Best Holding Company EU 2026: Cyprus vs 4 Countries

A holding company collects dividends from subsidiaries, holds intellectual property, or manages group restructuring. The country you choose for it determines your tax on incoming dividends, withholding tax on outgoing distributions, and compliance cost.

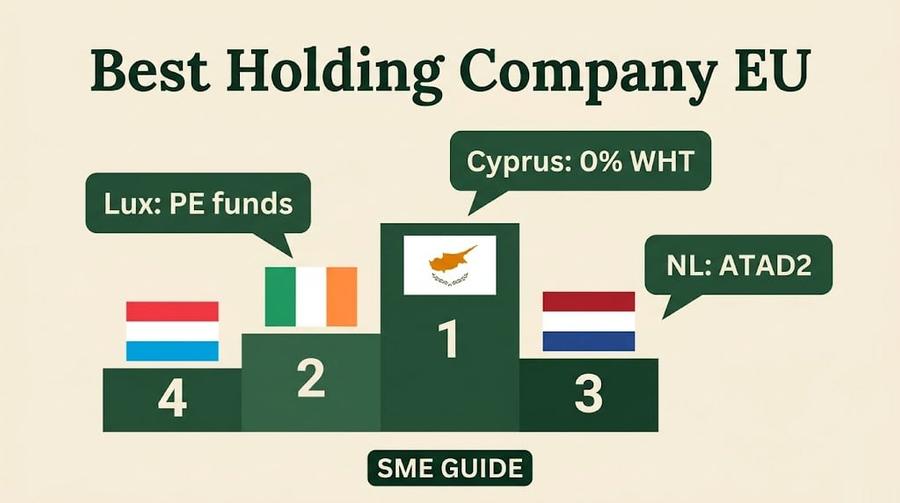

This guide compares the four main EU holding jurisdictions for SMEs and mid-market companies.

Comparison Table

| Feature | Cyprus | Netherlands | Luxembourg | Ireland |

|---|---|---|---|---|

| Corporate tax | 15% | 25.8% | 17-24.94% | 12.5% trading / 25% passive |

| Participation exemption | Yes (1%+ stake) | Yes (5%+ stake) | Yes (10%+ stake) | Yes (5%+ stake) |

| WHT outbound dividends | 0% | 15% (w/ exemptions) | 15% (w/ exemptions) | 25% (w/ exemptions) |

| WHT outbound interest | 0% | 0% | 0% | 20% (w/ exemptions) |

| Capital gains on shares | 0% | Exempt (participation) | Exempt (participation) | Exempt (participation) |

| IP Box | Yes (2.5%) | Yes (9%) | Yes (5.2%) | Yes (6.25%) |

| Annual compliance cost | EUR 3,000-6,000 | EUR 10,000+ | EUR 15,000+ | EUR 5,000-10,000 |

| English legal system | Yes (Common Law) | No | No | Yes (Common Law) |

Key criteria for evaluating EU holding company jurisdictions:

- Participation exemption: Cyprus and Netherlands offer full exemption on qualifying dividends received from subsidiaries

- Withholding tax on outbound dividends: Cyprus imposes 0% on dividends paid to all shareholders, outperforms most EU countries

- Capital gains on subsidiaries: Cyprus has 0% CGT on shares; Netherlands has a participation exemption on gains too

- Treaty network: Cyprus has 60+ double taxation treaties; Netherlands 100+, both excellent for international structures

- Substance requirements post-BEPS: Cyprus requires genuine management and control in Cyprus (at least director meetings in Cyprus, actual decision-making on the island)

- Cost of maintenance: Cyprus annual costs €1,500-3,000 vs Netherlands €5,000-10,000+

- Legal system: Cyprus uses common law (English-derived), familiar to UK and US lawyers

- Ruling availability: Cyprus does not issue formal advance rulings, but tax practice is well-established

Cyprus - Best for SMEs

Cyprus is the optimal jurisdiction for SMEs under EUR 20M revenue because of three factors: low corporate tax at 15%, unrestricted EU market access, and lean administrative structures. Non-Dom residents pay ~5% effective tax on foreign-sourced income. Capital gains are untaxed. Dividend income is tax-exempt. These provisions create cost-efficiency for growth-stage companies managing cash flow and reinvestment. Stamp duty on company formations is zero. The combination of structural tax advantages and EU regulatory alignment makes Cyprus significantly more attractive than comparable jurisdictions for scaling SMEs.

The 0% withholding tax on outbound dividends is the single most significant structural advantage Cyprus has over the Netherlands, Luxembourg and Ireland. In the other three jurisdictions, WHT applies at 15-25% on dividends paid to shareholders, and you must rely on tax treaties or EU directives to reduce or eliminate that charge. Cyprus charges zero by default, regardless of the shareholder's country of residence.

The participation exemption applies at 1% shareholding - the lowest minimum threshold of the four jurisdictions compared here. Netherlands requires 5%, Luxembourg 10%, and Ireland 5%. This matters for holding structures where you acquire minority stakes in operating companies.

Capital gains on shares are completely exempt in Cyprus. If your holding company sells its stake in a subsidiary, 0% Cypriot capital gains tax applies. This makes Cyprus ideal for holding companies that might exit individual subsidiaries over time.

Annual compliance costs in Cyprus are EUR 3,000-6,000 for a standard holding company structure. This includes mandatory audit (required even for small companies), accounting, registered agent and annual levy. In Luxembourg, the same compliance package costs EUR 15,000+ due to higher professional fees and stricter substance requirements.

Cyprus is a Common Law jurisdiction, inherited from British rule. Contracts, corporate structures and legal concepts follow the Common Law tradition familiar to English-speaking founders, US investors and UK-based advisors. Netherlands and Luxembourg operate under Civil Law systems, which creates additional complexity for Common Law trained advisors.

How Cyprus holding companies work: How Cyprus Holding Companies Pay 0% Tax on Dividends

Holding company guide: Holding Company in Cyprus

Netherlands - Old Standard, Now More Complex

The Netherlands remains a preferred holding jurisdiction due to its 100+ tax treaties, genuine participation exemption from 5% shareholding, and zero withholding tax on interest. Once the default jurisdiction for international groups in the 1990s-2000s, it now faces increased complexity from anti-abuse rules and BEPS compliance.

However, ATAD2 (the EU Anti-Tax Avoidance Directive 2, implemented in the Netherlands from 2022) closed most hybrid mismatch structures. The infamous "Dutch sandwich" and similar structures that used Netherlands-based entities to avoid tax in other jurisdictions no longer work. The ATAD2 rules are complex and require specialist advice to navigate.

The 25.8% Dutch corporate tax rate significantly reduces the attractiveness of the Netherlands vs Cyprus (15%) for companies that generate active income through the holding entity. For pure holding structures with participation exemption income, the corporate rate matters less, but it does affect the tax on management fees, royalties and other income that does not qualify for the exemption.

Dutch holding companies work well for large multinational groups that genuinely need the extensive treaty network and are willing to maintain substantive operations in the Netherlands. For SMEs, the compliance cost and complexity no longer justify the choice over simpler alternatives.

Luxembourg - For Funds and Family Offices

A SOPARFI offers participation exemption from 10% shareholding or EUR 1.2M acquisition cost, capital gains exemption on qualifying shareholdings, and access to 80+ tax treaties.

Luxembourg is best suited for: investment funds and fund management structures (Luxembourg is the second largest fund domicile in the world after the US), private equity holding structures, family offices managing EUR 100M+ in assets, and regulated financial activities where Luxembourg's regulatory framework is required.

For SMEs, the compliance cost makes Luxembourg impractical. A Luxembourg holding company requires: certified annual accounts (audit mandatory from certain thresholds), registered office with a licensed agent, economic substance requirements (local directors, genuine management), and ongoing regulatory filings. The total annual cost is EUR 15,000-25,000 before any actual business activity.

The Luxembourg SOPARFI is also subject to net wealth tax (NWT) of 0.5% on net assets, capped at EUR 500,000. For large asset bases, this is a meaningful ongoing cost.

Ireland - For US Market Access

Ireland taxes active trading income at a low rate, but passive holding income at 25%. Personal income tax reaches 55% (income tax plus PRSI plus USC), making Ireland unattractive for owner-managed companies where the owner also pays Irish personal tax.

Ireland's strongest advantage is the US connection: the large US multinational presence in Ireland (Google, Apple, Facebook, Microsoft) reflects years of consistent tax policy, a large English-speaking workforce, and the Common Law system. For companies seeking US venture capital investment or US corporate partnerships, an Irish entity is often easier to explain and structure.

Best for: companies accessing US market, US-backed venture capital, or tech companies using Ireland as EU headquarters. Less suitable for dividend-holding structures or owner-managed businesses where passive income is taxed at the higher rate.

Substance Requirements for All Four Jurisdictions

Post-2020 substance requirements across all four jurisdictions have increased significantly due to OECD BEPS Action 5 and EU Directive on Shell Companies (ATAD3). Holding companies now face stricter minimum activity standards. These rules require actual business operations, staff, management, and decision-making in the jurisdiction where incorporation occurs. Compliance involves demonstrating genuine economic substance beyond passive investment holding.

Cyprus: at least one resident director with genuine decision-making authority. Board meetings held in Cyprus. Cypriot bank account for company funds. Real economic activity or genuine management of investments.

Netherlands: a Dutch holding company must have Dutch-resident directors with genuine authority, board meetings in the Netherlands, and real substance. The Dutch tax authority (Belastingdienst) actively challenges thin substance arrangements.

Source: PwC Cyprus Tax Facts 2026. Rates and regimes current as of January 2026.

Luxembourg: similar requirements. CSSF (financial regulator) and Luxembourg tax authorities require genuine management presence. The EU Shell Companies Directive (Unshell), if adopted, would impose stricter minimum substance tests across all EU member states.

Ireland: the Revenue Commissioners apply a "mind and management" test. Key decisions must be made by directors who are physically present in Ireland when those decisions are taken. Merely having an Irish-resident director who rubber-stamps decisions made elsewhere is insufficient.

Verdict

Cyprus delivers lowest cost and fastest setup for single founders and small teams under EUR 20M with EU operations. The Netherlands or Luxembourg suit EUR 20M+ multinationals prioritizing treaty coverage and existing advisor networks. Luxembourg leads for investment funds and family offices managing EUR 100M+. Ireland fits US-connected tech companies and venture-backed startups.

The single most important variable: your planned exit strategy. If you intend to sell the holding company or its subsidiaries within 5-10 years, Cyprus's 0% capital gains on shares is a major advantage that compounds significantly at exit.

Tax Treaty Networks: Does It Matter?

Cyprus has 67 double tax treaties covering Russia, Ukraine, and most EU countries. Netherlands leads with 100+ treaties, particularly strong for US and Asian connections. Ireland maintains 76 treaties including a US agreement. Luxembourg has 83 treaties. Extensive networks matter most when your investment flows cross multiple jurisdictions or involve treaty-dependent structures. Cyprus excels for Eastern Europe and EU routes; Netherlands and Luxembourg dominate transatlantic and Asian corridors.

For most SME holding structures, the number of treaties matters less than the specific treaties with your operating countries. If your subsidiaries are in Germany, France, Spain and Poland, all four jurisdictions have treaties covering those countries. The treaty quality (withholding tax rates, tie-breaker provisions) varies and should be checked for your specific structure.

The EU Parent-Subsidiary Directive eliminates withholding tax on intra-EU dividends between qualifying companies regardless of treaty status. A Cyprus holding company receiving dividends from a French subsidiary pays 0% WHT under the Directive, not the Cyprus-France treaty rate. This makes the treaty network less critical for purely intra-EU structures.

Total Cost of Ownership: Cyprus vs Alternatives

Compliance costs often exceed tax savings for SMEs. A EUR 500K profit center pays EUR 15,000/year in Luxembourg compliance costs versus EUR 4,000 in Cyprus, saving EUR 11,000 annually before tax. Over 10 years, compliance cost savings alone reach EUR 110,000. For modest profit centers, administrative efficiency rivals tax rate advantages.

Cyprus annual costs breakdown: mandatory audit (EUR 1,500-3,000 for a standard holding company), accounting and bookkeeping (EUR 1,000-2,000/year), registered agent and address (EUR 500-1,000/year), annual levy to the government (EUR 350), total: EUR 3,350-6,350.

Netherlands annual costs: Dutch holding companies with substance requirements typically spend EUR 10,000-20,000/year on local management services, audit (mandatory from certain thresholds), accounting, and regulatory compliance. For smaller structures, the minimum substance package (a Dutch director service) runs EUR 7,000-12,000/year.

The cost differential is most significant in the first 3-5 years when the holding company is growing but not yet generating the dividend or capital gain that makes the structure valuable. During that period, Cyprus saves EUR 5,000-15,000/year in compliance costs vs Netherlands or Luxembourg.

Frequently Asked Questions

What is a participation exemption?

Does Cyprus charge withholding tax on dividends?

Is Luxembourg still good for holding companies?

What substance is required for a Cyprus holding company?

Can a Cyprus holding company own subsidiaries in other EU countries?

How much does a Cyprus holding company cost to run per year?

Sources: PwC Cyprus Tax Facts 2026, Cyprus Tax Department.

Need personalized advice? Book a consultation with an expat tax specialist.

Sources: PwC Cyprus Tax Facts 2026, Cyprus Tax Department.

Want to set up a Cyprus holding company? Get expert advice

For the Cyprus structure, the Company vs Self-Employed Calculator models net income through a Cyprus Ltd with Non-Dom dividends versus salary or sole trader - useful for comparing the real after-tax numbers against other jurisdictions.

![Cyprus Ltd vs Irish Ltd: Company Tax Compared [2026]](https://cdn.sanity.io/images/glqahhks/production/84e3d82538a859345d8d2447e8e097c5777fb238-1679x937.png?w=700&q=75&auto=format)

![Cyprus vs Malta Company Formation [2026]](https://cdn.sanity.io/images/glqahhks/production/97db89d0ce729a9e931d09bc1522631faa6c3474-1679x937.png?w=700&q=75&auto=format)