Quick Answer

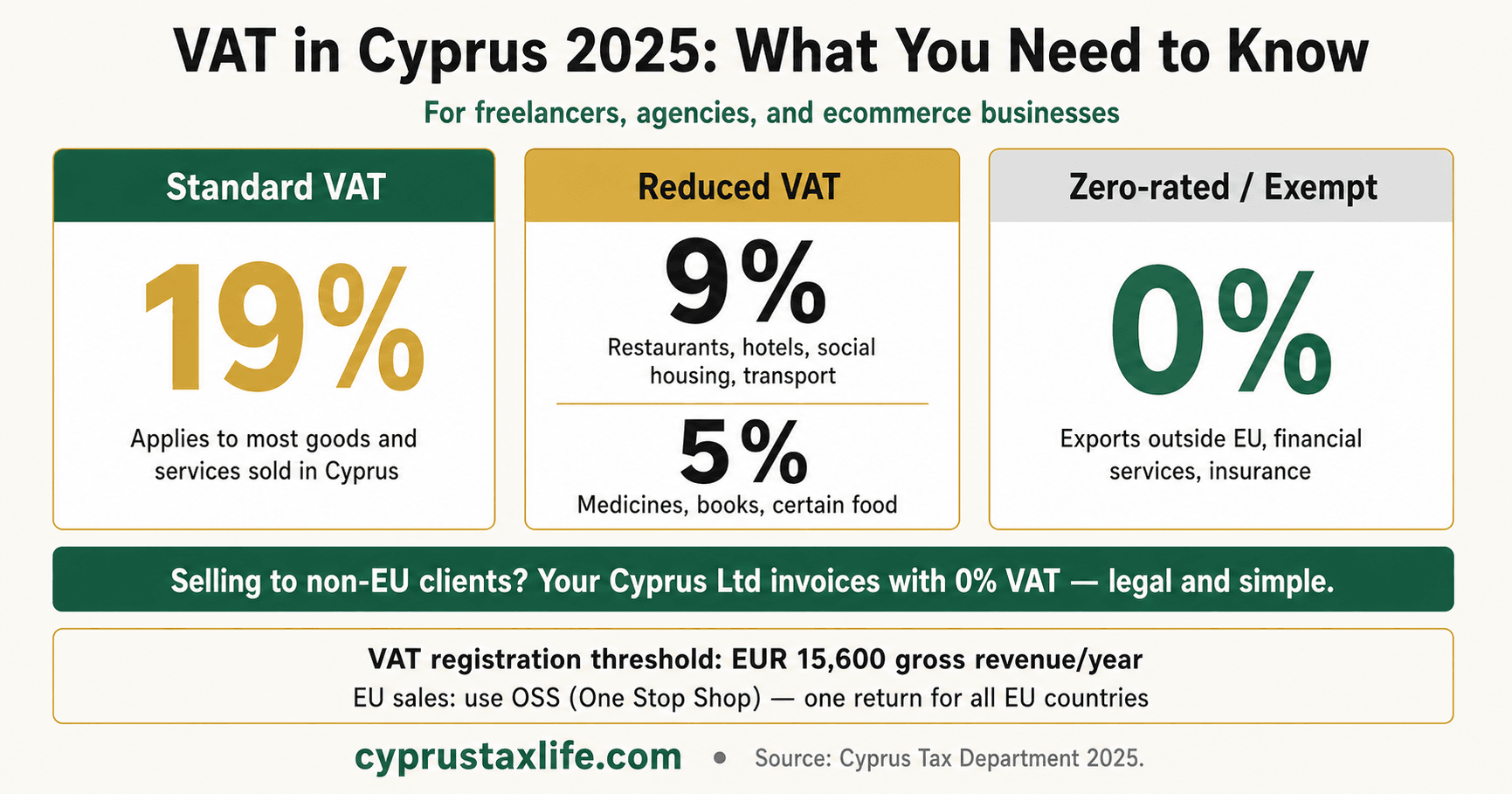

Cyprus VAT rates for 2026: standard rate 19%, reduced rate 9% (hospitality, transport, cultural services), super-reduced rate 5% (food, medicine, books, new residential properties). The VAT registration threshold is EUR 15,600 annual turnover. Cyprus companies providing B2B services to EU clients can apply reverse charge, removing the VAT obligation.

VAT in Cyprus: Complete 2026 Guide

Cyprus VAT is 19% standard rate. Freelancers and companies must register once turnover exceeds €15,600 per year. Here is everything you need to know.

Last updated:

Key Facts 2026

| Standard rate | 19% |

| Reduced rate (hospitality, transport, tourism) | 9% |

| Super-reduced rate (food, medicines, books) | 5% |

| Zero rate (exports, financial services, insurance) | 0% |

| Registration threshold | EUR 15,600 annual taxable turnover |

| VAT return frequency | Quarterly (default) |

| EU OSS available | Yes (for B2C cross-border EU sales) |

| IOSS available | Yes (for imports under EUR 150 B2C) |

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Get personalised guidance on Non-Dom status, company formation, and your specific tax situation from an experienced Cyprus tax advisor.

VAT in Cyprus, Frequently Asked Questions

Do I charge VAT to clients outside Cyprus?

What is the VAT registration threshold in Cyprus?

Can I reclaim VAT on business expenses?

How does OSS work for e-commerce?

Is VAT different for digital services vs physical products?

Frequently Asked Questions

What is the VAT rate in Cyprus?

At what turnover do I need to register for VAT in Cyprus?

Do freelancers in Cyprus need to register for VAT?

How often do I file VAT returns in Cyprus?

Can I get a VAT refund in Cyprus?

Is VAT charged on rent in Cyprus?

What is a Cyprus VAT number format?

Do I need to register for OSS if I sell digital products to EU customers from Cyprus?

What is the VAT reverse charge and when does it apply in Cyprus?

Can a foreign (non-Cyprus) business reclaim VAT paid on expenses in Cyprus?

Is the purchase of a new property in Cyprus subject to VAT?

How do I deregister from VAT in Cyprus?

Why can't financial services companies in Cyprus reclaim their VAT?

Related Guides

Sources

Cyprus Tax Department VAT Service. EU VAT Directive 2006/112/EC as implemented in Cyprus. Updated: April 2026.

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Free newsletter

What do you want to hear about?

No spam. Unsubscribe any time.