Lowest Corporate Tax in Europe by Country (2026)

Corporate tax rates vary dramatically across Europe - from 9% in Hungary to over 25% in France and Germany. For entrepreneurs setting up a company or relocating a business, choosing the right jurisdiction can save tens of thousands of euros per year.

According to Eurostat 2026, corporate tax revenues across the EU have remained stable as a share of GDP, yet statutory rates diverge significantly, the gap between the highest and lowest EU corporate tax rates now exceeds 25 percentage points.

This guide ranks EU and key non-EU countries by corporate tax rate, explains what the headline numbers hide, and shows why Cyprus at 15% often beats Hungary at 9% in practice.

EU Corporate Tax Rates - Full Ranking (2026)

Here are the standard corporate tax rates across Europe, from lowest to highest. Note that Latvia and Estonia are included separately at the bottom of this table because their 0% rate applies only to retained profits - distributions are taxed at 20%:

| Country | Corporate Tax Rate | Key Notes |

|---|---|---|

| Hungary | 9% | Lowest in EU; CFC rules apply |

| Bulgaria | 10% flat | Simplest regime in EU |

| Ireland | 12.5% (trading only) | 25% for passive income |

| Cyprus | 15% | Standard rate since 2023 |

| Lithuania | 15% | 5% for small companies under EUR 300K |

| Romania | 16% | 1% micro-enterprise under EUR 500K revenue |

| Poland | 19% standard | 9% for SMEs |

| Czech Republic | 21% | Standard rate |

| Netherlands | 19% up to EUR 200K / 25.8% above | ATAD2 reduced planning opportunities |

| Sweden | 20.6% | No special regimes |

| Latvia | 0% reinvested / 20% distributed | Only taxed on profit distribution |

| Estonia | 0% reinvested / 20% distributed | Only taxed on profit distribution |

| Spain | 25% | Standard rate |

| France | 25% | Standard rate |

| Germany | ~30% | Combined corporate + trade tax |

Bulgaria stands out as a notable option for very simple businesses: 10% flat rate, no complexity, minimal bureaucracy. However, Bulgaria lacks the treaty network, legal infrastructure, and EU business credibility of Cyprus or Ireland for international structures.

Germany is the highest in Western Europe in practice. The published corporate tax rate of 15% is misleading: companies also pay a solidarity surcharge and a municipal trade tax (Gewerbesteuer) that varies by city. In Frankfurt or Munich, the combined rate reaches 30-33%. German companies operating across borders face significant costs compared to alternatives.

EU and EEA countries with the lowest corporate tax rates (2026):

- Hungary: 9%, lowest in EU, but requires substance and has GAAR rules

- Bulgaria: 10%, flat rate, simple system, EU member

- Ireland: 15% (Pillar Two: 15% for large companies), strong treaty network, common law

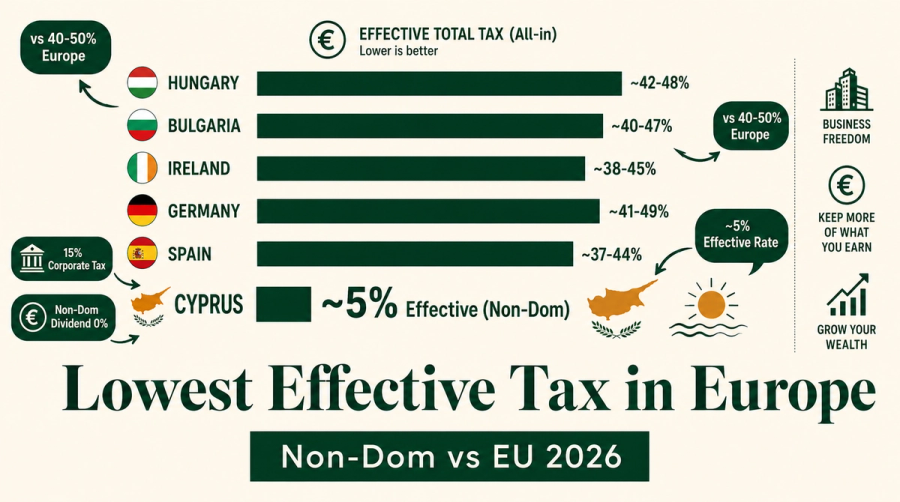

- Cyprus: 15%, but effective ~3% on IP income via IP Box; Non-Dom makes total effective rate ~17.65% for dividends

- Lithuania: 15% (5% for small companies), fast-growing tech hub

- Poland: 9% (small companies) / 19%, varies by size

- Romania: 1% micro-company / 16% standard

- Malta: 35% headline but 5% effective via 6/7ths refund, requires holding structure

- Germany: ~29.5% combined federal + trade tax, highest among major EU economies

- France: 25% (reduced 15% for SMEs on first €42,500)

What the Headline Corporate Tax Rate Doesn't Tell You

The corporate tax rate is only one part of the equation. Withholding tax on dividends, personal income tax, and anti-avoidance rules determine the actual cost.

Estonia and Latvia show 0% corporate tax on reinvested profits - but you pay 20% when distributing dividends. This is deferred taxation, not eliminated taxation. If you plan to extract profits as dividends, the effective rate is the same as other 20% countries. The headline rate is misleading for founders who need to actually take money out of the business.

Hungary at 9% has one of the most complex controlled foreign company (CFC) rule sets in the EU. A non-resident director or parent company may be caught by CFC rules, making the 9% nominal rate unachievable in practice for many international structures. For a non-Hungarian resident managing a Hungarian company remotely, the risk of being reclassified as a tax resident in another jurisdiction adds further complexity.

Ireland's reduced rate applies only to 'trading income' - income from active business operations. Passive income including dividends, interest, and royalties is taxed at 25%. For holding companies or IP structures, Ireland is therefore more expensive than its advertised rate suggests. The distinction between trading and non-trading income requires ongoing legal assessment and adds compliance costs.

The Netherlands introduced ATAD2 anti-hybrid rules that significantly reduced the tax planning advantages that made it attractive for international holding structures in the early 2000s. What worked in 2005 no longer works in 2026. Founders should base decisions on current rules, not historical reputation.

Cyprus vs Hungary: Why 15% Often Beats 9% in Practice

When comparing Cyprus and Hungary for company formation, the 6 percentage point difference in corporate tax rate is often offset by the sharply different treatment of founders and shareholders at the personal level. The total tax burden on extracted profits is what matters, not the rate on company profits in isolation.

| Factor | Hungary (9%) | Cyprus (15%) |

|---|---|---|

| Corporate tax rate | 9% | 15% |

| Dividend tax (individual) | Up to 30% on distributions | 0% for Non-Dom residents |

| Withholding tax on outbound dividends | 0% (EU) | 0% |

| CFC rules | Strict | Moderate (ATAD compliant) |

| Non-Dom regime for founders | None | Yes - 17 years, 2.65% GHS only |

| Capital gains tax (individual) | Taxable | 0% (no CGT in Cyprus) |

| English legal system | No | Yes (Common Law) |

| Treaty network | 90+ | 65+ |

For a founder receiving EUR 200,000 in dividends: Hungary = 9% corporate + 30% personal dividend tax. Cyprus = 15% corporate + 2.65% GHS for a Non-Dom resident. The effective combined rate favours Cyprus. At EUR 500,000 in distributions, the difference becomes even more pronounced: Hungary subjects the full amount to personal dividend tax, while in Cyprus the GHS contribution is capped at EUR 180,000 of insurable income.

Cyprus also has no capital gains tax on the sale of shares in non-Cypriot companies, and no inheritance tax. These advantages compound over time for founders building equity value rather than just taking salary.

How Cyprus Non-Dom works: Cyprus Non-Dom Status Guide

Which EU Country Is Best for a Holding Company?

For holding structures that collect dividends from subsidiaries, the key factor is not the corporate tax rate but the participation exemption and withholding taxes on outbound distributions. A holding company that pays 0% on dividends received and 0% on dividends paid to shareholders - regardless of its nominal corporate rate - is more efficient than a 9% jurisdiction with withholding taxes and no exemption.

Cyprus offers: (1) participation exemption on dividends received from qualifying subsidiaries - the dividend flows into the Cyprus holding company free of corporate tax, (2) 0% withholding tax on dividends paid to non-resident shareholders, (3) 0% tax on capital gains from selling shares, and (4) 65+ double tax treaties reducing withholding at the subsidiary level.

The practical outcome: profits generated by an operating subsidiary in any country flow up to a Cyprus holding company tax-free (under the participation exemption), and then flow out to the Non-Dom shareholder with only 2.65% GHS applied. No other EU jurisdiction combines all four of these characteristics for a standard company structure without special licensing or minimum investment requirements.

Full guide: How Cyprus Holding Companies Pay 0% Tax on Dividends

Learn more: Holding Company in Cyprus: Structure, Tax Benefits and Setup

Low Corporate Tax Outside the EU

For reference, these are key non-EU jurisdictions often compared to Cyprus. Each has distinct advantages but also significant trade-offs compared to an EU-based structure:

| Country | Corporate Tax | Key Notes |

|---|---|---|

| Georgia | 15% (or 1% Virtual Zone for IT) | Territorial system; non-EU |

| UAE | 9% (from June 2023) | No personal income tax; non-EU |

| Switzerland | ~15-20% (cantonal) | Varies by canton; high living costs |

| UK | 25% | Raised from 19% in 2023 |

Georgia offers a Virtual Zone regime for IT companies at 1% corporate tax on qualifying income, making it one of the lowest rates globally for software and SaaS businesses. However, Georgia is not in the EU, lacks the single market access, and banking infrastructure is less developed for international payments.

The UAE introduced a 9% corporate tax in June 2023 for companies earning above AED 375,000 (approximately USD 102,000) in profit. Below that threshold, the rate is 0%. Free zone companies may maintain a 0% rate on qualifying income if they meet specific substance requirements. There is no personal income tax in the UAE, making it attractive for founders who also relocate personally. The trade-off is distance from the EU market, cultural context, and the cost of establishing genuine substance.

How to Set Up a Cyprus Company

Setting up a Cyprus Ltd takes 1-2 weeks and costs EUR 1,500-3,000 in registration fees. Annual maintenance (accounting, audit, registered agent) is approximately EUR 3,000-6,000. These costs are well below comparable setups in the Netherlands, Ireland, or Germany.

To benefit from the personal tax advantages described in this article, the founder also needs to establish Cyprus tax residency - spending at least 60 days per year in Cyprus, not being a tax resident elsewhere for more than 183 days, and meeting the other conditions of the 60-day rule. This makes Cyprus particularly attractive for location-independent founders who can control where they spend their time.

Cyprus is an EU and eurozone member state, uses Common Law (inherited from the British legal system), and has a well-established network of international law firms and accounting firms experienced with cross-border structures. English is widely spoken and most business documents are drafted in English. These practical factors matter when operating an international business - bureaucratic delays and language barriers in lower-tax jurisdictions can quickly offset any nominal tax saving.

Full setup guide: How Much Does It Cost to Set Up a Company in Cyprus?

Company formation details: Cyprus Company Formation Guide

Frequently Asked Questions

Which EU country has the lowest corporate tax?

Is Cyprus corporate tax lower than Ireland?

Does Estonia have 0% corporate tax?

What is the corporate tax rate in Cyprus in 2026?

What is the lowest corporate tax in the world?

Can I legally reduce corporate tax by relocating my company?

Ready to set up a Cyprus company? See our advisory services

![Cyprus Ltd vs Irish Ltd: Company Tax Compared [2026]](https://cdn.sanity.io/images/glqahhks/production/84e3d82538a859345d8d2447e8e097c5777fb238-1679x937.png?w=700&q=75&auto=format)

![Cyprus vs Malta Company Formation [2026]](https://cdn.sanity.io/images/glqahhks/production/97db89d0ce729a9e931d09bc1522631faa6c3474-1679x937.png?w=700&q=75&auto=format)