Quick Answer

Cyprus has 0% capital gains tax on shares, ETFs, funds, and investments. Only immovable property located in Cyprus is taxed at 20% CGT. Key exemptions: €85,430 lifetime allowance on your primary residence, €25,629 for agricultural land. Non-residents pay Cyprus CGT only on Cyprus property — not on shares. Crypto gains are taxed at 8% (new flat rate, 2026).

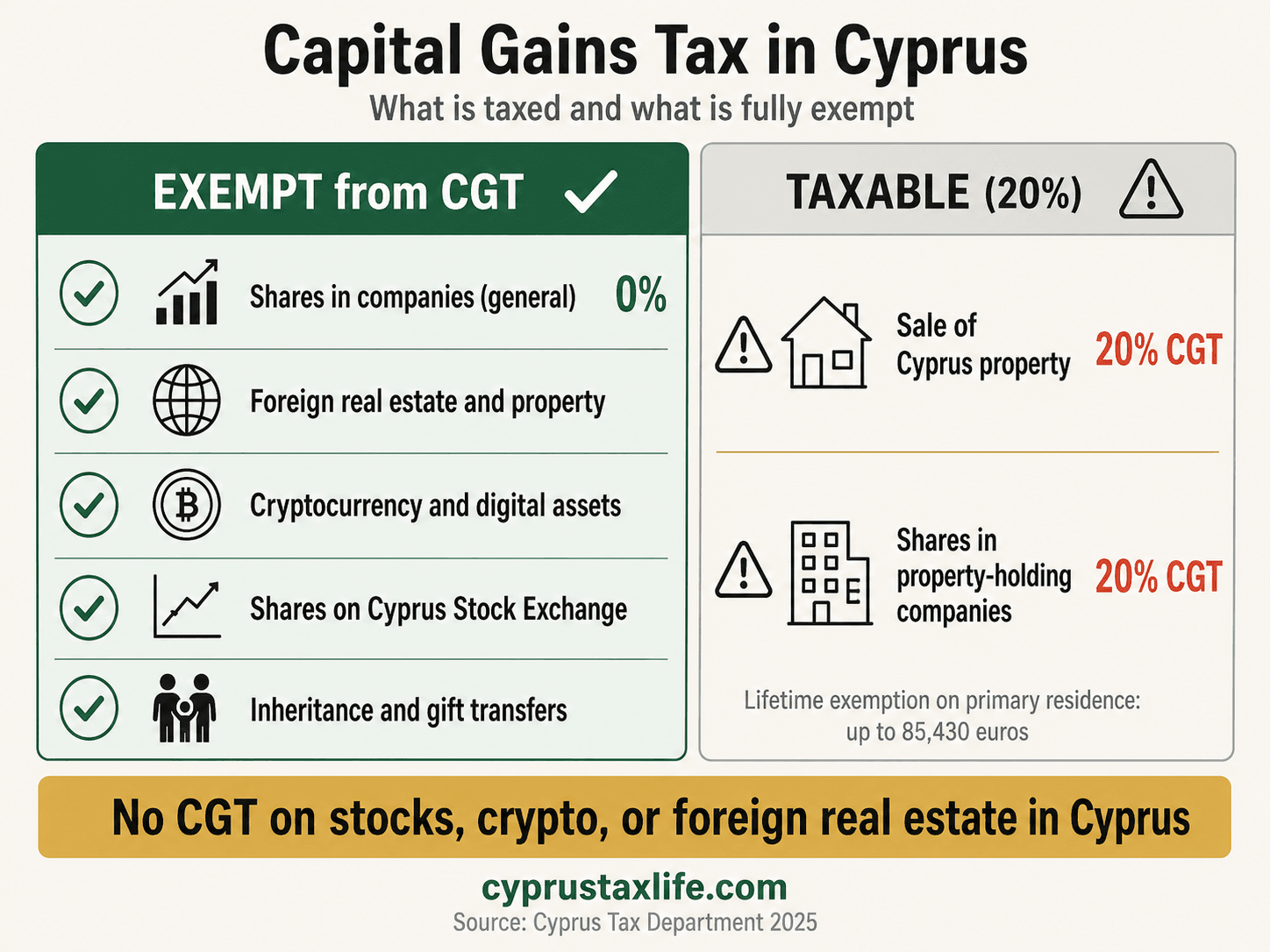

Capital Gains Tax in Cyprus: 0% on Shares and Securities

Cyprus applies 0% capital gains tax on shares, funds, and most financial instruments. Only gains from Cyprus real estate are subject to CGT at 20%.

Last updated:

Capital Gains Tax in Cyprus: The Short Answer

Cyprus charges capital gains tax (CGT) at 20% on profits from the disposal of immovable property located in Cyprus only. All other asset classes, company shares, ETFs, bonds, cryptocurrency, foreign property, precious metals, are exempt from CGT at 0%. This is one of the most favourable CGT regimes in the EU.

For comparison: the UK charges 20-24% CGT on shares and property, Germany charges income tax rate (up to 26.375%) on shares, France 30% on investment income. An investor selling €500,000 of shares or crypto in Cyprus pays no CGT. The same disposal in the UK could trigger a €95,000-120,000 tax bill.

What Is and Is Not Subject to Capital Gains Tax in Cyprus

- ✅ EXEMPT: Shares and securities listed on any recognised stock exchange

- ✅ EXEMPT: Unlisted company shares (Cyprus or foreign)

- ✅ EXEMPT: Cryptocurrency, confirmed by Cyprus Tax Department circular

- ✅ EXEMPT: Foreign real estate (property outside Cyprus)

- ✅ EXEMPT: ETFs, bonds, options and other financial instruments

- ⚠️ TAXED at 20%: Cyprus immovable property (land and buildings in Cyprus)

- ⚠️ TAXED at 20%: Shares in companies whose value derives >50% from Cyprus immovable property

The €17,086 lifetime exemption applies to all Cyprus property disposals in aggregate (not per transaction). Once that exemption is used, all further Cyprus property gains are taxed at 20%.

Cyprus CGT for Non-Residents: What Changes

Cyprus CGT is an asset-based tax, not a residence-based one. The taxable event depends on the nature of the asset, not where the seller lives.

Non-Residents Selling Cyprus Property

Non-residents selling Cyprus immovable property are subject to the full 20% CGT on the net gain - the same rate as residents. There is no reduced rate for non-residents, and no double tax treaty in force eliminates Cyprus CGT on Cyprus-sited property. Most treaties use the source-country principle for immovable property, meaning Cyprus retains the right to tax the gain.

Non-residents may still claim the lifetime personal exemptions: €17,086 for a property used as a main residence, and €85,430 for residential property that served as a principal private residence at any time.

Non-Residents Selling Shares or Foreign Assets

Non-residents have 0% Cyprus CGT on share disposals and gains from assets located outside Cyprus - identical treatment to residents. There is no withholding tax on share gains paid to non-residents and no obligation to file a Cyprus tax return solely because of a share disposal.

Practical Implication for Incoming Relocators

If you are planning to relocate to Cyprus and hold a large share portfolio, you do not need to liquidate it before moving. Gains realised after becoming a Cyprus tax resident continue to attract 0% CGT, and there is no exit tax triggered by establishing Cyprus tax residency - unlike Germany or the Netherlands, which impose departure taxes on unrealised share gains.

Cyprus CGT Indexation Table 1980-2025

Multiply the original purchase price by the factor for the year of acquisition to get the inflation-adjusted (indexed) cost. This reduces the taxable gain. The indexed cost is then subtracted from the sale price before applying the 20% CGT rate.

| Year of Purchase | Indexation Factor | Example: €100,000 purchase indexed to |

|---|---|---|

| 1980 | 9.05 | €905,000 |

| 1981 | 8.26 | €826,000 |

| 1982 | 7.52 | €752,000 |

| 1983 | 6.98 | €698,000 |

| 1984 | 6.49 | €649,000 |

| 1985 | 5.79 | €579,000 |

| 1986 | 5.40 | €540,000 |

| 1987 | 5.15 | €515,000 |

| 1988 | 4.87 | €487,000 |

| 1989 | 4.49 | €449,000 |

| 1990 | 3.74 | €374,000 |

| 1991 | 3.44 | €344,000 |

| 1992 | 3.20 | €320,000 |

| 1993 | 2.98 | €298,000 |

| 1994 | 2.78 | €278,000 |

| 1995 | 2.62 | €262,000 |

| 1996 | 2.48 | €248,000 |

| 1997 | 2.37 | €237,000 |

| 1998 | 2.28 | €228,000 |

| 1999 | 2.18 | €218,000 |

| 2000 | 2.09 | €209,000 |

| 2001 | 2.01 | €201,000 |

| 2002 | 1.93 | €193,000 |

| 2003 | 1.87 | €187,000 |

| 2004 | 1.78 | €178,000 |

| 2005 | 1.67 | €167,000 |

| 2006 | 1.60 | €160,000 |

| 2007 | 1.53 | €153,000 |

| 2008 | 1.45 | €145,000 |

| 2009 | 1.42 | €142,000 |

| 2010 | 1.42 | €142,000 |

| 2011 | 1.37 | €137,000 |

| 2012 | 1.32 | €132,000 |

| 2013 | 1.29 | €129,000 |

| 2014 | 1.28 | €128,000 |

| 2015 | 1.28 | €128,000 |

| 2016 | 1.27 | €127,000 |

| 2017 | 1.26 | €126,000 |

| 2018 | 1.23 | €123,000 |

| 2019 | 1.22 | €122,000 |

| 2020 | 1.22 | €122,000 |

| 2021 | 1.19 | €119,000 |

| 2022 | 1.12 | €112,000 |

| 2023 | 1.08 | €108,000 |

| 2024 | 1.06 | €106,000 |

| 2025 | 1.03 | €103,000 |

Approximate factors based on Cyprus Consumer Price Index series. Source: Cyprus Inland Revenue Department (Cap. 344). Verify the current year factor at taxdept.mof.gov.cy before filing a CGT return. Factors for years after 2025 are updated annually.

Key Facts 2026

| Capital gains on shares and securities | 0% |

| Capital gains on crypto (Non-Dom) | 0% |

| Capital gains on Cyprus real estate | 20% |

| Capital gains on overseas property | 0% |

| Primary residence lifetime exemption | EUR 85,430 |

| Agricultural use lifetime exemption | EUR 17,086 |

| Indexation allowance on property | Yes (purchase price adjusted for inflation) |

Free, no commitment

Moving to Cyprus or opening a company?

Tell us your situation and we'll connect you with our specialist expat advisory in Cyprus: Non-Dom tax, company setup and residency, done for you. Free consultation, no commitment.

Frequently Asked Questions

Is there capital gains tax in Cyprus on shares?

What is the capital gains tax rate on property in Cyprus?

How is the CGT on Cyprus property calculated?

Are crypto gains subject to capital gains tax in Cyprus?

What is the 8% crypto tax rate in Cyprus and how does it work?

Does DAC8 affect crypto reporting for Cyprus tax residents in 2026?

Does Non-Dom status give any additional CGT advantages in Cyprus?

Do I pay CGT in Cyprus on gains from selling a foreign company?

Is there a minimum holding period to avoid CGT on shares in Cyprus?

As a non-resident, do I pay Cyprus CGT when selling a Cyprus property?

How does the Cyprus CGT indexation allowance reduce the taxable gain?

What changed with capital gains tax in Cyprus in the 2026 tax reform?

Cryptocurrency disposal gains became taxable at a flat 8% from 1 January 2026 under Article 20E, ending their previous tax-exempt status. Disposals (selling, swapping, using crypto to pay) are now taxable income; holding crypto remains tax-free. This was the main CGT-related change in the 2026 reform, shifting crypto treatment from outside Cyprus's tax scope into a standalone income tax regime.

The core CGT rules on immovable property (20% on net gains) and securities (0%) were not changed by the 2026 reform. The lifetime exemptions of €17,086 to €85,430 on property remain in place. There is no new CGT on shares, ETFs, or bonds.

How can I legally reduce or avoid capital gains tax in Cyprus?

Capital gains tax in Cyprus can be eliminated through three legal strategies. Hold investments as shares or securities: disposals of shares, ETFs, bonds, and other securities incur 0% CGT regardless of gain size or holding period. Use lifetime exemptions on property: up to €85,430 on principal private residence (occupied as main home for at least 5 years), €17,086 on agricultural land, and €25,629 on other property. Apply indexation allowance: purchase price adjusts for inflation, substantially reducing taxable gain on older property.

Related Guides

Sources

Cyprus Capital Gains Tax Law (Cap. 344). 2026 Cyprus Tax Reform Package. Updated: April 2026.

For cryptocurrency disposals, use our Cyprus Crypto Tax Calculator to calculate the 8% flat rate on your gains. For property sales, the Cyprus Capital Gains Tax Calculator applies the indexation formula and lifetime exemptions automatically.

Cyprus has 0% capital gains tax on shares, ETFs, and crypto — and is one of only two EU member states with this advantage. See which other countries offer 0% CGT in our comparison of countries with no capital gains tax.

Capital Gains Tax in Cyprus for Non-Residents

Non-residents have very limited Cyprus CGT exposure. The rule is straightforward: you pay Cyprus CGT only if you dispose of immovable property physically located in Cyprus. All other asset classes — shares, bonds, funds, crypto, foreign property — are outside the scope of Cyprus CGT for non-residents.

Non-Resident Property Sales

A non-resident who sells a Cyprus apartment or plot of land pays 20% CGT on the net gain, calculated in exactly the same way as for a Cyprus resident. The same lifetime exemptions apply: EUR 85,430 for a principal residence (if you lived in the property), EUR 25,629 for agricultural land. Indexation relief also applies. There is no higher rate or additional withholding for non-residents.

The CGT liability must be declared and paid to the Cyprus Tax Department before the property transfer is registered at the Land Registry. The Land Registry will not complete the title transfer until a CGT clearance certificate (form N.313) is issued by the Tax Department, confirming that either CGT has been paid or no CGT is due.

Non-Resident Share Disposals: 0% CGT

Non-residents pay 0% Cyprus CGT when selling shares in Cyprus companies (listed or unlisted), provided the company does not derive more than 50% of its value from Cyprus immovable property. There is no withholding obligation on the Cyprus company when it facilitates a share sale between non-resident parties. No Cyprus tax return is required for non-residents whose only Cyprus activity is the disposal of qualifying shares.

Filing Requirements for Non-Residents with Cyprus CGT

Non-residents who sell Cyprus immovable property must file a CGT return (form IR167) within 30 days of the disposal date. Payment of the CGT is due at the same time. The gain is calculated in EUR regardless of the currency in which the sale is denominated. Non-residents are not required to register for income tax or file an income tax return unless they have additional Cyprus-source income beyond the property gain.

Frequently Asked Questions

Do non-residents pay capital gains tax in Cyprus?

Non-residents pay Cyprus capital gains tax only on gains from the disposal of immovable property located in Cyprus (land and buildings). The rate is 20% on the net gain after allowable deductions. Gains from shares, securities, and crypto are exempt from CGT regardless of whether you are resident or non-resident.

There is no CGT on share disposals for anyone in Cyprus. Non-residents also do not pay Cyprus income tax on passive income (dividends, interest) from Cyprus sources if they have no permanent establishment in Cyprus.

How is capital gains tax calculated in Cyprus on property?

Cyprus CGT on immovable property is calculated as: (Sale price minus Acquisition cost minus Allowable deductions) multiplied by 20%. Allowable deductions include the original purchase price indexed for inflation using the official CPI index, legal and professional fees, transfer fees paid at acquisition, and capital improvements.

Each individual has a lifetime exemption: EUR 17,086 for a main residence lived in for at least 5 years, EUR 25,629 for agricultural land transferred to a family member, or EUR 85,430 as a general lifetime exemption. Shares and securities are entirely exempt from CGT.

Did the 2026 tax reform change capital gains tax in Cyprus?

Yes - the 2026 reform introduced a new 8% flat rate on gains from the disposal of crypto-assets (Bitcoin, Ethereum, NFTs, tokens). Previously, crypto gains had no specific CGT treatment and were generally not taxable in Cyprus.

For shares and other securities, the existing 0% CGT rule remains unchanged. For immovable property, the 20% CGT rate also remains unchanged. The most significant change for investors is the new 8% crypto rate effective 1 January 2026. Non-dom status does not exempt crypto gains - the 8% applies to all Cyprus tax residents.

Do I pay capital gains tax on shares in Cyprus?

No. Cyprus charges 0% capital gains tax on the disposal of shares and securities. This applies to listed shares (any recognised stock exchange), unlisted private company shares, ETFs, bonds, mutual funds, and other financial instruments. There is no holding period requirement. The 0% exemption applies to both Cyprus tax residents and non-residents.

What are the capital gains tax exemptions in Cyprus?

Cyprus CGT exemptions include: (1) All shares and securities — 0% CGT, unconditionally. (2) EUR 85,430 lifetime exemption on the sale of your primary residence in Cyprus. (3) EUR 25,629 lifetime exemption on agricultural land sold for continued agricultural use. (4) EUR 17,086 general personal lifetime exemption on all other Cyprus property gains. (5) Transfers on death (inheritance) — fully exempt. (6) Gifts between spouses and between parents and children — fully exempt. (7) Corporate reorganisations — exempt under specific conditions. (8) Foreign real estate — gains on property outside Cyprus are not subject to Cyprus CGT.

Does a non-resident pay capital gains tax on Cyprus company shares?

No. Non-residents pay 0% Cyprus CGT on the disposal of shares in Cyprus companies, provided the company does not derive more than 50% of its value from Cyprus immovable property. There is no withholding tax. No Cyprus tax return is required for non-residents whose only activity is a qualifying share disposal.

How much capital gains tax do I pay when selling a Cyprus property?

CGT is 20% on the net gain after exemptions. First, the purchase cost is adjusted for inflation using the official Cyprus CPI index, which reduces the taxable gain. Then lifetime exemptions apply: EUR 85,430 if the property was your primary residence, or EUR 17,086 for other property (the general personal exemption). Transfers on death and gifts to family members are fully exempt. For many long-held primary residences, the combined indexation adjustment and exemption can reduce the CGT bill to zero or near zero.

Cyprus Capital Gains Tax Exemptions: Complete List for 2026

Personal annual exemption: EUR 17,086

Each individual in Cyprus has a EUR 17,086 lifetime exemption on capital gains from the disposal of immovable property. This applies once in a lifetime and reduces the taxable gain. For example, if you sell a property and realise a gain of EUR 50,000, the first EUR 17,086 is exempt, you only pay CGT on EUR 32,914 (at 20% = EUR 6,583 tax).

Primary residence exemption: EUR 85,430

If you are selling your primary residence (the property you have lived in for at least 5 consecutive years), the first EUR 85,430 of gain is exempt from CGT. This is the most significant exemption and applies to the family home. Note: this exemption and the EUR 17,086 personal exemption can both be applied, giving a combined potential exemption of up to EUR 102,516 on the sale of a primary residence.

Agricultural land exemption: EUR 25,629

Sales of agricultural land qualify for an additional EUR 25,629 exemption.

Other CGT exemptions (complete list):

- Transfers on death (inheritance): exempt

- Gifts between parents and children: exempt

- Gifts between spouses: exempt

- Gifts to charities: exempt

- Transfers related to company reorganisations: exempt under certain conditions

- Disposal of shares NOT in property-owning companies: entirely exempt (Cyprus has no CGT on shares unless the company owns real estate)

- Disposal of securities on the Cyprus Stock Exchange: exempt

- Foreign real estate: gains on property outside Cyprus are NOT subject to Cyprus CGT

What IS subject to CGT in Cyprus:

- Disposal of immovable property located in Cyprus (land, buildings)

- Disposal of shares in companies where more than 50% of the company's value consists of Cyprus immovable property

- Rights related to Cyprus immovable property

CGT rate: 20% flat on the net gain after exemptions and allowable deductions (cost of acquisition, inflation adjustments, improvement costs).

Source: Cyprus Income Tax Law (Cap.297), Cyprus Land Registry and Survey Department, PwC Cyprus Tax Facts 2026.

Free, no commitment

Moving to Cyprus or opening a company?

Tell us your situation and we'll connect you with our specialist expat advisory in Cyprus: Non-Dom tax, company setup and residency, done for you. Free consultation, no commitment.

Related resources

Non-Dom + zero CGT

Non-Dom status adds dividend exemption on top of zero CGT on shares

Crypto capital gains

When crypto gains are CGT-exempt and when the 8% flat rate applies

Crypto tax in depth

8% business income vs 0% CGT — full breakdown for crypto holders

Cyprus vs Germany CGT

Germany taxes share gains at 25% + solidarity — Cyprus charges 0%

Cyprus vs UK CGT

UK CGT on shares: 18–24%. Cyprus: 0%. The difference side by side.

Free newsletter

What do you want to hear about?

No spam. Unsubscribe any time.