Quick Answer

Setting up a Cyprus private limited company (Ltd) takes 5-10 business days and costs approximately EUR 700-1,000 for registration. Annual running costs including accounting and audit average EUR 3,000-3,750. Cyprus companies pay 15% corporate tax, and Non-Dom shareholders pay approximately 2.65% GHS on extracted dividends - making the effective total extraction rate around 17-18%.

Cyprus Company Formation 2026: Complete Guide to Opening a Company in Cyprus

Everything you need to know about Cyprus company formation: costs, timeline, required documents, and how to pay as little as 5% effective tax with a Cyprus Ltd in 2026.

Last updated:

Cyprus Ltd at a Glance

- 15%

- Corporate tax rate on net profits

- €2,100

- Approximate formation cost

- €3,000/year

- Annual maintenance (accounting, VAT, tax)

- 2-4weeks

- Typical incorporation timeline

Key Facts 2026

| Corporate tax rate | 15% flat (since January 2026, up from 12.5%) |

| Setup cost (government fees) | EUR 700-1,000 |

| Total first-year cost (incl. accounting) | EUR 3,000-4,500 |

| Formation timeline | 5-10 business days |

| VAT registration threshold | EUR 15,600 annual turnover |

| Annual levy | EUR 350 |

| Double tax treaties | 65+ countries |

| Dividend withholding tax | 0% to non-resident shareholders |

| Minimum directors | 1 (company can also be single-member) |

Free, no commitment

Moving to Cyprus or opening a company?

Tell us your situation and we'll connect you with our specialist expat advisory in Cyprus: Non-Dom tax, company setup and residency, done for you. Free consultation, no commitment.

Get personalised guidance on Non-Dom status, company formation, and your specific tax situation from an experienced Cyprus tax advisor.

Which Company Structure Should You Choose in Cyprus?

Four company types are available, but the Ltd is the standard choice for most international professionals.

Private Ltd (Recommended)

15% corp tax, limited liability, EU status. The standard for remote workers and freelancers.

Branch Office

Extension of a foreign company. Suitable for large multinationals, not individuals.

Partnership

Two or more persons. No separate legal personality. Less common for tax optimization.

Sole Proprietorship

Simple setup but income taxed at up to 35%. Not recommended for tax efficiency.

Why Is a Ltd Company the Best Option in Cyprus?

For international professionals, remote workers, and freelancers looking to optimize their Cyprus company tax burden, the Private Limited Company offers the best combination of tax efficiency and legal protection:

- 15% corporate tax on profits, compared to up to 35% personal income tax

- Dividends to Non-Dom shareholders taxed at only 2.65% (GHS only, no SDC)

- Salary-plus-dividends is the standard structure for Cyprus Ltd directors

- EU company status enables seamless invoicing to international clients

- Limited liability protects personal assets from business risks

EU Company Benefits

A Cyprus Ltd is a full EU company with access to EU directives, double tax treaties, and VAT reverse-charge for cross-border B2B services.

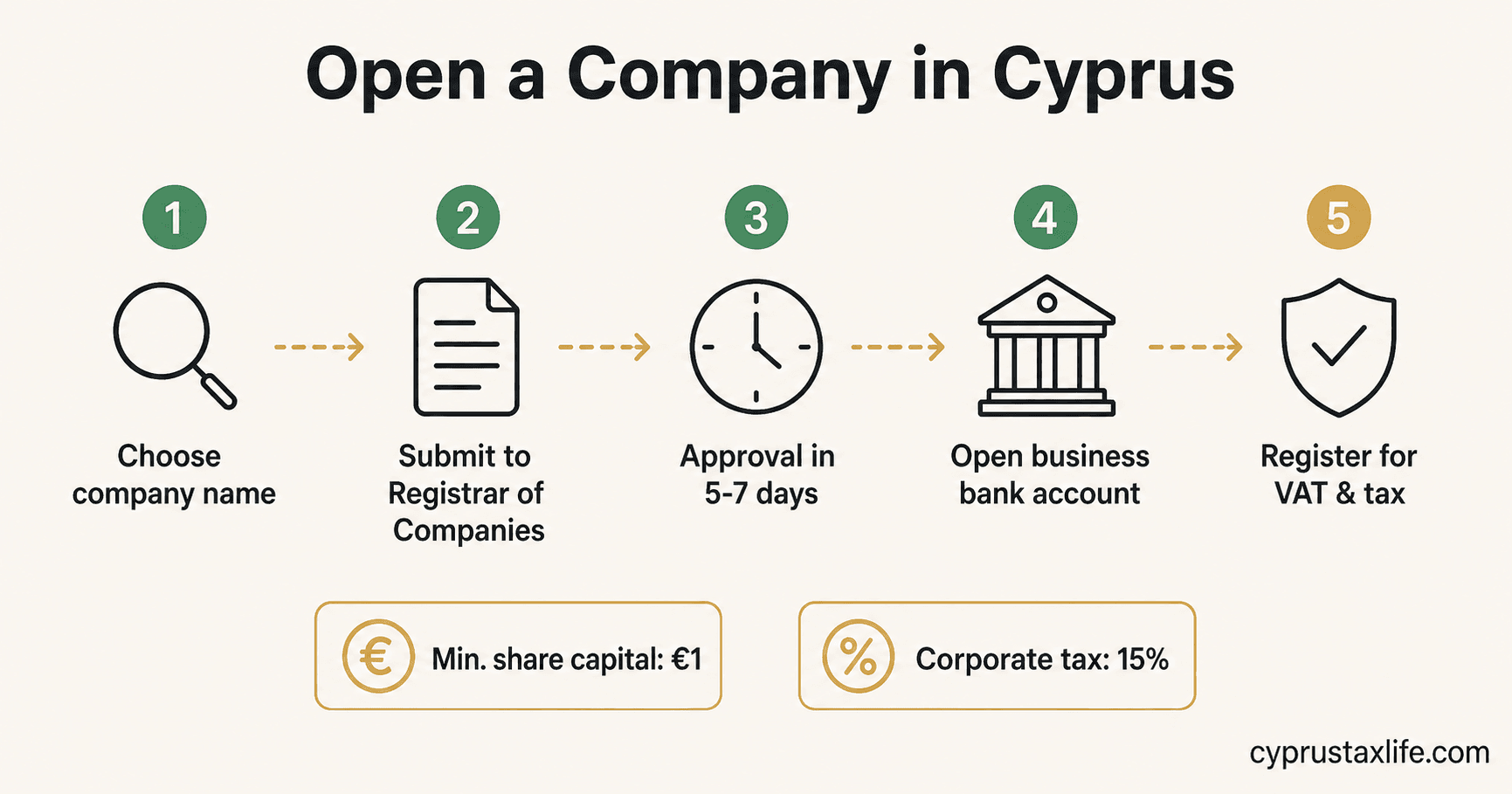

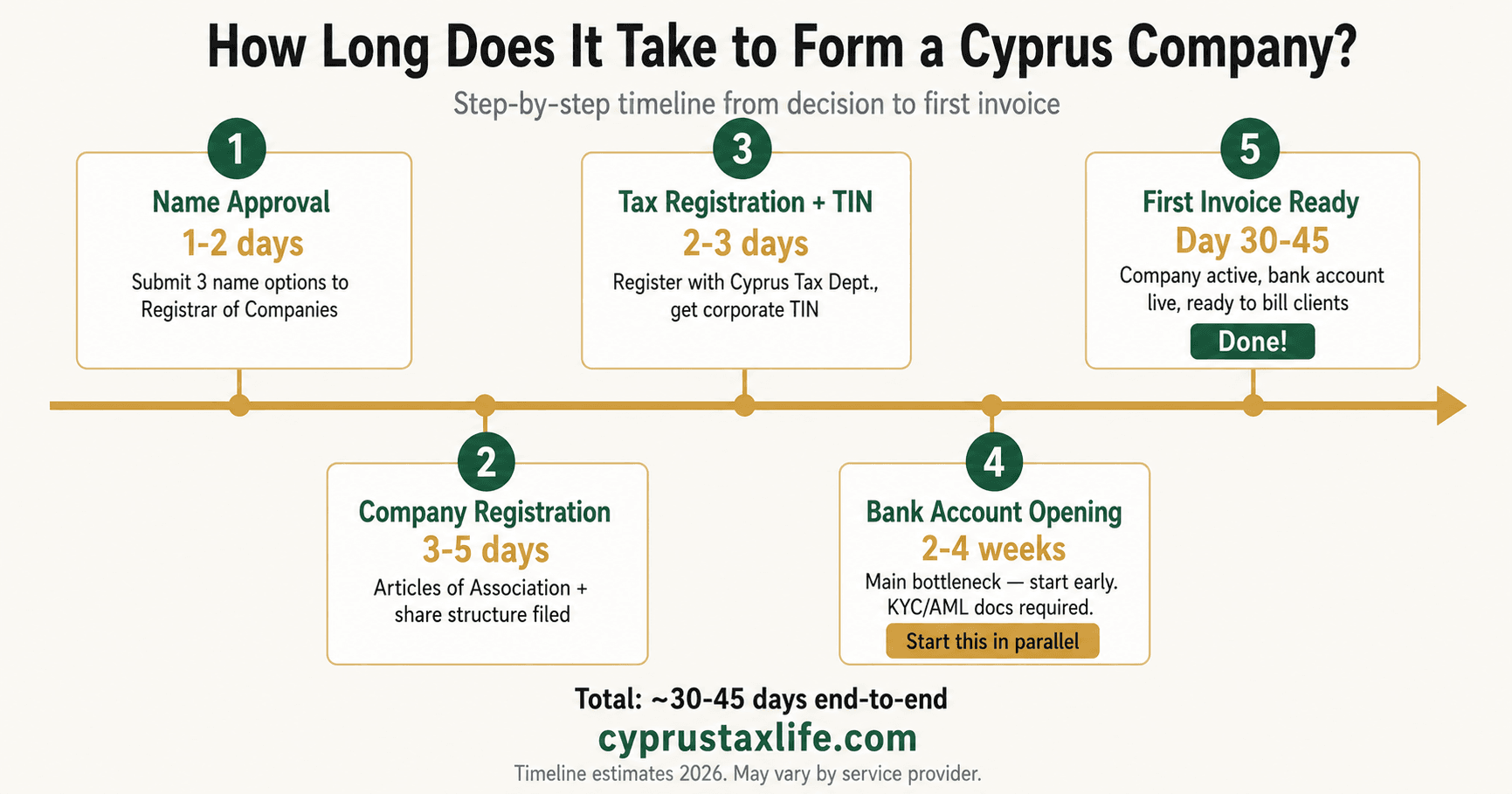

How to Open a Company in Cyprus: Step-by-Step

The full process takes 7 to 15 business days and can be completed entirely remotely.

Name Reservation

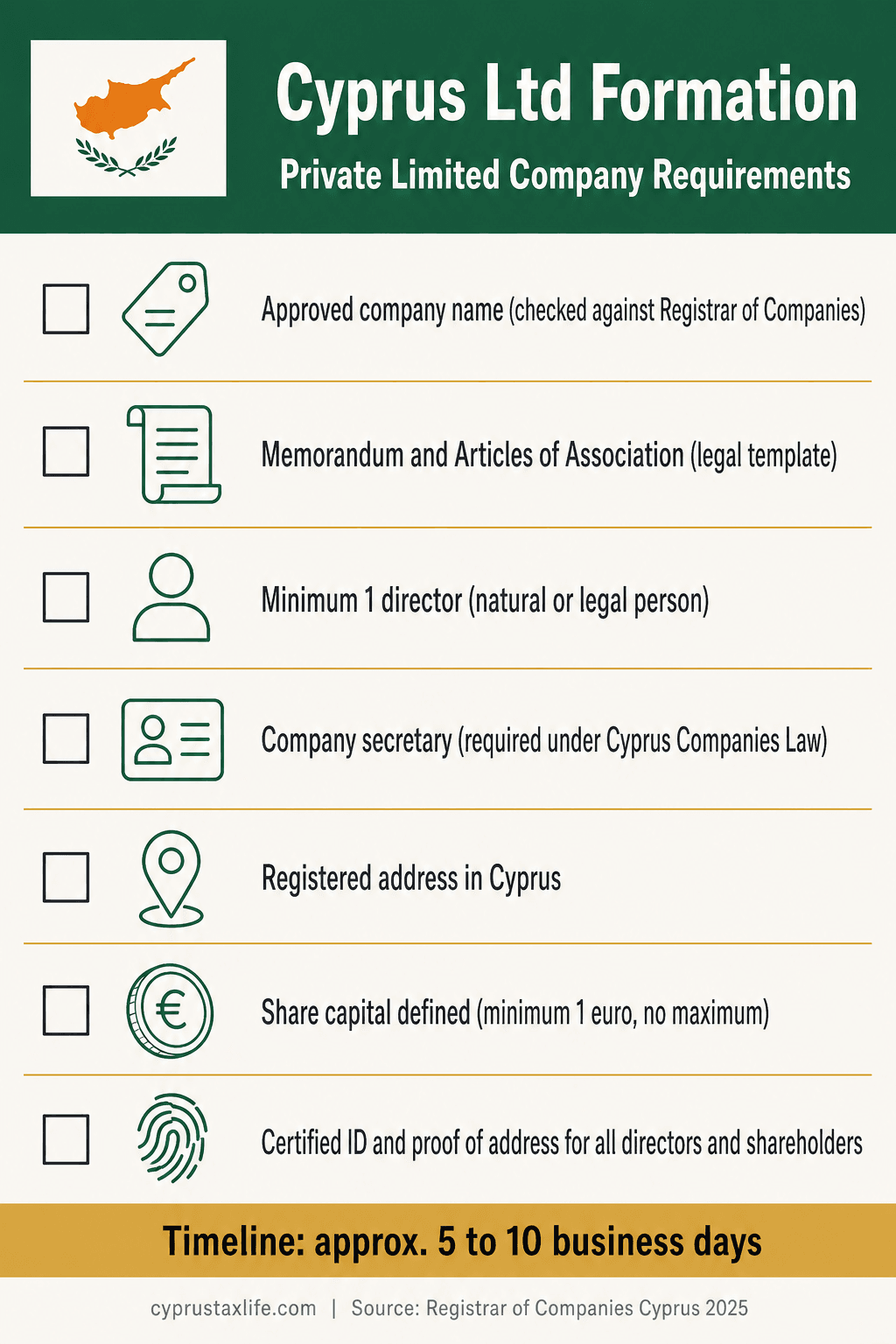

Submit your preferred company name to the Registrar of Companies for approval. The name must be unique and not misleading. Allow 2-5 business days.

Prepare Incorporation Documents

Your advisor prepares the Memorandum and Articles of Association, defining the company's purpose, share structure, and governance rules.

Register with the Registrar

Submit your incorporation application to the Department of Registrar of Companies and Official Receiver (DRCOR) with director, shareholder and Ultimate Beneficial Owner (UBO) details. This is the step people mean when they search "register a company in Cyprus."

- Registrar reviews and approves the Memorandum and Articles of Association

- File the mandatory UBO (beneficial ownership) declaration — required within 90 days of incorporation

- Registrar issues the Certificate of Incorporation, HE1/HE3 certificates and company registration number

- Typical processing time: 5-10 business days for standard filing, 3-5 days for expedited service

Obtain Tax ID (TIC)

Register with the Tax Department for a corporate Tax Identification Code. Required for filing tax returns and invoicing.

VAT Registration

Mandatory for companies providing services to EU or international clients. B2B services to overseas clients are generally zero-rated.

Open Corporate Bank Account

Use a digital bank (Revolut Business) for speed, or a traditional Cyprus bank. Both require the Certificate of Incorporation and director ID.

Our guides cover the essentials, but every situation is different. Professional advisors in Cyprus can help you set up the optimal structure for your specific circumstances.

Have questions about your situation?

Every case is different. Get personalized guidance for your specific tax and relocation needs.

How Much Does It Cost to Form and Maintain a Cyprus Company?

Transparent pricing based on current 2026 figures from Cyprus service providers.

Formation (One-Time): ~2,100 EUR

- Name reservation

- Document preparation (Memorandum & Articles)

- Registrar of Companies fees

- TIC registration

- VAT registration

Annual Maintenance: ~3,000 EUR

- Accounting and bookkeeping

- VAT returns (quarterly)

- Corporate tax return

- Company secretary duties

- Registrar annual levy (350 EUR)

Cyprus Company Formation Costs 2026

All amounts in EUR. Government fees are fixed; advisor fees are market rates.

One-Time Setup Costs

| Item | EUR (approx.) | Notes |

|---|---|---|

| Government registration fee (Registrar) | 440 | Name reservation €10 + incorporation €165 + stamps €265 |

| Memorandum & Articles drafting (lawyer) | 300–600 | M&A preparation and filing by a Cyprus formation agent |

| Notarisation & translation | 100–200 | Required if documents originate outside Cyprus |

| Total setup (one-time) | 840–1,240 | Excludes optional nominee director |

Annual Recurring Costs

| Item | EUR/year | Notes |

|---|---|---|

| Annual government levy (Registrar) | 350 | Mandatory for all Cyprus companies. Due 30 June each year. |

| Accounting & bookkeeping | 1,200–3,600 | Depends on transaction volume and complexity |

| Statutory audit | 1,500–4,000 | Required if turnover >€200k or >25 employees |

| Company secretarial | 200–500 | Annual return filing, register maintenance |

| Annual total (minimum setup, no audit) | 1,750–4,450 | Audit cost added if turnover >€200k |

Optional Costs

| Item | EUR/year | Notes |

|---|---|---|

| Registered office address | 300–600 | Required if you don't have a physical Cyprus office |

| Nominee director | 500–1,500 | Strengthens management & control substance |

| Corporate bank account opening | Free | No fee, but expect 3–8 weeks for full approval |

Includes one-time setup (€840–1,240) + first year annual costs (€1,750–4,450). Excludes optional nominee director and bank account costs.

Source: Cyprus Registrar of Companies fee schedule 2026. Advisor fees based on market rates from Cyprus law firms and accounting practices.

What Is the Best Tax Structure for Remote Workers in Cyprus?

The standard setup for a remote professional or freelancer using a Cyprus Ltd:

- The Ltd invoices clients abroad for consultancy or professional services

- The company pays 15% corporate tax on net profits

- Directors set a modest salary covering Social Insurance and GESY

- Remaining profits distributed as dividends at only 2.65% GHS (Non-Dom)

With this structure and a Cyprus corporate tax rate of 15%, the effective total tax rate on business income is approximately 15%, compared to 40-50% in many Western European countries.

Frequently Asked Questions

How much does company formation in Cyprus cost?

The total cost to form a Cyprus Ltd is approximately EUR 2,100. This includes EUR 600-900 in legal fees for a local formation agent, EUR 105 in Registrar of Companies government fees, and EUR 300-500 for a registered office address for the first year. Annual maintenance (accounting, VAT filing, audit, registered office renewal) typically runs EUR 3,000-6,000 per year depending on company activity.

How long does company formation in Cyprus take?

Incorporation with the Cyprus Registrar of Companies takes 5-10 business days once all documents are submitted. The full process from start to finish — including name reservation, document preparation, registration, Tax ID (TIC), VAT registration, and bank account opening — typically takes 2-4 weeks. Expedited registration is available from the Registrar at an additional fee, reducing incorporation to 3-5 days.

Can a non-resident open a company in Cyprus?

Yes. Non-residents and foreign nationals from any country can form a Cyprus Ltd without living in Cyprus. The entire process can be completed remotely: documents are signed electronically or via notarized power of attorney, and the Registrar accepts remote submissions. The company will need a local registered office address (provided by your formation agent or law firm) and a registered agent. You do not need to be physically present in Cyprus.

What is the minimum share capital for a Cyprus company?

There is no minimum share capital requirement for a Cyprus Private Limited Company (Ltd). EUR 1 is sufficient. Most companies are formed with 1,000 shares at EUR 1 each (total EUR 1,000 nominal share capital) purely as a convention. The absence of a paid-up minimum makes Cyprus formation accessible and straightforward compared to jurisdictions that require EUR 10,000 or more in paid-up capital.

Does a Cyprus company need a registered office in Cyprus?

Yes. All Cyprus companies are legally required to maintain a registered office address in Cyprus where official correspondence, the company register, and statutory records are kept. This does not need to be a physical office where staff work — a registered agent or law firm address is standard and typically costs EUR 300-500 per year. The address must be a real Cyprus address; PO boxes are not accepted by the Registrar.

What is the corporate tax rate for a Cyprus company?

Cyprus companies pay 15% corporate tax on net taxable profits. This applies to profits from trading, services, and most active business income. Dividends received from subsidiaries (where Cyprus holds at least 1% of shares) are exempt from corporate tax under the participation exemption. Qualifying IP income can benefit from the IP Box regime, reducing the effective rate on royalties and licensing to approximately 2.5%. Non-Dom shareholders then pay 2.65% GHS on dividends received — resulting in an effective total rate of approximately 17-18% from gross business profit to net cash in hand.

How do I register a company in Cyprus?

To register a company in Cyprus, you reserve a company name with the Registrar of Companies (2-5 business days), prepare the Memorandum and Articles of Association with a licensed advisor, and submit the incorporation application together with director, shareholder and Ultimate Beneficial Owner (UBO) details. The Registrar of Companies and Official Receiver (DRCOR) issues the Certificate of Incorporation once approved, typically within 5-10 business days of filing. After registration you separately obtain a Tax Identification Code and, if applicable, register for VAT.

What is the Cyprus UBO register and is it mandatory?

The UBO (Ultimate Beneficial Owner) register is a mandatory filing with the Cyprus Registrar of Companies that discloses the individuals who ultimately own or control a company, in line with EU anti-money-laundering rules. Every Cyprus company must submit its UBO declaration within 90 days of incorporation and update it whenever ownership changes. The UBO register is separate from the general Cyprus business/corporate registry entry created at incorporation, and failure to file carries fines for the company and its officers.

Does Cyprus have LLCs or IBCs like other jurisdictions?

No. Cyprus company law does not have an "LLC" or "IBC" entity type — the closest and standard equivalent is the Private Limited Company (Ltd), registered with the Registrar of Companies under the Cyprus Companies Law (Cap. 113). A Cyprus Ltd offers the same limited-liability protection that founders typically look for in an LLC or IBC, plus EU company status, a 12.5%-15% corporate tax rate, and access to Cyprus’s double tax treaty network — benefits an offshore IBC does not provide.

Ready to open your Cyprus company?

We handle registration, business bank account, VAT and Non-Dom setup end to end — done remotely, usually in under a week.

Estimate your total one-off and annual running costs with the Cyprus Company Formation Cost Calculator. To compare whether a Cyprus Ltd saves more tax than operating as a self-employed sole trader, the Company vs Self-Employed Calculator models all three structures side by side.

Frequently Asked Questions

Free, no commitment

Moving to Cyprus or opening a company?

Tell us your situation and we'll connect you with our specialist expat advisory in Cyprus: Non-Dom tax, company setup and residency, done for you. Free consultation, no commitment.

Related resources

Company costs reference

Formation €2k, levy €350, audit costs, all official figures

Real company setup examples

What 5 entrepreneurs actually paid in taxes after forming a Cyprus Ltd

Tax calculator

Model your revenue, salary and expenses — see effective rate

Company FAQ

8 Q&As on corporate tax, formation timelines and costs

Free newsletter

What do you want to hear about?

No spam. Unsubscribe any time.