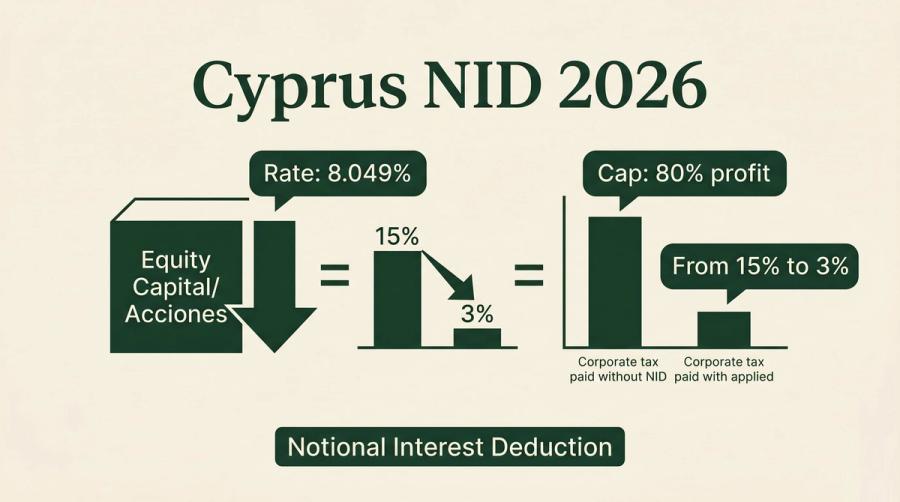

Cyprus NID 2026: Notional Interest Deduction at 8.049%

The Cyprus Notional Interest Deduction (NID) allows companies to deduct a calculated notional interest on new equity capital from their taxable income. The NID effectively treats equity financing in the same way as debt financing for tax purposes, reducing the effective corporate tax rate significantly for equity-funded businesses. The NID reference rate for Cyprus companies in 2026 is 8.049%.

What the NID Is and How It Works

A Cyprus company that finances its operations through new equity - paid-up share capital or share premium - can deduct a notional interest charge on that equity from its taxable profits. This deduction is not a cash payment; it is a calculation-based allowance that reduces the corporate tax base.

The deduction equals the qualifying new equity multiplied by the NID reference rate. For 2026, the Cyprus rate is 8.049%, meaning a company with EUR 1,000,000 of qualifying new equity can deduct EUR 80,490 from its taxable income before applying the 15% corporate tax rate.

NID Reference Rate for 2026

The NID reference rate is calculated as the 10-year government bond yield of the country where the equity funds are deployed (as at 31 December of the prior year) plus a 5% premium. The Cyprus Tax Department publishes the applicable rates annually.

Rates published on 18 March 2026 (based on yields as at 31 December 2025):

- Cyprus: 3.049% bond yield + 5% = 8.049% NID rate.

- Germany: 2.853% + 5% = 7.853%.

- United Kingdom: 4.574% + 5% = 9.574%.

- United States: 4.120% + 5% = 9.120%.

- Switzerland: 0.295% + 5% = 5.295%.

What Equity Qualifies for NID

Only new equity introduced on or after 1 January 2015 qualifies. Qualifying equity includes:

- New paid-up share capital - cash contributions.

- New share premium accounts.

- In-kind contributions at verified fair market value.

Retained earnings, existing equity pre-2015, and reserves that have not been formally converted to share capital or share premium do not qualify.

The 80% Cap

The NID deduction cannot exceed 80% of the company's taxable profit before applying the NID. It cannot create or increase a tax loss, and any excess NID is not carried forward to future years. This means the minimum effective tax rate under NID is 15% multiplied by 20% = 3% of taxable profit.

Who Benefits Most

The NID is most beneficial for:

- Holding companies receiving dividend income (which is already tax-exempt) and investing through equity-funded subsidiaries.

- IP companies funded through equity rather than shareholder loans.

- Operating companies in Cyprus that receive new equity injections from shareholders.

- International structures where new capital is injected into a Cyprus entity to fund acquisitions or operations.

Companies that rely entirely on retained earnings without new equity injections benefit less, as the NID only applies to new equity post-2015.

NID vs IP Box

The NID can be combined with the Cyprus IP Box regime (2.5% effective tax rate on qualifying IP income) but careful structuring is required to avoid overlap and ensure both regimes apply optimally.

Sources: KPMG Cyprus Tax Alert - NID Reference Interest Rates 2026. EY Global Tax News - Cyprus Tax Authority Publishes Bond Yield Rates for NID (March 2026). PwC Worldwide Tax Summaries - Cyprus Corporate Tax Credits and Incentives.

![Cyprus Ltd vs Irish Ltd: Company Tax Compared [2026]](https://cdn.sanity.io/images/glqahhks/production/84e3d82538a859345d8d2447e8e097c5777fb238-1679x937.png?w=700&q=75&auto=format)

![Cyprus vs Malta Company Formation [2026]](https://cdn.sanity.io/images/glqahhks/production/97db89d0ce729a9e931d09bc1522631faa6c3474-1679x937.png?w=700&q=75&auto=format)