Moving from Spain to Cyprus

Quick Answer

Moving from Spain to Cyprus with Non-Dom status reduces your effective tax rate from ~40-50% to approximately 5%. Cyprus applies 0% Special Defence Contribution on foreign dividends, a flat 15% corporate tax, and offers tax residency with just 60 days of physical presence per year under the 60-day rule. A double tax treaty between Spain and Cyprus prevents double taxation during the transition.

Last updated: 2026-06-16

Why Spain Professionals Consider Cyprus

Spain imposes a high tax burden on entrepreneurs, with the combination of income tax reaching 47% (45% national + up to 3% regional surcharge in Catalonia, Andalusia, and other regions), plus the notorious autonomo social security system. The cuota de autonomo (mandatory monthly self-employed contribution) was reformed in 2023 to a quota-based system: contributions range from EUR 200/month to EUR 530/month depending on net income. However, the mandatory minimum means that even low-earning autonomos must pay social security contributions.

For company owners (administradores de sociedades), the situation involves both the IS (Impuesto de Sociedades, corporate tax) at 25% (23% for smaller companies), and dividend taxation included in the ahorro (savings) income brackets at rates ranging from 19% to 28% for amounts above EUR 300,000. The combined effective rate on company profits distributed as dividends reaches approximately 43-46%.

Spain is also notable for the regional variation in tax rates, particularly the wealth tax (Impuesto sobre el Patrimonio). While the Madrid regional government applies a 100% bonus effectively eliminating the wealth tax, other regions like Catalonia charge up to 3.48% on high-net-worth individuals. This has made Madrid a domestic migration destination within Spain, but many entrepreneurs look further.

The Beckham Law (Ley Beckham, now called Regimen Especial de Trabajadores Desplazados) offers a 24% flat tax for qualifying professionals who move to Spain, but it applies for only 6 years and has eligibility restrictions. Cyprus Non-Dom is permanent, simpler, and offers a lower effective rate.

Spain Tax Burden at a Glance

| Tax type | 🇪🇸 Spain |

|---|---|

| Income tax | Up to 47% (national 45% + regional up to 3%) |

| Corporate tax | 25% (23% for SMEs under EUR 1M revenue) |

| Capital gains tax | 19-28% (progressive brackets on savings income) |

| Dividend tax | 19-28% (included in savings income) |

| Social contributions | ~6.35% employee + ~29.9% employer; autonomo: EUR 200-530/month mandatory quota |

| Effective rate | ~40-50% |

Tax Comparison: Spain vs Cyprus

On EUR 100,000 of business revenue:

Spain (SL + dividends): IS at 25% = EUR 25,000. Remaining EUR 75,000 as dividends, taxed at savings income rates (approximately 24% blended) = EUR 18,000. Total approximately EUR 43,000 (43% effective). Add autonomo contributions for the director: EUR 2,400-6,360 per year.

Spain (SL + salary): IS at 25% = EUR 25,000 (though salary reduces taxable profit). Salary subject to IRPF at up to 47% + employee social security ~6.35%. This route can reach 47-52% effective.

Cyprus (Ltd + Non-Dom): Corporate tax at 15% = EUR 15,000. Low salary plus dividends at 0% income tax + 2.65% GHS. Total approximately EUR 5,000 (5% effective).

Annual savings: approximately EUR 38,000-45,000 on EUR 100,000 revenue.

Spanish content creators and YouTubers have been among the most high-profile cases of this tax arbitrage, with several well-known creators relocating to Andorra. However, Andorra comes with significant lifestyle restrictions (limited international connections, small country). Cyprus offers comparable or better effective rates with full EU membership, Mediterranean climate, English-language environment, and strong international connectivity.

Interactive Tax Calculator

Spain

Effective rate

45%

Est. tax: €45,000

Cyprus (Non-Dom)

Effective rate

5%

Est. tax: €5,000

Annual savings by moving to Cyprus

€40,000

Estimates based on effective rates. Consult a tax advisor for your specific situation.

Cyprus Non-Dom: ~5% effective tax

The alternative most entrepreneurs do not know about

- ✓15% corporate tax (flat, no surcharges)

- ✓0% dividend income tax (Non-Dom)

- ✓2.65% GHS on all income

- ✓No wealth tax, no inheritance tax

- ✓60-day rule for flexible tax residency

- ✓Full EU membership and treaty network

Double Tax Treaty: Spain - Cyprus

Spain and Cyprus have a double tax treaty in force. Key provisions: dividends 10% (5% if the beneficial owner holds at least 25% of the capital), interest 10%, royalties 10%. Spain has an exit tax (articulo 95bis LIRPF) on unrealized capital gains for taxpayers who have been Spanish residents for at least 10 of the last 15 years and hold shares with unrealized gains above EUR 4,000 (with portfolio value above EUR 1 million or gains in a single company above EUR 500,000). For EU moves, payment can be deferred. Spain's tax authority (Agencia Tributaria, Hacienda) is known for aggressive enforcement of residency rules and anti-avoidance provisions.

Leaving Spain: Exit Process

Spain has specific exit requirements and an important exit tax:

Exit tax (articulo 95bis LIRPF): If you have been a Spanish resident for at least 10 of the last 15 tax years and your share portfolio has unrealized gains above EUR 4,000 with total portfolio value above EUR 1 million (or single company gains above EUR 500,000), Spain assesses an exit tax. For moves to EU member states like Cyprus, payment is deferred until actual disposal. Annual communication to Hacienda is required.

Padron Municipal deregistration: You must request a baja del padron municipal (removal from the municipal register) at your local ayuntamiento. This is important as the padron is used as evidence of residence in Spain.

Modelo 030: File Modelo 030 with Hacienda to notify the change of address and update your census data. This formally registers your non-residency with the Spanish tax authority.

Final IRPF return: File a final Spanish income tax return (declaracion de la renta) covering the year of departure. Mark the return as "periodo impositivo inferior al ano natural" (tax period shorter than the full calendar year).

Autonomo deregistration: If registered as autonomo, file a baja (deregistration) with the RETA (Regimen Especial de Trabajadores Autonomos). This stops ongoing social security contributions.

SL considerations: If maintaining a Spanish SL, ensure management is genuinely conducted from Cyprus to avoid Spanish corporate residency.

Cost of Living: Spain vs Cyprus

Spain offers a range of costs depending on location, with Madrid and Barcelona being most expensive:

Housing: Barcelona EUR 1,200-2,000 rent vs Larnaca EUR 550-750 (savings: 55-65%). Madrid EUR 1,100-1,800. Smaller cities EUR 600-1,000. Groceries: Spain EUR 250-350 vs Cyprus EUR 250-350 (comparable) Dining out: Spain EUR 200-300 vs Cyprus EUR 150-200 (Spain slightly more expensive in major cities) Transport: Spain EUR 80-130 vs Cyprus EUR 100-150 (comparable; Spain has better public transport in cities) Utilities: Spain EUR 120-180 vs Cyprus EUR 100-150 (similar Mediterranean climate)

Total monthly: Spain EUR 2,500-3,300 (major cities) vs Cyprus EUR 1,400-1,900

The climate profiles are broadly similar (Mediterranean, warm and sunny), though Cyprus has more reliable summers and milder winters. For entrepreneurs moving from Barcelona or Madrid, the cost of living savings are meaningful, especially on housing. The absence of the autonomo mandatory contribution (EUR 2,400-6,360/year) represents an immediate savings.

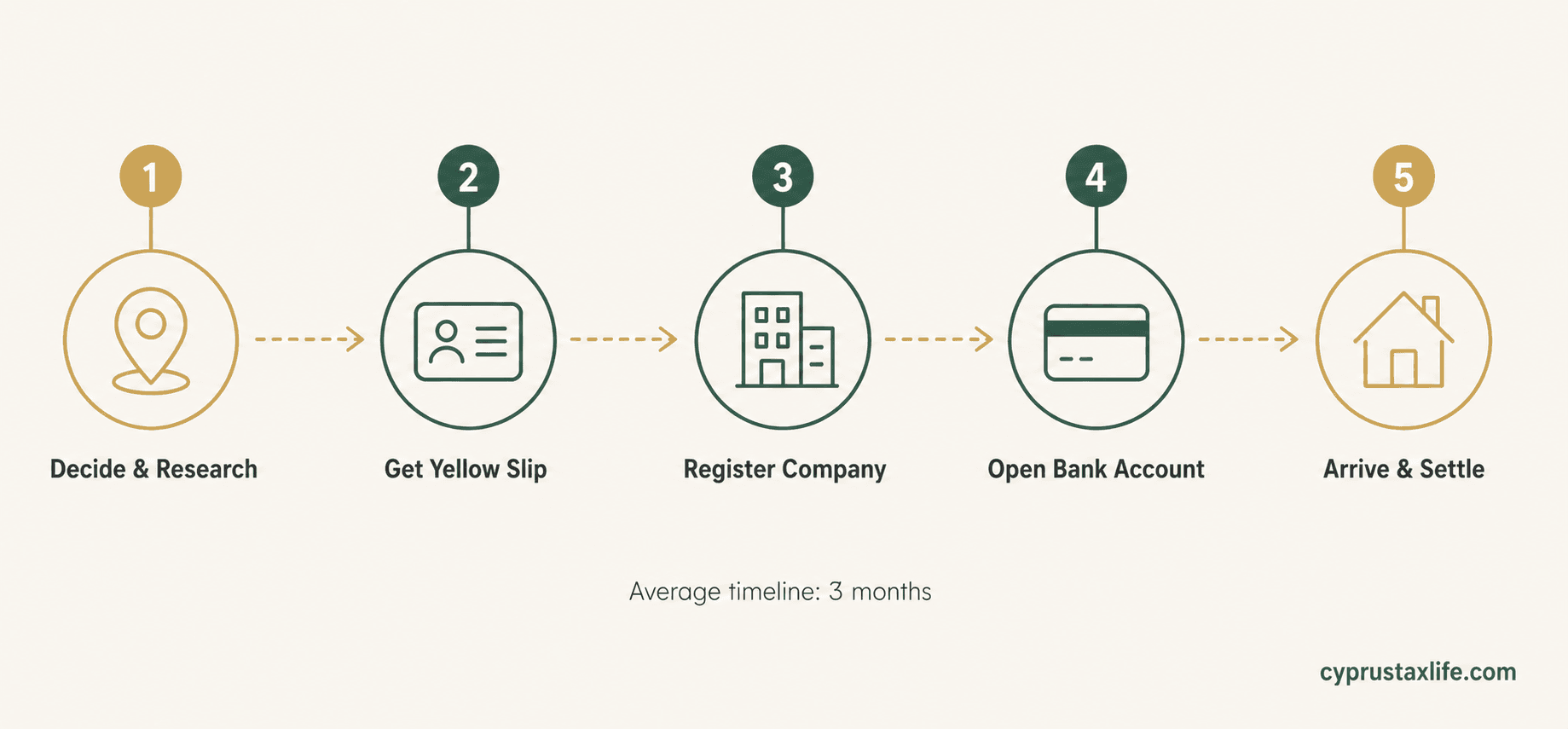

Step-by-Step Relocation Checklist

Consult a Spanish tax advisor about exit tax exposure (articulo 95bis LIRPF)

Research Cyprus cities, particularly Limassol and Larnaca (Spanish-speaking communities in both)

Set up a Cyprus Ltd company (approximately EUR 2,100)

Find accommodation in Cyprus and sign a rental contract

Request baja del padron municipal at your local ayuntamiento

File Modelo 030 with Hacienda (change of census data and address)

File baja in RETA (deregister from autonomo social security)

File your final Spanish IRPF return for the departure year

Apply for Cyprus tax residency (60-day or 183-day rule)

Register for Non-Dom status at the Cyprus Tax Department

Obtain your Yellow Slip (EU citizen registration)

Open a Cyprus bank account

Register for GHS healthcare

Set up payroll structure in Cyprus (low salary + dividends)

If exit tax applies, set up annual reporting arrangements with Hacienda

Learn more about Cyprus:

Frequently Asked Questions

Does Spain have an exit tax when moving to Cyprus?+

What is Modelo 030 and do I need to file it when leaving Spain?+

How does Cyprus compare to Andorra for Spanish entrepreneurs?+

Can I use the Cyprus 60-day rule as a Spanish citizen?+

What happens to my Spanish Social Security (Seguridad Social) pension?+

Is there a Spanish-speaking community in Cyprus?+

Sources and References

- PwC Worldwide Tax Summaries — Cyprus

- KPMG Cyprus — Tax and Advisory

- EY Cyprus — Tax Services

- Cyprus Ministry of Finance (mof.gov.cy)

Effective rates are approximations for entrepreneur structures (company + low salary + dividends). Consult a qualified tax advisor before making decisions.

Free, no commitment

Moving to Cyprus or opening a company?

Tell us your situation and we'll connect you with our specialist expat advisory in Cyprus: Non-Dom tax, company setup and residency, done for you. Free consultation, no commitment.

Related Articles

Germany's exit tax (§6 AStG) taxes unrealised gains on shares >1% when you emigrate. Moving to Cyprus (EU): you can defer payment indefinitely. Full breakdown for German founders and investors.

Miriam Alonso

Miriam Alonso- Tax Planning

- Relocation

Canada's departure tax treats you as having sold your worldwide assets the day you stop being a tax resident. What is caught, what is exempt, how to defer it, and what the cost-base reset means for where you go next.

![Countries With No Property Tax [2026]: The Real Cost](https://cdn.sanity.io/images/glqahhks/production/6f7ea0efceed8a692ad7c3785efa8baaf4d1e208-1679x937.jpg?w=700&q=75&auto=format)

Compare countries with no property tax and the stamp duty they charge instead. See the 10-year holding cost that makes Cayman pricier than Portugal.

Miriam Alonso