Lowest VAT Rates in Europe by Country (2026)

VAT rates in the EU range from 17% in Luxembourg to 27% in Hungary. For businesses deciding where to register, and for consumers comparing costs, understanding which countries have the lowest VAT matters.

This guide ranks all EU countries by standard VAT rate and explains what the rates mean in practice for businesses operating across borders.

EU VAT Rates - Full Ranking (2026)

Source: PwC Cyprus Tax Facts 2026. VAT rates across Europe verified as of January 2026.

| Country | Standard VAT | Key Reduced Rates |

|---|---|---|

| Luxembourg | 17% | 8% reduced, 3% super-reduced |

| Malta | 18% | 5% reduced, 0% on food/medicine |

| Cyprus | 19% | 9% hotels/restaurants, 5% food/medicine |

| Germany | 19% | 7% reduced |

| Romania | 19% | 9% food, 5% books/medicine |

| Bulgaria | 20% | 9% tourism accommodation |

| France | 20% | 10% reduced, 5.5% food |

| Netherlands | 21% | 9% reduced |

| Belgium | 21% | 12% reduced, 6% essential goods |

| Czech Republic | 21% | 12% and 0% reduced |

| Sweden | 25% | 12% and 6% reduced |

| Denmark | 25% | No reduced rates |

| Norway | 25% | 15% food, 12% transport (non-EU) |

| Hungary | 27% | 18% and 5% reduced |

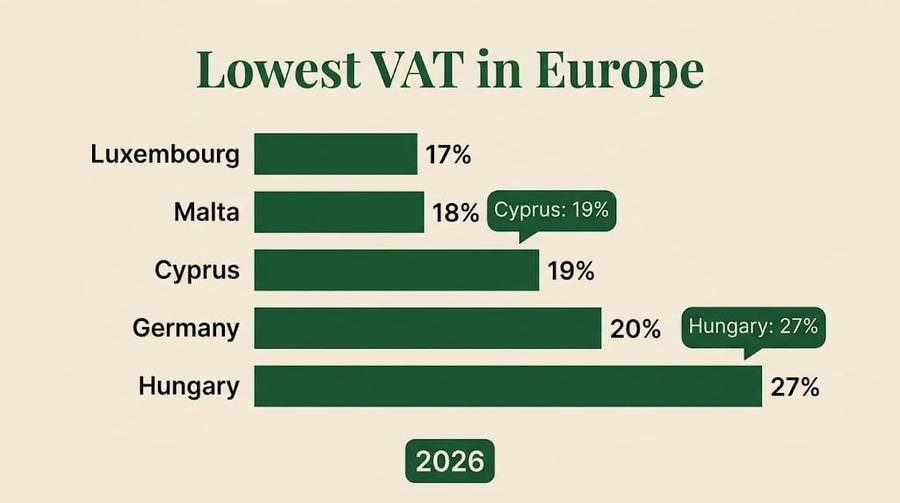

EU countries with the lowest standard VAT rates (2026):

- Luxembourg: 17%, EU's lowest standard rate

- Malta: 18%

- Cyprus: 19%, also has9% reduced rate and 5% super-reduced

- Germany: 19%, with 7% reduced rate on essentials

- Romania: 19%

- Bulgaria: 20%

- France: 20%

- Italy: 22%

- Sweden: 25%

- Hungary: 27%, EU's highest VAT rate

Special low-VAT categories in Cyprus:

- 9% on: restaurants, hotels, passenger transport, live events

- 5% on: some food items, books, pharmaceuticals, medical devices

- 0% on: exports, intra-EU B2B services, international transport

Why Cyprus VAT Is Competitive

Cyprus applies a 19% standard VAT rate, matching Germany and Romania but below France (20%), Italy (22%), Spain (21%), Sweden (25%), and Hungary (27%). This positions Cyprus as competitive within the EU for VAT efficiency.

Key reduced rates in Cyprus: 9% for hotels, restaurants and tourist services. 5% for food, books, pharmaceuticals and renovation services. 0% for exports and internationally provided services where the customer is outside Cyprus.

The reduced rate on hotel and restaurant services (9%) is one of the more generous hospitality rates in the EU. Many countries apply a higher reduced rate to this sector, or the full standard rate. This makes Cyprus an attractive base for hospitality businesses serving international clients.

For businesses operating in Cyprus, the 19% VAT rate means you reclaim input VAT on your purchases at that rate. If your Cyprus company buys office equipment, professional services or business travel within Cyprus, you reclaim 19% VAT on those costs. In Hungary, you would be reclaiming 27%.

Full Cyprus VAT guide: VAT in Cyprus: Rates, Registration Threshold and Filing

Does VAT Rate Matter for Business Registration?

VAT rate differences no longer matter for B2C digital services after the 2021 EU One Stop Shop reform. Your customer's country VAT rate applies regardless of where you register, so a Luxembourg registration won't give you a 17% rate on German sales. This closed a major tax advantage that low-VAT countries previously held.

Before OSS, a digital service provider registered in Luxembourg could charge all EU customers at 17% VAT regardless of where the customer was located. Amazon, Apple and Spotify famously used Luxembourg for exactly this reason. Since July 2021, that advantage is gone for B2C cross-border digital services.

Where VAT rate still matters: (1) Local services and physical goods sold domestically. (2) VAT on your own purchases (input VAT) from local suppliers. (3) B2B transactions under the reverse-charge mechanism where you are the buyer. (4) Real estate transactions and property-related services delivered locally.

For most international businesses, the VAT rate of your company's country affects mainly your local overhead costs - office rent, local professional services, utilities. Cross-border B2C digital revenue is taxed at destination regardless of where you are registered. Cross-border B2B services are typically reverse-charged.

The practical conclusion: do not choose a company location solely for VAT rate. The corporate tax rate, dividend withholding tax, and personal tax treatment of profits are far more significant factors for most business models.

Cyprus VAT Registration - Key Facts

You must register for VAT in Cyprus when your annual taxable turnover reaches EUR 15,600. This threshold is among the EU's lower limits - the EU minimum for cross-border OSS purposes is EUR 10,000, though member states set domestic thresholds independently. The UK threshold, by comparison, is GBP 90,000.

Voluntary registration: businesses below the EUR 15,600 threshold can register voluntarily if they wish to reclaim input VAT on purchases. This is often beneficial for businesses with significant startup costs or that purchase heavily from VAT-registered suppliers.

Filing frequency: VAT returns are filed quarterly in Cyprus via the TAXISnet online portal. Returns must be submitted and payment made within 40 days of the end of each quarter. Late submission carries a fixed penalty plus interest on unpaid amounts.

Intrastat and EC Sales List: businesses trading goods or services within the EU above the applicable thresholds must also file Intrastat reports (for goods) and EC Sales Lists (for services). These are reporting requirements separate from the VAT return itself.

The VAT registration number format in Cyprus is "CY" followed by 9 digits. This number appears on all invoices issued to EU business customers and is required for EU reverse-charge transactions.

Filing deadlines: Cyprus Tax Filing Deadlines 2026

Company setup: Cyprus Company Formation Guide

How VAT Works for a Cyprus Company in Practice

Standard domestic sales require you to charge 19% VAT on the invoice and collect it from the customer. File quarterly VAT returns and pay the net amount (VAT collected minus VAT paid on purchases) to the tax authority.

Exports to non-EU countries: zero-rated. No VAT is charged. You can still reclaim input VAT on costs related to those exports.

Sales to EU business customers: zero-rated under reverse-charge, provided you have the customer's valid VAT number. You must include the EC Sales List entry and quote their VAT number on the invoice.

Sales to EU consumers (non-business): apply the OSS rules. Either register for OSS and charge VAT at the customer's country rate, or register for VAT in each country where your B2C sales exceed EUR 10,000 per year (combined threshold across all EU countries).

Purchases from EU suppliers: if they supply you without charging VAT (reverse-charge basis), you must self-account for VAT in Cyprus on that purchase. This is a paper entry - you declare the VAT due and simultaneously claim the input VAT credit, usually netting to zero if you are fully taxable.

VAT Refunds and Input Tax Recovery

A Cyprus-registered business can reclaim input VAT paid on purchases against VAT collected on sales. Excess input VAT generates a refund from the Cyprus Tax Department. To qualify, the business must be VAT-registered and maintain proper documentation of all VATable transactions. Refund timing depends on the application method and verification requirements.

Common situations where input VAT recovery creates a cash benefit: (1) A new business making significant startup purchases before revenue begins. (2) An export-focused business that charges 0% on all sales but pays 19% on Cypriot purchases. (3) A business with a large capital expenditure (new equipment, office fit-out) in a quarter with low revenue.

Refund processing in Cyprus: the tax authority is required to process refund applications within 30 days. In practice, refunds for amounts over EUR 3,000 may be subject to additional review. The Cyprus Tax Department has improved its refund processing in recent years, but larger refunds can take 60-90 days in practice.

VAT and international services: if your Cyprus company provides services to EU business clients, those are typically zero-rated under reverse-charge. You can still reclaim input VAT on your Cypriot costs related to those services. This is a key advantage for service businesses based in Cyprus serving EU corporate clients.

EU vs Non-EU VAT Systems

**Standard VAT rates outside the EU:**

UK: 20% (unchanged since 2011)

Switzerland: 8.1%

Norway: 25%

UAE: 5% (introduced 2018, no reduced rates)

For businesses operating between the EU and non-EU countries, the place of supply rules determine which country's VAT system applies. Services supplied to non-EU business customers are generally outside the scope of EU VAT entirely. Goods exported to non-EU countries are zero-rated for EU VAT purposes.

For companies choosing between EU and non-EU domiciles purely on VAT grounds: the choice rarely matters for international service businesses where most revenue is zero-rated or reverse-charged. The EU VAT system's OSS simplification (a single registration covering B2C sales across all EU countries) is actually an advantage of EU membership that non-EU businesses must work around.

Frequently Asked Questions

Which EU country has the lowest VAT?

What is VAT in Cyprus?

Can I register for VAT in Luxembourg to pay less VAT on EU sales?

Is there a VAT registration threshold in Cyprus?

Is there VAT on residential rental in Cyprus?

Does Hungary have the highest VAT rate in Europe?

Sources: PwC Cyprus Tax Facts 2026, Cyprus Tax Department.

Need personalized advice? Book a consultation with an expat tax specialist.

Sources: PwC Cyprus Tax Facts 2026, Cyprus Tax Department.

Questions about VAT in Cyprus? Get expert advice

For Cyprus specifically, use our Cyprus VAT Calculator to calculate VAT at the standard 19% rate, reduced 9% rate, or super-reduced 5% rate - and see the net price excluding VAT.

![Cyprus Ltd vs Irish Ltd: Company Tax Compared [2026]](https://cdn.sanity.io/images/glqahhks/production/84e3d82538a859345d8d2447e8e097c5777fb238-1679x937.png?w=700&q=75&auto=format)

![Cyprus vs Malta Company Formation [2026]](https://cdn.sanity.io/images/glqahhks/production/97db89d0ce729a9e931d09bc1522631faa6c3474-1679x937.png?w=700&q=75&auto=format)