Quick Answer

Cyprus applies a 15% corporate income tax rate from January 2026 (raised from 12.5% under the OECD Pillar Two reform). Despite the rate increase, Cyprus remains one of the most competitive EU jurisdictions due to the 2.5% IP Box effective rate, 0% withholding tax on outbound dividends, 0% personal CGT on shares, and the Non-Dom regime that limits dividend tax to 2.65% GHS only.

Cyprus Corporate Tax 2026: 15% Rate, IP Box and Five Key Advantages

Cyprus raised its corporate tax from 12.5% to 15% on 1 January 2026 to comply with OECD Pillar Two. The rate increase changes less than it appears: the IP Box, 0% withholding tax on dividends, and Non-Dom personal tax regime remain fully intact.

Last updated:

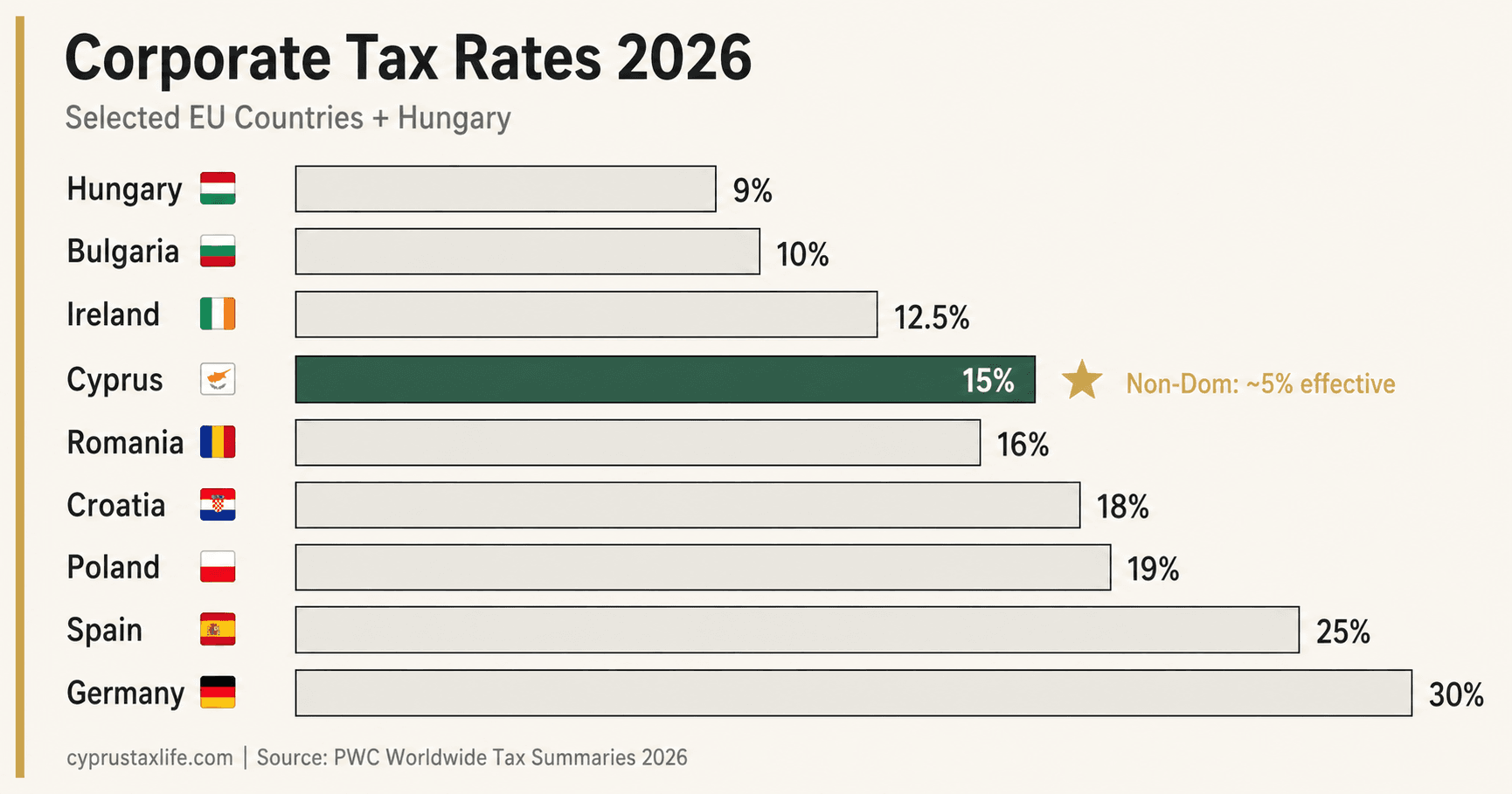

EU Corporate Tax Rates 2026: Where Does Cyprus Rank?

Standard headline corporate income tax rate, lowest to highest. Effective rates vary based on structure and available regimes.

| Country | Corp Tax Rate | Key Notes |

|---|---|---|

| Hungary | 9% | Subject to EU minimum tax (Pillar 2) adjustments for large groups |

| Bulgaria | 10% | Plus 5% dividend withholding tax on distributions |

| Ireland | 12.5% | Trade income only; passive and non-trading income taxed at 25% |

| Cyprus | 15% | 0% dividend withholding; IP Box at 2.5% effective; 65+ tax treaties |

| Lithuania | 15% | Small businesses (income <EUR 300k): 5% |

| Romania | 16% | Micro-entity rate: 1% (under EUR 500k turnover) |

| Latvia | 20% | Paid only on distributed profits (similar to Estonia) |

| Estonia | 20% | 0% on retained profits; 20% on distributions |

| Poland | 19% | Small businesses: 9% |

| Netherlands | 19-25.8% | Tiered; participation exemption available |

| Spain | 25% | New businesses: 15% for first 2 profitable years |

| France | 25% | Reduced from 33.33% progressively since 2018 |

| Germany | ~29-33% | Corp tax + solidarity surcharge + trade tax (Gewerbesteuer) |

Sources: KPMG Corporate Tax Rate Survey 2025, European Commission taxation database. Rates as of 2026. Large multinational groups (>EUR 750M revenue) subject to OECD Pillar 2 global minimum tax of 15%.

Key Facts 2026

| Corporate tax rate (from 1 Jan 2026) | 15% |

| Previous rate (until 31 Dec 2025) | 12.5% |

| Reason for change | OECD Pillar Two global minimum tax (GloBE) implementation |

| IP Box effective rate | ~2.5% on qualifying IP income (80% profit exemption) |

| Dividend withholding tax (non-residents) | 0% |

| Capital gains on share disposal | 0% |

| Advance tax instalments | Two equal instalments (August and December of tax year) |

| Corporate tax return deadline | 31 March of the following year |

| Annual company levy | EUR 350 |

| Compared to EU average | EU average ~21.3% - Cyprus remains among lowest in EU |

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Get personalised guidance on Non-Dom status, company formation, and your specific tax situation from an experienced Cyprus tax advisor.

Cyprus Corporate Tax vs EU Countries (2026)

| Country | Corp tax rate | Effective on dividends (resident) | WHT on outbound dividends | CGT on shares (personal) |

|---|---|---|---|---|

| Cyprus (Non-Dom) | 15% | 2.65% GHS only | 0% | 0% |

| Ireland | 12.5% | ~33% (PRSI + USC) | 25% | 33% |

| Bulgaria | 10% | ~15% (WHT on divs) | 5% | 10% |

| Estonia | 0% (retained) / 22% on distribution | 22% at distribution | 7% | 20% |

| Malta | 35% (6/7 refund = 5% effective) | 5% after refund | 0% (EU residents) | 0% |

| Germany | ~30% (corp + trade tax) | 26.4% (Abgeltungsteuer) | 25% | 26.4% |

| France | 25% | 30% (PFU flat tax) | 25% | 30% |

| Spain | 25% | 19-28% progressive | 19% | 19-28% |

| United Kingdom | 25% | 33.75-39.35% (higher/add rate) | 0% (UK-EU treaties) | 18-24% |

WHT = withholding tax. Effective rates are indicative and depend on tax residency, treaties and structure. Cyprus Non-Dom figures assume dividend distribution to Non-Dom shareholder (0% SDC, 2.65% GHS only).

IP Box: EUR 100,000 in royalty income - tax comparison

| Country | Royalty income | Taxable amount | Tax paid | Effective rate |

|---|---|---|---|---|

| Cyprus (IP Box - 15%) | EUR 100,000 | EUR 16,667 (80% exempt) | EUR 2,500 | 2.5% |

| Netherlands (Innovation Box - 9%) | EUR 100,000 | EUR 100,000 | EUR 9,000 | 9.0% |

| Ireland (KDB - 10%) | EUR 100,000 | EUR 100,000 | EUR 10,000 | 10.0% |

| United Kingdom (Patent Box - 10%) | EUR 100,000 | EUR 100,000 | EUR 10,000 | 10.0% |

| Germany (standard 30%) | EUR 100,000 | EUR 100,000 | EUR 30,000 | 30.0% |

| Spain (standard 25%) | EUR 100,000 | EUR 100,000 | EUR 25,000 | 25.0% |

Cyprus IP Box uses the nexus approach (OECD BEPS Action 5 compliant). 80% of qualifying IP income is deducted from taxable income, leaving 20% taxable at 15% = 3% gross effective rate, or 2.5% after the standard 80% deduction on the net profit.

Which structure makes sense at each income level?

| Annual revenue / profit | Recommended structure | Reason |

|---|---|---|

| Below EUR 30,000 | Self-employed in Cyprus | Below the income tax threshold (EUR 19,500 allowance). Company overhead (EUR 3,500-6,000/year accounting + audit) exceeds the tax saving. |

| EUR 30,000 - 80,000 | Cyprus Ltd + Non-Dom | 15% corporate tax + 2.65% GHS on dividends = ~17% effective. Versus 16.6% SI + 4.7% GHS + income tax for self-employed. Cyprus Ltd clearly wins above EUR 50K. |

| EUR 80,000 - 300,000 | Cyprus Ltd + Non-Dom + low salary | Optimise salary below EUR 19,500 (0% income tax), distribute remainder as dividends. Use NID if funded by equity contribution. Effective rate 14-17%. |

| EUR 300,000+ | Cyprus HoldCo + OpCo structure | Holding company in Cyprus receives dividends from operating subsidiaries tax-free. IP Box if applicable (software, patents, trademarks). NID on equity injections. Effective rate under 10%. |

| IP/royalty income (any level) | Cyprus Ltd + IP Box | 2.5% effective tax rate on qualifying royalties. Software, patents, trademarks, designs all qualify if developed by the Cyprus entity. Setup requires demonstrable R&D substance in Cyprus. |

Frequently Asked Questions

What is the Cyprus corporate tax rate in 2026?

Does the Cyprus IP Box still work at 15%?

Is there withholding tax on dividends paid by a Cyprus company?

What is the effective total tax rate for a Cyprus Ltd owner under Non-Dom?

Who qualifies for the Cyprus Non-Dom dividend exemption?

What is the Notional Interest Deduction (NID) in Cyprus?

Can a non-resident own a Cyprus company?

How does Cyprus compare to Ireland for company structure?

How can a Cyprus company optimize its corporate tax?

What are the economic substance requirements for a Cyprus company?

What is the effective corporate tax rate for tech companies in Cyprus?

How does a solo founder optimize corporate tax with a Cyprus company?

Cyprus Corporate Tax Calendar: Deadlines and Filing Requirements

Meeting Cyprus tax deadlines is essential to avoid penalties and interest. All Cyprus-resident companies must comply with the following annual filing cycle.

Annual Filing Deadlines

31 March - Submission of provisional tax return (1st installment). Provisional tax is based on your estimated profit for the current tax year.

30 June - Second provisional tax installment (50% of estimated annual tax).

31 July (extended) - Electronic filing of the tax return for the PREVIOUS year via the TaxisNet portal.

31 December - Third and final provisional tax installment, or revision of provisional tax estimate.

Within 9 months of year end - Company annual return to the Registrar of Companies. For December year-end companies, this is 31 December.

Penalties for Late Filing

- EUR 100 flat penalty for late submission

- Interest at 1.75% per month on any unpaid tax

- Companies with annual turnover exceeding EUR 70,000 must submit audited financial statements

- Cyprus Tax Department has significantly increased enforcement since 2022 - voluntary compliance is strongly recommended

Underestimation Penalty

If your provisional tax estimate falls more than 25% below the actual tax liability for the year, a 10% surcharge applies on the difference. This makes accurate forecasting critical, particularly for growing companies.

Deductible vs Non-Deductible Expenses: The Complete Guide

Understanding which expenses reduce your taxable profit is one of the most practical aspects of Cyprus corporate tax planning. Cyprus follows a system where only expenses incurred wholly and exclusively for business purposes are deductible.

Fully Deductible Expenses (100%)

- Salaries, wages, and employer social insurance contributions

- Office rent and utilities directly related to business operations

- Professional fees - accountant, lawyer, and mandatory auditor

- Business travel (flights, hotels for legitimate business trips with documentation)

- Marketing and advertising (Google Ads, website costs, social media campaigns)

- Software subscriptions (SaaS tools used for business purposes)

- Bank charges and interest on business loans

- Depreciation and wear and tear allowances (see rates below)

- Bad debts written off, with documentation showing active pursuit of recovery

- Research and development expenditure (100% deduction, plus potential IP Box benefits)

Partially Deductible Expenses

- Business entertainment (client lunches, dinners): 50% deductible. Keep receipts and record the business purpose

- Motor vehicles: Capital allowances only on commercial vehicles. Private passenger cars are not deductible

- Home office: A proportional share of rent and utilities is deductible based on the space dedicated exclusively to business

Non-Deductible Expenses

- Owner drawings - if you pay yourself informally. Must be structured as director's fees through payroll

- Fines and penalties of any kind

- Non-business entertainment and personal expenses passed through the company

- Charitable donations (unless made to Cyprus Tax Department-approved charities)

- Provisions for anticipated losses - only actual realized losses are deductible

- Capital expenditure (must be depreciated over time, not expensed immediately)

Notional Interest Deduction (NID)

NID is a powerful and often underused tool. Cyprus allows companies to deduct a notional interest charge on new equity capital invested in the company - whether through fresh capital contributions or reinvested retained earnings.

The NID rate equals the 10-year Cyprus government bond yield plus 5 percentage points, which in 2026 approximates 8-10% annually. This effectively creates a deduction for the cost of equity financing, making Cyprus especially attractive for holding companies and IP-holding structures.

Example: EUR 100,000 of new equity injected into a Cyprus Ltd. NID deduction at 9% = EUR 9,000 per year. Tax saving: EUR 9,000 x 15% = EUR 1,350 annually, with no cash outflow.

Wear and Tear Allowances (Depreciation Rates)

Cyprus uses a straight-line depreciation system for capital assets, referred to locally as "wear and tear" (apomosis). Capital expenditure cannot be expensed immediately but is deducted over the asset's useful life at statutory rates. Below are the current rates for the most common asset types.

Practical Example

EUR 6,000 MacBook Pro purchased in Year 1. At 33% annual depreciation = EUR 2,000 deduction per year. Fully written off by Year 3. Total tax saving over 3 years: EUR 6,000 x 15% = EUR 900.

Note: Cyprus does not have a formal super deduction mechanism, but certain approved capital expenditure in technology and renewable energy sectors may qualify for enhanced rates. A Cyprus tax advisor can confirm the applicable rate for specific equipment.

Loss Carryforward and Group Relief

Cyprus offers one of the most flexible loss utilization regimes in the EU, with no time limit on carrying forward losses and an efficient group relief system.

Individual Company Loss Carryforward

- Tax losses can be carried forward indefinitely against future taxable profits - no expiry date

- Unlike Germany (which caps loss offset at 60% of profit per year), Cyprus imposes no such restriction

- Losses cannot be carried back to prior tax years

- Important: if a company changes ownership by more than 50%, and the business also changes character, the right to use prior losses may be restricted

Capital Allowance Losses

- Unrelieved capital allowances (unused depreciation) are also carried forward indefinitely

- If depreciation allowances exceed profit in a given year, the excess becomes a capital allowance loss to offset in future years

Group Loss Relief

- Losses can be surrendered between group companies if both are Cyprus-resident

- Minimum 75% common ownership required (direct or indirect)

- Surrendering company must have made a loss in the same tax year the claimant made a profit

- Must be claimed by including the transfer in both companies' tax returns for that year

Group Relief Example

Company A (holding company, Cyprus Ltd) makes a loss of EUR 50,000 in Year 1. Company B (100% operating subsidiary of A, Cyprus Ltd) makes a profit of EUR 200,000 in Year 1.

With group relief, Company B can claim the EUR 50,000 loss from A, reducing its taxable profit to EUR 150,000.

Tax without group relief: EUR 200,000 x 15% = EUR 30,000.

Tax with group relief: EUR 150,000 x 15% = EUR 22,500. Saving: EUR 7,500.

This planning opportunity is particularly relevant for founders operating multiple Cyprus entities, such as a holding company owning IP and an operating company generating revenue.

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Free newsletter

What do you want to hear about?

No spam. Unsubscribe any time.