International Tax Planning: The Legal Framework for Paying Less

Cyprus combines Non-Dom status, 0% CGT, 15% corporate tax, and 65+ tax treaties into the most complete international tax planning base in the EU.

Last updated:

International tax planning is the process of structuring personal income, business operations, and investments across multiple jurisdictions to reduce the total tax burden legally. It covers residency decisions, corporate structuring, income classification, treaty usage, and the timing of capital events.

For entrepreneurs, investors, and high-income professionals with location flexibility, international tax planning can reduce effective tax rates from 40-55% in most Western European countries to single digits - while remaining fully compliant with EU law, OECD standards, and bilateral tax treaties.

The Four Pillars of International Tax Planning

1. Tax Residency and Personal Domicile

Tax residency determines which country has primary taxing rights over your worldwide income. Most countries use a 183-day rule: spend more than 183 days in a country per calendar year and you become a tax resident. Some countries (like Cyprus) offer a 60-day fast-track. Others (like the US) apply citizenship-based taxation regardless of where you live.

Within residency, domicile is a secondary concept that determines which assets and income streams are subject to local tax. Non-Domiciled (Non-Dom) status in countries like Cyprus, Malta, and Ireland exempts foreign-sourced income from domestic income tax - a critical tool for those with income from offshore sources.

How Cyprus tax residency works: Cyprus Tax Residency Guide.

2. Corporate Structure and Jurisdiction

Where you incorporate your company determines: (a) the corporate tax rate on profits; (b) withholding taxes on dividends paid to shareholders; (c) access to tax treaties with other countries; (d) whether dividend income qualifies for Non-Dom exemption. Cyprus combines a 15% corporate rate, 0% withholding on outbound dividends, 0% CGT on share disposals, and 60+ tax treaties - making it one of the most efficient corporate jurisdictions in the EU.

Cyprus company setup and corporate tax: Cyprus Company Formation Guide.

3. Investment Income Treatment

How dividends, interest, royalties, and capital gains are taxed varies significantly across jurisdictions. In Germany, dividend income is taxed at 25% (Abgeltungsteuer). In France, at 30% (flat tax). In Cyprus, for a Non-Dom resident, dividend income is subject to 0% income tax and only the 2.65% GHS health contribution - capped at €4,770 per year regardless of dividend size. Capital gains on securities (shares, bonds) are exempt from CGT in Cyprus entirely.

Non-Dom framework and dividend treatment: Cyprus Non-Domicile Status.

4. Treaty Networks and Exit Planning

Double Tax Treaties (DTTs) prevent income from being taxed twice - once in the source country and once in the residence country. Cyprus has DTTs with 65+ countries, including most EU members, UK, US, India, Russia, and UAE. These treaties reduce withholding tax on dividends, interest, and royalties flowing between treaty partners - often to 0-5%.

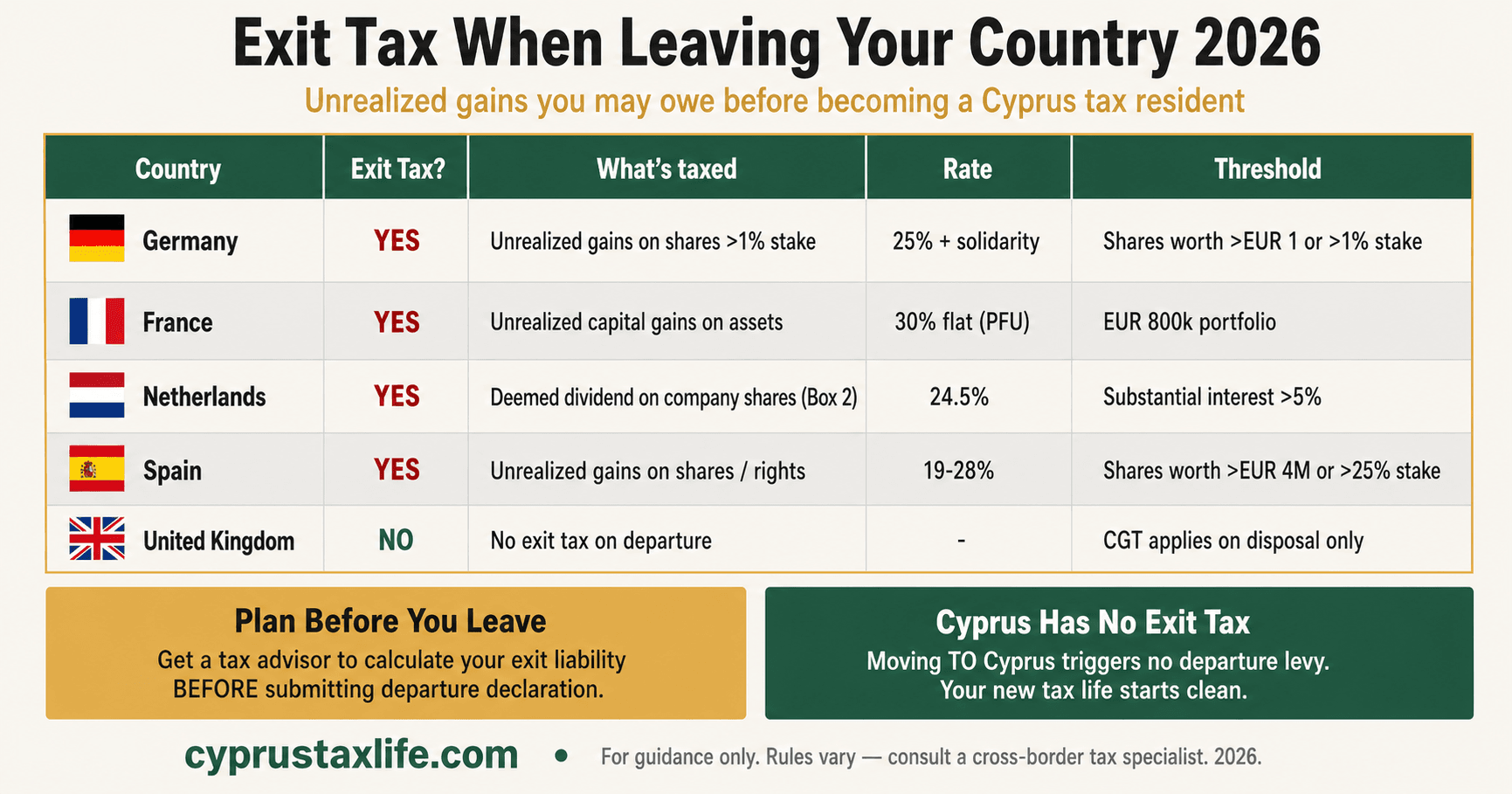

Exit planning refers to the strategy of establishing new tax residency before a large capital gain event (business sale, IPO, equity vesting). Most high-tax countries impose an exit tax on unrealised gains when you depart. Planning the sequence and timing correctly is critical to avoiding double taxation.

Cyprus treaty network: Cyprus Double Tax Treaties.

EU vs. Global Approach: Which Makes Sense

| Factor | EU-Based (Cyprus) | Non-EU (UAE, Bahamas) |

|---|---|---|

| EU passport / Schengen access | Yes - full EU rights | No |

| Tax on foreign dividends | 2.65% GHS (Non-Dom) | 0% |

| Corporate tax rate | 15% | 0-9% |

| Capital gains (securities) | 0% | 0% |

| Legal certainty and stability | High (EU framework) | Variable |

| Banking and business access | Full EU banking | Restrictions in some cases |

| OECD / FATF compliance | Full | Improving but historically complex |

| Residency requirements | 183 days or 60-day rule | Usually 0-90 days |

For entrepreneurs who need EU residency, Schengen freedom, stable banking, and EU-compliant corporate structures, Cyprus offers the most tax-efficient combination within the EU. The UAE is more competitive on pure tax rate, but requires genuine relocation and does not provide EU access.

Cyprus as a Base for International Tax Planning

Cyprus combines all four pillars of international tax planning in a single jurisdiction. The framework works as follows:

1. Personal residency: establish Cyprus tax residency via 183-day rule or 60 Day Rule. Confirm Non-Dom status (automatic for non-domiciled individuals).

2. Corporate structure: incorporate a Cyprus limited company. Use as operating company, holding company, or IP holding vehicle depending on income type.

3. Income structuring: pay minimal salary (if desired for social insurance); distribute profits as dividends at 2.65% GHS. For IP income, apply for IP Box regime at 2.5% effective corporate rate.

4. Treaty positioning: use Cyprus DTT network to reduce withholding at source on income received from other countries. For business exits, ensure Cyprus is the registered shareholder of shares being sold.

Holding structures: Cyprus Holding Company.

IP income optimisation: Cyprus IP Box Regime.

Common Mistakes in International Tax Planning

Not breaking home-country tax residency properly

Establishing a new tax residency is not sufficient on its own. Most high-tax countries have rules that maintain tax residency if you retain a home, family centre of life, or economic ties. Failing to break the prior residency cleanly results in dual taxation. A formal tax residency certificate from Cyprus and a certificate of departure from the home country are typically required.

Ignoring exit tax on departure

Germany, France, Spain, and the Netherlands all impose exit taxes on unrealised capital gains when a resident departs. For entrepreneurs with significant equity value, this tax event on departure can be substantial. Planning the timing - and in some cases using instalment payment arrangements - is critical. Exit tax rules vary significantly by country and asset type.

Using Non-Dom structure for employment income

Non-Dom status exempts passive foreign income (dividends, interest) from tax. It does not exempt employment income earned in Cyprus. An entrepreneur who pays themselves a salary from their Cyprus company will still be subject to Cyprus income tax on that salary at progressive rates (0% up to €22,000, then 20-35%). The optimised structure involves minimal salary and dividend-based distributions.

Underestimating substance requirements

Post-BEPS (Base Erosion and Profit Shifting) rules require genuine economic substance in the jurisdiction where profits are taxed. A Cyprus company that has no real operations, no employees, and no decision-making in Cyprus may be challenged by tax authorities in other jurisdictions as an artificial arrangement. Substance is not just paperwork: it means actual directors, real business activity, and genuine management in Cyprus.

What is the most tax-efficient country in the EU for international tax planning?

Cyprus is consistently ranked as the most tax-efficient EU country for entrepreneurs, investors, and high earners. It combines 15% corporate tax, 0% CGT on securities, 0% withholding on outbound dividends, Non-Dom status for foreign dividend exemption, and a network of 65+ double tax treaties. The effective tax rate for a Non-Dom receiving dividends from a Cyprus company is approximately 2.65%.

How does international tax planning differ from tax evasion?

Tax planning uses legal structures, treaty provisions, and legitimate residency changes to reduce tax liability within the law. Tax evasion involves concealing income or assets from tax authorities - which is illegal. All strategies described in this guide are based on disclosed, legal structures recognised by EU law, OECD guidelines, and bilateral tax treaties. The key distinction is transparency: legal structures are disclosed to relevant tax authorities.

How long does it take to set up international tax planning through Cyprus?

The full setup typically takes 4-10 weeks. Company formation in Cyprus takes 5-10 business days. Obtaining a Tax Identification Number and registering for VAT takes 2-4 weeks. Yellow Slip (EU citizen registration) or residence permit (non-EU) takes 2-6 weeks. The Non-Dom tax residency certificate is issued by the Tax Department after the first year of residence is confirmed. Most structures are operational within 2-3 months of initiating the process.

Do I need to live in Cyprus full time for international tax planning?

No. The 60 Day Rule allows Cyprus tax residency with just 60 days per year, provided you have no other tax residency, maintain a permanent home in Cyprus, and have a business, employment, or directorship connection. Standard tax residency requires 183 days per year. Many entrepreneurs use Cyprus as their primary tax base while spending time across multiple countries.

Is Cyprus an EU-blacklisted tax haven?

No. Cyprus is an EU member state and is not on the EU list of non-cooperative jurisdictions for tax purposes. It meets OECD BEPS standards, exchanges tax information automatically under CRS (Common Reporting Standard), and complies with EU anti-tax avoidance directives (ATAD I and II). Its low tax rates are legal under EU state aid rules and treaty law.

What professional advisers are needed for international tax planning?

Typically: a Cyprus-qualified tax adviser (for local tax registration, Non-Dom application, and annual filings); a corporate lawyer (for company formation and shareholder agreements); and a home-country tax adviser (for exit tax analysis and residency break). For complex structures involving multiple jurisdictions, an international tax specialist with knowledge of both Cyprus and the originating jurisdiction is advisable.

Does Pillar Two (the 15% global minimum tax) affect my Cyprus holding company?

Almost certainly not, unless your consolidated group revenue exceeds EUR 750 million. Pillar Two targets large multinationals only, that threshold excludes the vast majority of entrepreneurs, investors, and SME groups using Cyprus structures. If your group is below EUR 750 million in annual consolidated revenue, your Cyprus corporate tax rate, IP Box benefits, and Non-Dom dividend path are completely unaffected by Pillar Two. For the rare larger group that does cross the threshold, Cyprus's Qualified Domestic Minimum Top-Up Tax (QDMTT) collects any top-up tax in Cyprus itself, preventing a foreign jurisdiction from claiming it under the UTPR backstop.

Can my home country (Germany, UK, Spain) tax my Cyprus company's profits even if I've moved to Cyprus?

Controlled Foreign Corporation (CFC) rules give your home country the right to attribute a Cyprus company's low-taxed passive income to you as a resident, but only if you are still tax-resident there. If you have genuinely moved to Cyprus and broken your home-country tax residence, CFC rules in your former country cannot reach you or your Cyprus company. The risk arises when founders maintain home-country residency while owning a Cyprus company, or when they return within the anti-avoidance windows (e.g., the UK's five-year temporary non-residence rule). Even for home-country residents who retain shares in a Cyprus company, adequate economic substance in Cyprus, real management, local decision-making, provides a safe harbour under most CFC regimes including Germany's AStG and the UK's Part 9A TIOPA.

What exit taxes do I need to plan for before moving to Cyprus?

Exit taxes vary significantly by country and are one of the most overlooked costs in relocation planning. Germany imposes a deemed disposal tax (Wegzugsteuer under §6 AStG) on shares held at over 1% in any corporation when a German tax resident emigrates, the unrealised gain is taxed as income in the year of departure. The UK taxes gains on assets disposed of within five years of departure if the individual returns to the UK (temporary non-residence rules). France and Spain have similar exit tax regimes on significant shareholdings. Exit tax must be modelled before restructuring, not after, the tax saving in Cyprus may take several years to offset a large exit tax bill. A qualified cross-border tax adviser should calculate the net present value of the move accounting for exit costs before you commit.

How does the Cyprus Non-Dom regime compare to Estonia's distributed profit model for a founder taking dividends?

Estonia's OÜ structure defers corporate tax (20%) until profits are distributed, it is a deferral mechanism, not an exemption. The moment you pay yourself a dividend from an Estonian company, 20% corporate tax applies, plus personal income tax in your country of residence. A Cyprus Non-Dom structure taxes corporate profit at 15% and then applies 0% income tax plus 2.65% GHS on dividends, for a total effective rate of approximately 17-18% through the full chain, with no deferral risk and no catch-up tax on distribution. Estonia is advantageous primarily for founders who reinvest heavily and delay distributions for years. For founders taking regular income from their company, Cyprus delivers a lower effective rate with more structural certainty.

What is the minimum real presence required to make a Cyprus structure tax-legitimate?

There is no single prescribed minimum, but the standard used by tax authorities and courts combines several factors: at least one Cyprus-resident director with relevant expertise and genuine authority to make decisions; board meetings physically held in Cyprus (not by phone from another country) with contemporaneous minutes; key contracts signed in Cyprus; local bank accounts operated by Cyprus-based signatories; and some form of local office or co-working presence. For an IP Box claim, the nexus approach additionally requires that qualifying R&D expenditure is incurred in Cyprus. As a practical floor for a holding company, budget EUR 30,000-60,000 per year for a resident director service, registered office, accounting, and audit, this is the cost of legitimate substance. A structure that costs less than this is almost certainly cutting corners that will not survive scrutiny.

This guide provides general information on international tax planning frameworks and is not legal or tax advice. International tax law is complex and jurisdiction-specific. Consult a qualified Cyprus tax specialist before implementing any structure.

Cyprus as an International Tax Planning Hub

Cyprus offers a combination of features that few other EU jurisdictions can match: 15% corporate tax, 0% withholding on outbound dividends, interest, and royalties to treaty partners, a participation exemption on subsidiary dividends, a 2.5% IP Box regime, and the Non-Dom framework giving shareholders a ~5% effective total rate on distributed profits. The result is a legal structure that competes with traditional low-tax holding locations while offering full EU treaty access.

1. IP Holding and the IP Box Regime

The Cyprus IP Box gives an 80% notional deduction on qualifying IP income, reducing the effective corporate tax rate on royalties and licensing income to 2.5%. Qualifying assets include patents, copyrights in software, and other IP that has been developed or substantially improved in Cyprus. The IP must meet the modified nexus approach under OECD BEPS Action 5, the Cyprus company must have incurred qualifying R&D expenditure relative to the income claimed under the IP Box. Combined with 0% withholding on royalties paid to Cyprus under most DTAs, this is a competitive structure for technology IP.

2. Dividend Pipeline and the Participation Exemption

A Cyprus holding company receiving dividends from subsidiaries in which it holds at least 1% of share capital benefits from a full participation exemption, the dividends are exempt from Cyprus corporate tax (subject to anti-avoidance rules that exclude passive holding structures if the subsidiary pays less than 6.25% effective tax in its home country). The exempt dividend can then be distributed to a Non-Dom resident shareholder at only 2.65% GHS, resulting in a total effective rate of approximately 17-18% from gross operating profit at the subsidiary to net cash in the shareholder's hands.

3. Cyprus as a Treaty Conduit

With 65+ double tax agreements, Cyprus provides reduced withholding rates on income flows from many countries. The UK-Cyprus DTA provides 0-15% WHT on dividends. The Israel-Cyprus DTA provides 5% on dividends. The UAE-Cyprus treaty and Singapore-Cyprus treaty are useful for structuring income flows from the Gulf and Asia-Pacific. A Cyprus holding company in the chain can reduce source-country withholding to DTA rates, provided the Cyprus company has genuine substance (physical office, local director, real decision-making authority).

4. Substance Requirements, What BEPS Changed

Post-BEPS, Cyprus structures must have real economic substance. The Cyprus tax authorities apply the management and control test: where are board meetings held, where do directors actually reside and exercise judgment, does the company have its own staff and office? Nominee director arrangements where decisions are actually made elsewhere will not satisfy the substance test and risk the company being treated as tax resident in the shareholder's home country instead. The minimum substance package for a Cyprus holding company typically includes: a local bank account, a registered office with real use, at least one local non-executive director with decision-making involvement in board meetings held in Cyprus, and local bookkeeping.

5. The Non-Dom + Holding Company Structure

The most common structure for relocating entrepreneurs: a Cyprus Ltd (15% CIT) owned by a Non-Dom Cyprus tax resident individual (0% SDC on dividends + 2.65% GHS). Effective total rate from gross profit to net cash: approximately 17-18%. Compared to a UK Ltd owned by a UK resident: 25% CIT + 39.35% dividend tax on higher-rate taxpayers = ~54% effective total rate. The structure is fully legal and widely used by EU nationals who have established genuine Cyprus tax residency. The key compliance obligation is ensuring genuine substance in both the company and the individual's personal residency.

BEPS 2.0 and Pillar Two: What the 15% Global Minimum Tax Means for Cyprus Structures

Pillar Two, the OECD's Global Minimum Tax framework, establishes a 15% effective tax rate floor for Multinational Enterprises (MNEs) with consolidated global revenues exceeding EUR 750 million. Cyprus transposed the EU Minimum Tax Directive into domestic law, introducing both an Income Inclusion Rule (IIR) and a Qualified Domestic Minimum Top-Up Tax (QDMTT). For any Cyprus group entity that is part of a qualifying MNE, the QDMTT ensures that the top-up tax is collected in Cyprus rather than in the parent jurisdiction, preserving Cyprus's tax sovereignty even within the Pillar Two framework.

The vast majority of entrepreneurs, freelancers, and SMEs structuring through Cyprus are entirely unaffected by Pillar Two. The EUR 750 million revenue threshold excludes virtually all private holding structures, consulting companies, and even mid-sized operating groups. If your consolidated group revenue is below this threshold, Pillar Two has no bearing on your Cyprus corporate tax rate, your dividend pipeline, or your Non-Dom status, the 12.5% (now 15%) corporate rate and the effective ~5% dividend path remain intact for your structure.

For larger groups that do cross the threshold, the QDMTT mechanism is actually a feature rather than a bug. Because Cyprus collects the top-up tax domestically, the parent company's jurisdiction cannot apply a secondary top-up under the Undertaxed Profits Rule (UTPR). Groups with genuine operational substance in Cyprus, staff, management, real decision-making, can rely on the substance-based income exclusion (SBIE), which carves out a portion of profits based on payroll costs (10% phase-in) and tangible assets (8% phase-in), reducing the effective top-up exposure significantly.

The IP Box regime warrants specific attention under Pillar Two. An effective tax rate of 3%, the result of the 80% income exemption applied to a 15% base, falls below the 15% global minimum for qualifying MNEs. For groups above the EUR 750 million threshold using the IP Box, a top-up tax brings the effective rate to 15% on those IP profits. Below the threshold, the IP Box remains a fully effective planning tool with no Pillar Two interference. Cyprus has been proactive in its legislative response, so the domestic QDMTT infrastructure is in place and the legal certainty for structures is high.

CFC Rules: When Your Home Country Taxes Your Cyprus Company Anyway

Controlled Foreign Corporation (CFC) rules are the single most underappreciated risk in international tax planning. Germany's CFC regime under §§7-14 Außensteuergesetz (AStG) attributes low-taxed passive income of a foreign subsidiary directly to the German shareholder if: (a) German residents hold more than 50% of the shares, (b) the subsidiary's income is predominantly passive (interest, royalties, certain dividends), and (c) the foreign effective tax rate is below 25%. Cyprus's 12.5% corporate rate, and certainly the effective rate under the IP Box, falls well below that 25% threshold, meaning a German-resident shareholder's Cyprus holding company could face German CFC attribution on passive income unless a substance safe harbour is met.

The UK's CFC rules under Part 9A TIOPA 2010 operate on a similar logic but with important differences. The UK applies a gateway test that first determines whether income belongs to a CFC, then checks whether an exemption applies. The full territorial exemption, the excluded territories exemption (Cyprus is not on that list), and, critically, the significant people functions (SPF) exemption are the main defences. If the key entrepreneurial risk-taking functions for the income are genuinely located in Cyprus, the SPF exemption applies and CFC attribution to the UK parent is blocked. Spain (under Article 91 LIRPF and Article 100 LIS) and France (Article 209B CGI) follow broadly the OECD BEPS Action 3 model, with effective rate tests ranging from below 50% of the domestic rate (Spain) to below 60% of the French rate (France), all of which Cyprus's standard rate satisfies.

The substance safe harbour is the primary and most robust defence against CFC rules across all major jurisdictions. What constitutes adequate substance is fact-specific, but common indicators include: a local Cyprus management team with genuine decision-making authority, local office premises (not a registered address), board meetings held and minuted in Cyprus, local bank accounts operated by Cyprus-based directors, and key contracts negotiated and executed in Cyprus. The BEPS Action 5 framework that Cyprus operates under, the modified nexus approach for IP, also directly informs substance requirements for IP Box claims and CFC defence simultaneously, making well-documented substance a dual-purpose asset.

A practical point that often gets overlooked: CFC rules target passive income, not active business income. A Cyprus company that genuinely operates a business, employing staff, delivering services, managing client relationships, is far less vulnerable than a pure holding company receiving dividends and royalties. Entrepreneurs who move to Cyprus, run their operations from the island, and maintain Cyprus tax residency under the 60-day rule are in a structurally different position from a German resident who sets up a Cyprus holding but continues to work and live in Germany. The former scenario is a clean international tax structure; the latter is the scenario CFC rules were designed to address.

The Cyprus Holding Company vs the Estonian OÜ vs the Irish Holding: A Direct Comparison

Estonia's distributed profit model, where corporate tax is deferred until dividends are paid, at which point a 20% (or 14% for regular distributions) rate applies, is often cited as a competitor to Cyprus for digital entrepreneurs. The comparison is misleading for high-income founders. An Estonian OÜ retains profits tax-free only as long as they remain in the company; the moment a founder takes a dividend, the Estonian corporate tax (20%) applies before personal taxation in the founder's residence country. A Cyprus Non-Dom founder takes dividends subject to 15% corporate tax plus 2.65% GHS, with 0% further income tax, a total effective rate of approximately 17-18% through the full chain, with no deferral risk and no clawback on distribution.

Ireland presents a genuinely competitive holding regime for certain structures, particularly those involving substantial EU-source royalties or where the 12.5% rate on trading income is the primary driver. Ireland's participation exemption on dividends and capital gains from qualifying subsidiaries is broad, and its treaty network (73 treaties) is extensive. However, Ireland's substance requirements are stringent and enforcement has intensified post-BEPS, the cost of establishing and maintaining a compliant Irish holding structure with genuine local management is materially higher than Cyprus. Ireland also lacks the personal tax benefit: an Irish-resident founder faces income tax at up to 40% plus USC and PRSI on salary or dividends taken personally, with no Non-Dom dividend exemption equivalent to Cyprus's.

The table below captures the key variables for an entrepreneur earning primarily dividend income from an operating subsidiary, evaluating Cyprus, Estonia, and Ireland as the holding jurisdiction, assuming the founder moves to and tax-resides in each respective country:

Cyprus: Corporate tax 15% | Effective dividend tax at holding level ~0% (participation exemption within group) | Personal dividend tax (Non-Dom) 0% income + 2.65% GHS | Total effective rate on distributed profits ~5% | Substance cost: low-to-medium | Treaty network: 68 treaties | CFC risk (from Germany): moderate without substance, low with genuine substance. Estonia: Corporate tax 0% on retained / 20% on distribution | Personal dividend tax: varies by residence | Total effective rate on distributed profits: 20%+ on distribution | Substance cost: low | Treaty network: 62 treaties | CFC risk: similar to Cyprus. Ireland: Corporate tax 12.5% trading / 25% passive | Personal income tax up to 40% + USC + PRSI | Total effective rate on distributed profits: 35-55% for Irish-resident founder | Substance cost: high | Treaty network: 73 treaties | CFC risk: low (OECD-compliant, excluded territories in many CFCs).

The Cyprus advantage is most pronounced precisely for the profile this guide targets: a founder or investor who is willing to actually relocate, take Cyprus tax residency under the 60-day rule, and structure their income primarily as dividends from a Cyprus holding company. No other EU jurisdiction combines a sub-5% effective rate on dividend income with a genuine lifestyle proposition, full EU access, English-language legal system, and a cost of living materially below Western European capitals. Estonia and Ireland are legitimate choices for specific fact patterns, particularly where the founder will not relocate, but neither competes with Cyprus on the combined tax and lifestyle outcome for a relocating entrepreneur.

Lifestyle Arbitrage: When Tax Planning and Quality of Life Align

Tax planning and quality of life are usually presented as a trade-off: you pay for low taxes with geographic inconvenience, poor infrastructure, or social isolation. Cyprus breaks that framing. An entrepreneur moving from Munich, London, or Madrid to Limassol or Paphos is not making a sacrifice, they are moving to a Mediterranean island with 340 days of sunshine per year, a functioning EU healthcare system (GESY), English as a de facto second language, a growing international professional community, direct flights to most European capitals, and a cost of living that is 30-40% lower than Western European major cities on a like-for-like basis.

Consider the full financial picture for an entrepreneur earning EUR 300,000 per year in Germany, structured as a GmbH paying salary plus dividends. German corporate tax on GmbH profits runs at approximately 30% (corporate tax plus trade tax, Gewerbesteuer). Dividends paid to a German-resident shareholder face the Abgeltungsteuer at 25% plus Solidaritätszuschlag. Salary is subject to income tax at the marginal rate of up to 45% plus social security contributions. The combined tax burden on EUR 300,000 in annual income through a German structure easily exceeds EUR 130,000-150,000 per year. A comparable Cyprus Non-Dom structure, EUR 300,000 taken as dividends from a Cyprus holding company, generates approximately EUR 15,000-17,000 in total tax and GHS contributions. The annual tax saving is in the range of EUR 115,000-135,000.

Cost-of-living arbitrage compounds the tax saving. Renting a well-appointed three-bedroom apartment in Limassol's business district costs EUR 2,500-3,500 per month, comparable to a modest one-bedroom in Munich or a small flat in a second-tier London neighbourhood. Private school fees, dining, transportation, and leisure costs are all materially lower. A family with two children relocating from Germany to Cyprus can realistically reduce their total annual cost of living by EUR 30,000-50,000 while maintaining or improving objective quality of life metrics: climate, safety, international school quality, and access to outdoor activities.

The total annual financial benefit, tax saving plus cost-of-living reduction, for a EUR 300,000/year earner relocating from Germany to Cyprus can exceed EUR 150,000. Over a five-year horizon, the compounding effect of reinvesting those savings is transformative for wealth accumulation. The critical point is that this is not a grey-area tax scheme requiring aggressive positions or opaque structures. Cyprus is an EU member state with a clean tax reputation, full exchange-of-information compliance, and a tax authority that applies its rules transparently. The benefit is structural and legal, it arises because Cyprus has deliberately designed its tax system to attract internationally mobile talent and capital.

Common International Tax Planning Mistakes

Moving too fast without exit planning is the most expensive mistake. Many entrepreneurs focus entirely on the destination tax regime and ignore the exit tax implications in their home country. Germany imposes a deemed disposal tax (Wegzugsteuer) under §6 AStG on shares in corporations held at greater than 1% when a resident emigrates, the unrealised gain is taxed as if the shares were sold on the day of departure. The UK has similar anti-avoidance rules for individuals who emigrate and return within five years (the temporary non-residence rules). France, Spain, and Italy all have exit tax regimes. Failing to model the exit tax cost before restructuring can eliminate years of prospective tax savings in a single assessment.

Not establishing genuine substance is the second critical error. A Cyprus company with a registered address, a nominee director, and no actual operations is not a legitimate tax structure, it is a shell company that fails the substance tests required by Cyprus domestic law, EU anti-avoidance directives, and the economic employer / significant people functions tests used in CFC analysis. Genuine substance means real people making real decisions in Cyprus: at minimum, a resident director with relevant expertise, regular board meetings held in Cyprus, local bank accounts operated locally, and documented decision-making trails. The cost of proper substance, EUR 30,000-60,000 per year for a well-run structure, is a rounding error relative to the tax savings; cutting corners on substance is false economy.

Maintaining excessive ties to the home country after relocation is a structural vulnerability that audits exploit. Tax authorities in Germany, the UK, and Spain apply the centre-of-life / habitual abode tests aggressively in residency disputes. Keeping the family home in Germany while renting in Cyprus, holding a German driving licence, maintaining German club memberships and bank accounts as primary accounts, and spending significant time in Germany for business meetings all create factual ammunition for a German tax authority to argue continued German tax residency. The 60-day Cyprus rule is a sufficient condition for Cyprus tax residency, but it does not automatically sever home-country residency, that requires active steps to break the home-country tax residence tie, which varies by jurisdiction.

Ignoring social security implications can create unexpected costs that partially offset tax savings. EU Regulation 883/2004 on social security coordination determines which member state's social security system applies to an EU citizen, it is not freely choosable. Self-employed individuals who move to Cyprus but continue providing services primarily to clients in their home country may find that home-country social security continues to apply for up to two years under the posting rules, or that Cyprus social insurance (16.6% self-employed on 80% of profits, capped) applies from day one of Cyprus self-employment. Non-EU situations, entrepreneurs from the US, UK post-Brexit, Israel, require analysis of the applicable bilateral social security agreement or, absent one, the risk of dual contributions. Getting professional advice on social security at the same time as tax advice is not optional, it is a prerequisite for accurate financial modelling.

Finally, treating international tax planning as a one-time transaction rather than an ongoing compliance discipline is a mistake that compounds over time. Tax laws change, the 2025-2026 Cyprus reform package itself introduced new income tax bands, changed the SDC rate on dividends for domiciled taxpayers, and added the crypto flat rate. Substance requirements evolve as BEPS implementation matures. Home-country CFC rules are updated regularly. A structure that was optimal and compliant in 2022 may require review in 2026. Building a relationship with a qualified Cyprus tax adviser, maintaining clean corporate records, and conducting an annual structure review are not bureaucratic overhead, they are the maintenance cost of keeping a valuable tax asset in working order.

Free, no commitment

Moving to Cyprus or opening a company?

Tell us your situation and we'll connect you with our specialist expat advisory in Cyprus: Non-Dom tax, company setup and residency, done for you. Free consultation, no commitment.

Free newsletter

What do you want to hear about?

No spam. Unsubscribe any time.