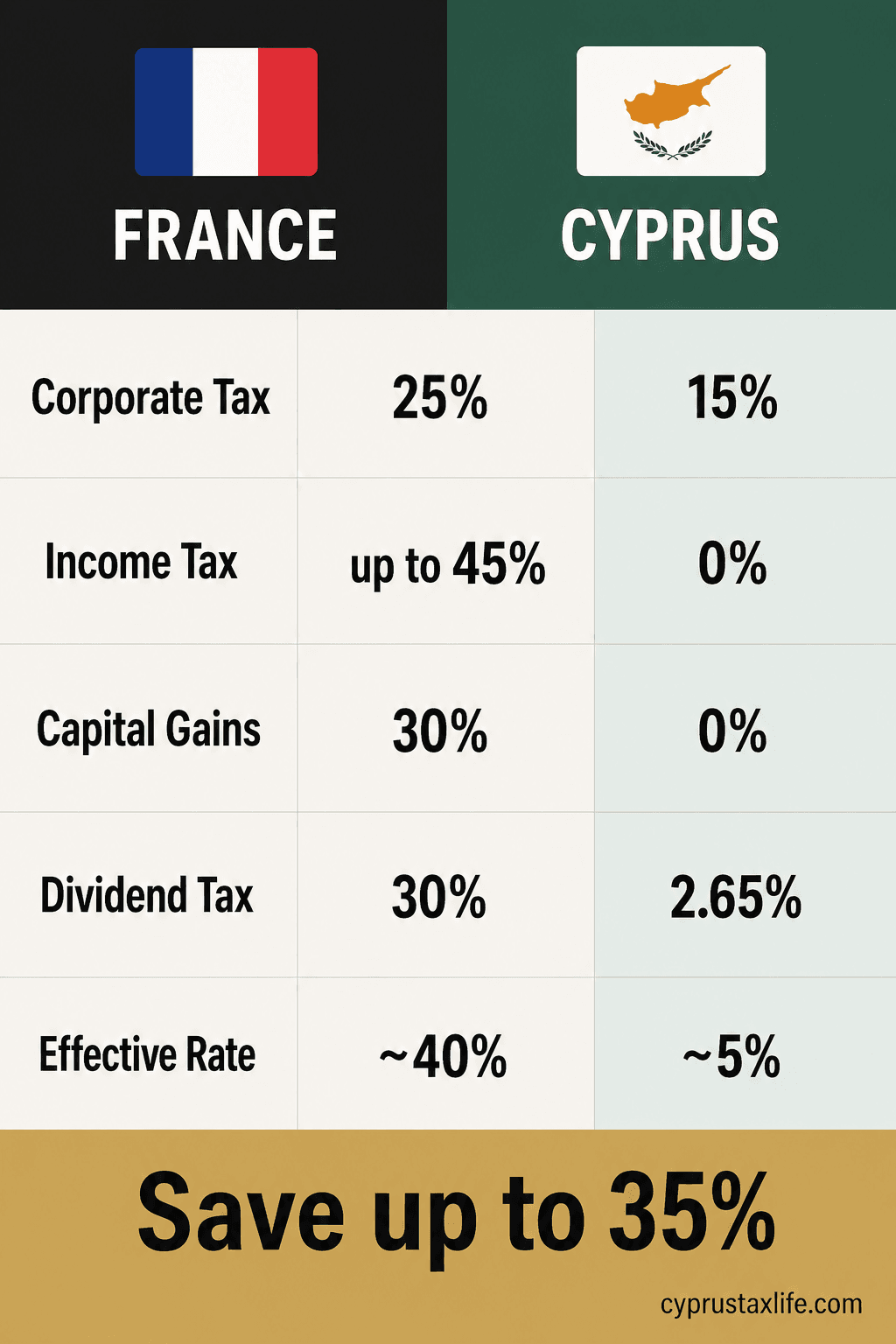

Tax Comparison: France vs Cyprus

| 🇫🇷 France | 🇨🇾 Cyprus (Non-Dom) | |

|---|---|---|

| Corporate tax | 25% | 15% |

| Income tax | Up to 45% + 4% exceptional contribution | 0% (dividends) |

| Capital gains tax | 30% PFU (or progressive scale) | 0% (no Cyprus property) |

| Dividend tax | 30% PFU (12.8% income tax + 17.2% social charges) | 0% income tax + 2.65% GHS |

| Wealth tax | IFI on real estate above EUR 1.3M | None |

| Social contributions | ~45% employer + ~22% employee | ~4% on salary (capped) |

| Effective rate (entrepreneur) | ~42-50% | ~5% |

| VAT | 20% | 19% |

Tax Burden in France

France is infamous for its exceptionally high tax burden, particularly on entrepreneurs and business owners. The income tax system uses progressive rates from 0% to 45%, with an additional 3% contribution on income above EUR 250,000 and 4% above EUR 500,000.

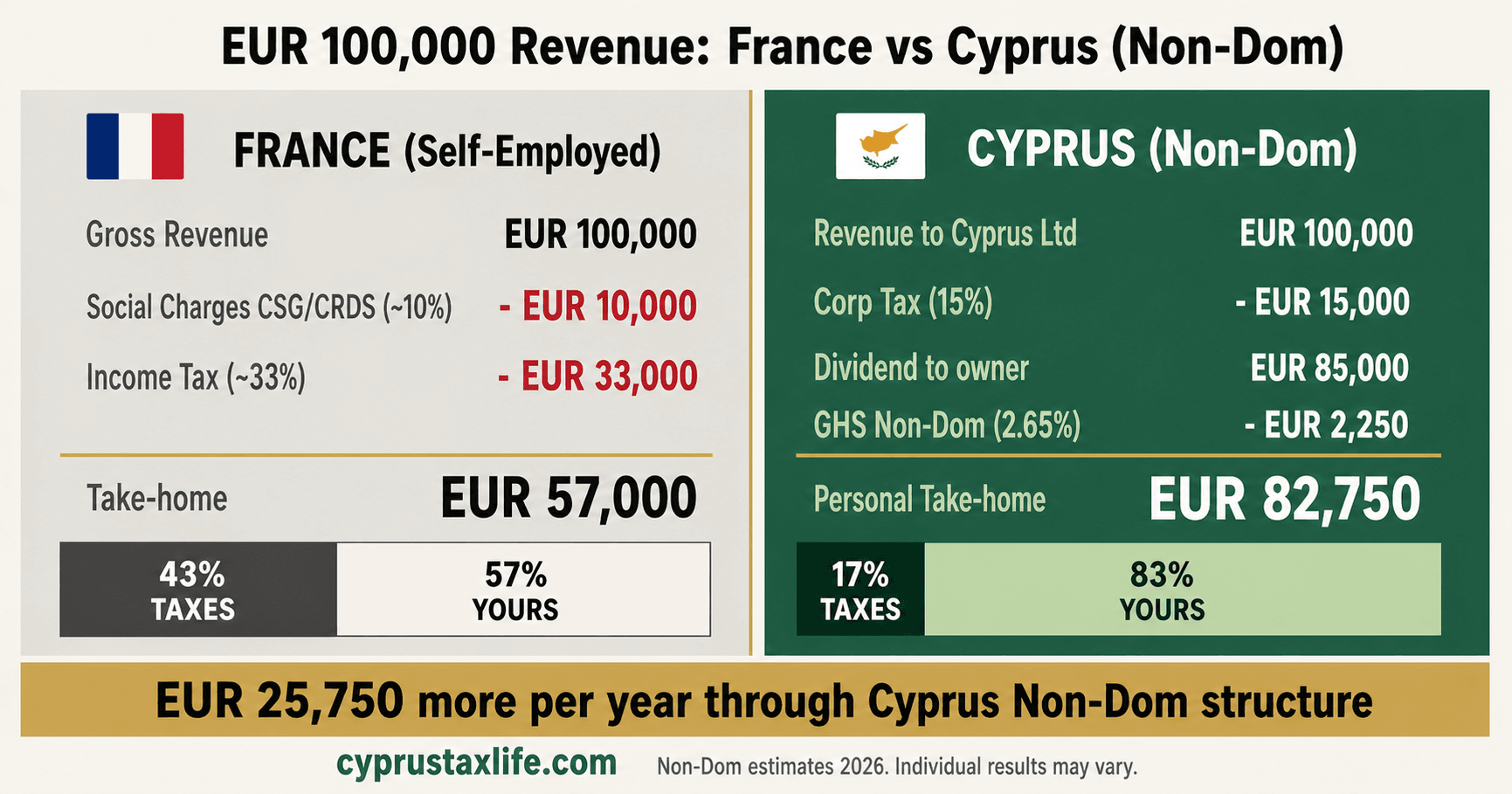

The corporate tax rate (Impot sur les societes, IS) is now a flat 25% after a gradual reduction from 33.33%. When distributing dividends, shareholders face the PFU (Prelevement Forfaitaire Unique, also known as the "flat tax") of 30%, comprising 12.8% income tax and 17.2% social charges (CSG/CRDS). Alternatively, dividends can be taxed on the progressive scale with a 40% deduction, which can be favorable for lower-income individuals.

The combined effect on distributed corporate profits is devastating: on EUR 100,000 of profit, the company pays EUR 25,000 in corporate tax. The remaining EUR 75,000, if distributed as dividends, is then taxed at 30% (EUR 22,500). The total tax burden reaches EUR 47,500, an effective rate of 47.5%.

Social contributions in France are among the highest in Europe. For employees, employer contributions range from 25% to 42% of gross salary, and employee contributions are approximately 22%. For self-employed (TNS), contributions range from 35% to 45% depending on income level.

France also has the IFI (Impot sur la Fortune Immobiliere), a real estate wealth tax on net real estate assets exceeding EUR 1.3 million, with rates from 0.5% to 1.5%.

Why Cyprus is Better for Entrepreneurs

The contrast between France and Cyprus for entrepreneurs is perhaps the most dramatic in all of Europe. Where France imposes a combined 47.5% on distributed corporate profits, Cyprus under the Non-Dom regime achieves approximately 5%.

With a Cyprus Ltd, corporate tax is a flat 15% (no surcharges, no exceptional contributions). Dividends are fully exempt from income tax under Non-Dom status, with only a 2.65% GHS contribution. There is no equivalent of the French CSG/CRDS social charges on investment income.

Cyprus has no wealth tax of any kind, no inheritance tax, and no gift tax. For French entrepreneurs with significant real estate holdings, this alone can represent substantial savings.

The French entrepreneur community in Cyprus is growing, with Limassol and Paphos hosting established French-speaking networks. Cyprus offers a quality of life comparable to southern France, with 340 days of sunshine per year, Mediterranean cuisine, and a safe, family-friendly environment, but at a fraction of the tax cost.

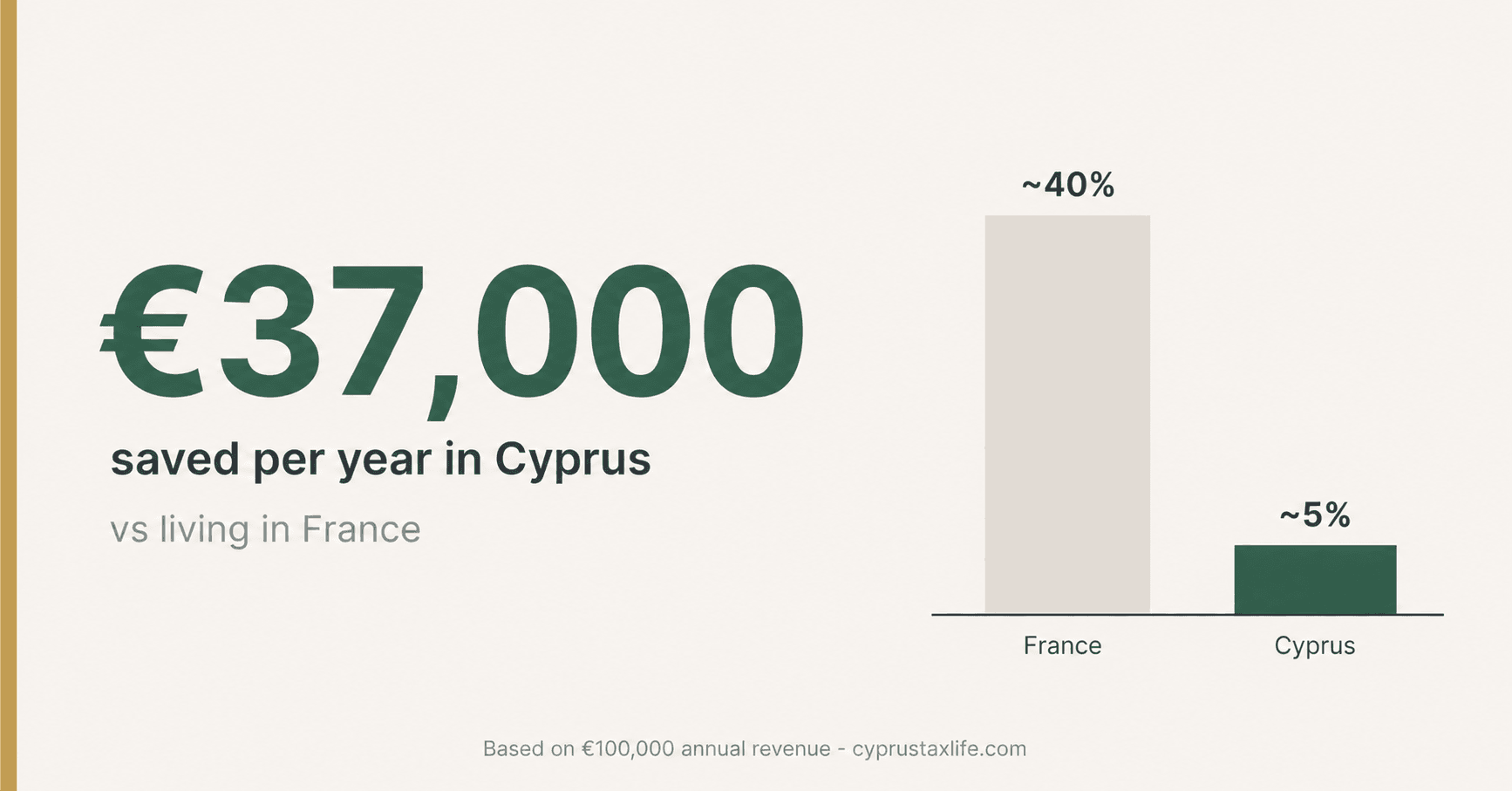

Tax Calculation: EUR 100,000

🇫🇷 France

🇨🇾 Cyprus (Non-Dom)

Annual savings moving to Cyprus

EUR 42,500

EUR 212,500 over 5 years

Double Tax Treaty: France - Cyprus

France and Cyprus have a double tax treaty signed in 1981. Withholding tax rates: dividends 10% (if the beneficial owner holds at least 10% of capital) or 15% otherwise, interest 0-10%, royalties 0-5%. The treaty follows the OECD model with comprehensive provisions. Pensions paid to Cyprus residents from French sources are generally taxable only in Cyprus. Capital gains from share disposals are taxable only in the state of residence of the seller. French entrepreneurs should note that the treaty contains specific anti-abuse provisions that require genuine economic substance in Cyprus.

Exit Tax and Emigration from France

France has a comprehensive exit tax (exit levy) that applies when a taxpayer who has been a French tax resident for at least 6 of the last 10 years transfers their tax residence abroad. The tax applies to unrealized capital gains on shareholdings exceeding EUR 800,000 in value or representing at least 50% of a company's profits. For moves within the EU/EEA, the tax is automatically deferred (sursis automatique). The deferred tax is forgiven after maintaining the shareholding for two years post-departure if the shareholding is below EUR 2.57 million, or after five years for larger holdings. If shares are sold during the deferral period, the exit tax becomes due. The CSG/CRDS portion (17.2%) is immediately due and cannot be deferred, though this is currently being challenged in courts.

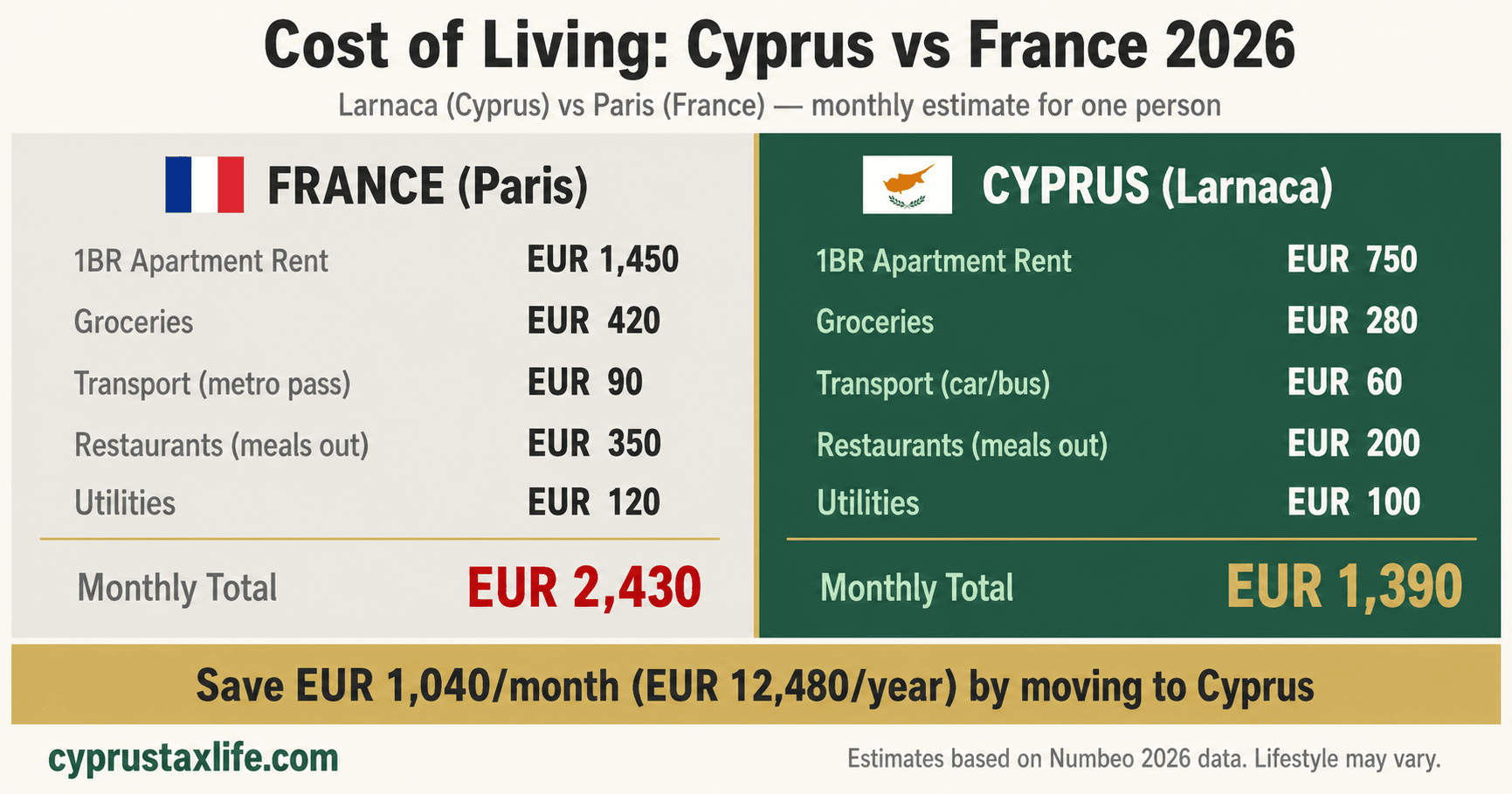

Cost of Living: France vs Cyprus

Cyprus is substantially cheaper than France, especially compared to Paris and the Cote d'Azur. Rent in Limassol or Larnaca for a 2-bedroom apartment averages EUR 600-800, compared to EUR 1,500-2,500 in Paris or EUR 1,200-1,800 on the French Riviera. Dining out is approximately 40-50% cheaper. A quality restaurant meal for two costs EUR 30-40 in Cyprus versus EUR 60-80 in Paris. Groceries are 20-30% cheaper overall, though French supermarkets offer more variety in cheese and wine. Healthcare costs are lower through the GHS system (2.65% contribution) compared to the French mutuelle and social charges. Property prices in Cyprus are approximately 50-60% lower than equivalent locations in southern France.

Practical Steps to Relocate

Notify the French tax authorities (Service des impots des particuliers) of your departure

File your final French tax return for the year of departure

Address the exit tax if applicable (gather asset valuations)

Establish a Cyprus Ltd company (5-7 working days, approximately EUR 2,100)

Apply for Cyprus tax residency

Register for Non-Dom status

Obtain your Yellow Slip

Open a Cyprus bank account

Transfer your social insurance to Cyprus

Close or restructure any French structures (SAS, SARL, EURL)

Update your French bank about your new tax residency

Frequently Asked Questions

Can French tax authorities challenge my move to Cyprus?+

What about the French exit tax?+

Is the PFU (flat tax) still better than moving to Cyprus?+

Do I still pay CSG/CRDS if I live in Cyprus?+

Can I keep my SAS or SARL after moving to Cyprus?+

Is there a French-speaking community in Cyprus?+

Sources and References

Tax data: PwC Worldwide Tax Summaries, KPMG Tax Guides (2025/2026), Big Four country guides, government tax authority publications. Effective rates are approximations for entrepreneur structures (company + low salary + dividends). Consult a qualified tax advisor before making decisions.

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Related Articles

![Best Holding Company [2026]: Cyprus vs 4 Rivals](https://cdn.sanity.io/images/glqahhks/production/9ec5328706d63fc458c40c9b2e7d80c38816e68f-1678x937.jpg?w=700&q=75&auto=format)

Compare Cyprus, Luxembourg, Netherlands and Malta as holding jurisdictions. Cyprus: 3% effective on dividends, 0% CGT, under EUR 7,000/year to maintain.

Miriam Alonso

Miriam Alonso- Company & Accounting

![Cyprus Withholding Tax on Dividends [2026]: 0% Guide](https://cdn.sanity.io/images/glqahhks/production/d06fdbecc2a60a7a2c152fdeaa9dc27d4c596810-1679x937.jpg?w=700&q=75&auto=format)

Learn why Cyprus charges 0% withholding on dividends to non-residents. SDC at 5% applies only to Cyprus-domiciled recipients. Includes treaty rates table.

Miriam Alonso- Tax Planning

![Cyprus Ltd vs UK Ltd [2026]: 5 Key Differences](https://cdn.sanity.io/images/glqahhks/production/e89433a9e5baf35b8c64e7bf69af332c4dce01c2-1679x937.jpg?w=700&q=75&auto=format)

Compare Cyprus Ltd vs UK Ltd: 15% vs 25% corp tax, 2.65% vs 39.35% dividend tax, and full EU access. Complete guide for British entrepreneurs in 2026.

Miriam Alonso- Company & Accounting