Cyprus vs Estonia: Tax Calculator & Full Comparison 2026

Interactive calculator: Estonia OÜ vs Cyprus Ltd + Non-Dom. See exact tax for your revenue. 2026 rates for both countries.

Last updated: 2026-06-01

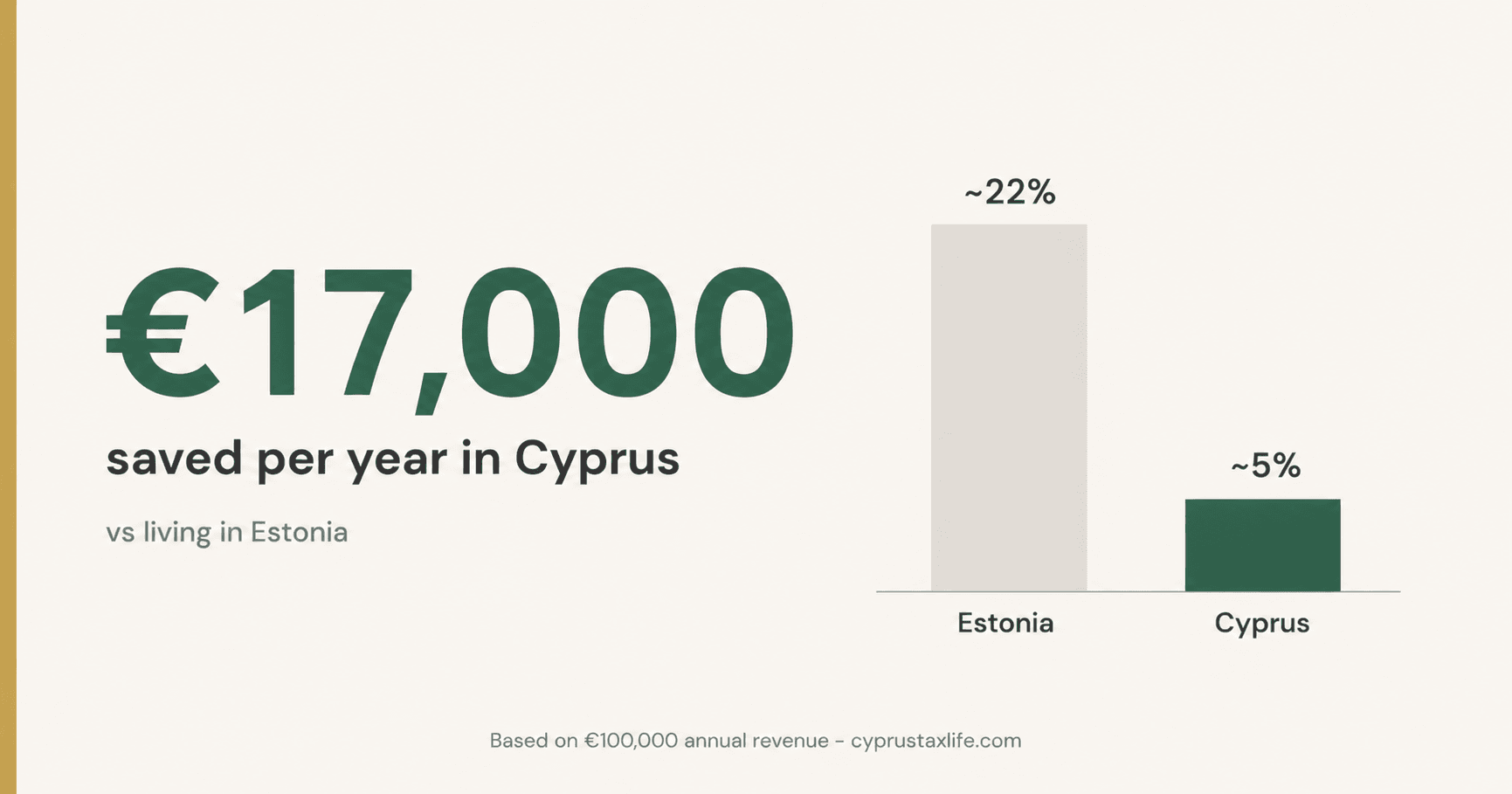

Effective tax rate comparison

~22% (when distributing)

Estonia

~5%

Cyprus Non-Dom

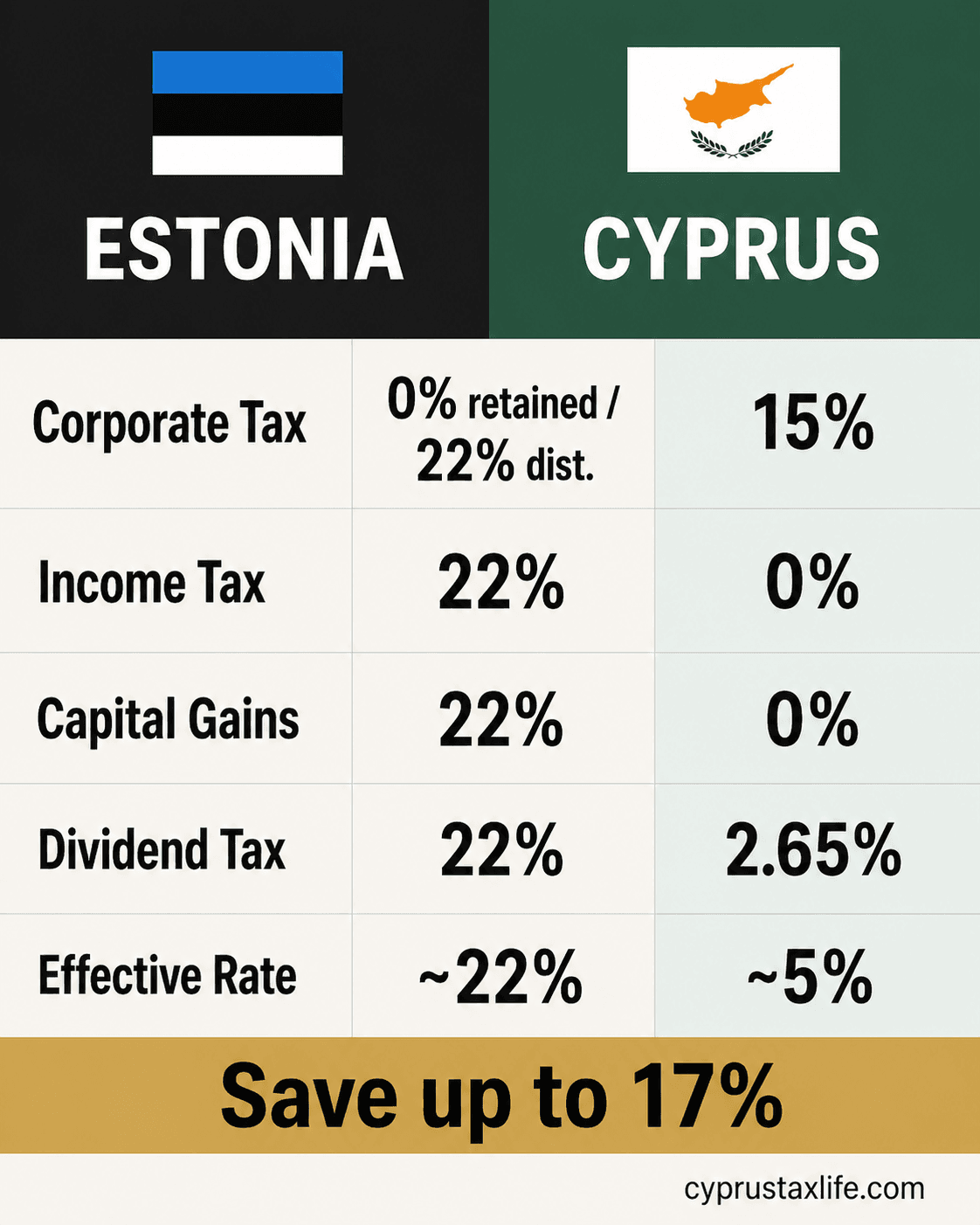

Tax Comparison: Estonia vs Cyprus

| 🇪🇪 Estonia | 🇨🇾 Cyprus (Non-Dom) | |

|---|---|---|

| Corporate tax | 0% on retained / 22% on distributed | 15% |

| Income tax | 22% (flat) | 0% (dividends) |

| Capital gains tax | 22% (when distributed) | 0% (no Cyprus property) |

| Dividend tax | 22% at company level (no additional personal tax) | 0% income tax + 2.65% GHS |

| Wealth tax | None | None |

| Social contributions | ~1.6% employee + ~33.8% employer (on salary) | ~4% on salary (capped) |

| Effective rate (entrepreneur) | ~22% (when distributing) | ~5% |

| VAT | 22% | 19% |

Tax Burden in Estonia

Estonia's corporate tax system is unique in Europe: companies pay 0% tax on retained profits. The 22% corporate tax rate (raised from 20% in 2025) only applies when profits are distributed as dividends. This "distribution tax" system means Estonian companies can accumulate profits indefinitely without paying tax.

The e-Residency program allows foreigners to establish Estonian companies remotely (without living in Estonia), but tax residency of the company depends on where management is exercised - not where the shareholders reside. An Estonian company managed from, say, Spain, would be considered a Spanish tax resident.

For an entrepreneur genuinely residing and managing their business from Estonia: personal income tax is a flat 22% (no progressive rates). Social security contributions are significant: the employer pays 33.8% (pension fund and health insurance) on top of the gross salary, and the employee pays 1.6%. For self-employed, the total social burden is 35.4% of declared income.

The practical implication: if you need to extract money (dividends), the effective rate on EUR 100,000 of revenue is approximately 22% (the company pays 22% when distributing, and shareholders receive dividends net of this tax with no additional personal income tax). If you can leave money in the company indefinitely, the "effective rate" is 0% until distribution.

Why Cyprus is Better for Entrepreneurs

Estonia's system is excellent for companies that can leave profits in the company (to reinvest, grow, or hold). Cyprus is better when you need to extract money now.

The key comparison: when an Estonian entrepreneur distributes EUR 100,000 of profits, they pay 22% (EUR 22,000). When a Cyprus Non-Dom entrepreneur distributes EUR 100,000 of profits (from a Cyprus Ltd that paid 15% tax), they have already paid EUR 15,000 in corporate tax, and the remaining EUR 85,000 is distributed with only 2.65% GHS (~EUR 2,250). Total: EUR 17,250, approximately 17.25% effective - lower than Estonia's 22%.

But Cyprus is even simpler: on EUR 100,000 of revenue, the total effective rate is approximately 5% (15% corporate tax on profits, then 2.65% GHS on dividends, and since the entrepreneur typically takes a salary up to EUR 19,500 exempt threshold, the overall blended rate is ~5%). This is genuinely lower than Estonia for comparable income extraction.

Estonia's advantage: if you can leave money in the company for years, the 0% deferral is valuable. But most entrepreneurs need to extract money to live. For lifestyle-driven entrepreneurs who need to pay themselves, Cyprus wins clearly.

Tax Calculation: EUR 100,000

🇪🇪 Estonia

🇨🇾 Cyprus (Non-Dom)

Annual savings moving to Cyprus

EUR 17,000

EUR 85,000 over 5 years

Double Tax Treaty: Estonia - Cyprus

Estonia and Cyprus have a double tax treaty in force. Key provisions: dividends 0-5%, interest 0-10%, royalties 5-10%. Both are EU members, so EU directives apply and reduce withholding taxes to 0% for qualifying intra-EU transactions. The treaty provides clear rules for entrepreneurs using both countries. Estonia's e-Residency is purely an administrative program and does not create Estonian tax residency - this is a common misconception.

Exit Tax and Emigration from Estonia

Estonia does not impose a formal exit tax on individuals. Estonian companies that transfer their place of effective management abroad may trigger CIT on undistributed profits at that point (distribution tax becomes due on the retained earnings). This is a significant consideration for entrepreneurs who have accumulated large retained earnings in an Estonian OÜ before deciding to relocate. The entire retained profit reserve would become taxable if the company is deemed to have left Estonian tax jurisdiction.

Cost of Living: Estonia vs Cyprus

Estonia (Tallinn) offers a relatively low cost of living compared to Western Europe. Rent for a 2-bedroom apartment in Tallinn: EUR 800-1,300. Estonia is approximately 20-30% cheaper than Cyprus in housing. However, Estonian winters are harsh (temperatures often below -15°C) compared to Cyprus's mild winters (10-16°C). Summer in Estonia is pleasant but short. For lifestyle-driven entrepreneurs prioritizing Mediterranean climate, Cyprus clearly wins. For those prioritizing tech ecosystem and Eastern European culture, Tallinn is an interesting choice. Monthly living costs: Tallinn EUR 1,200-2,000, Cyprus EUR 1,500-2,500.

Practical Steps to Relocate

Evaluate how frequently you need to extract profits (determines if Estonia's deferral is valuable)

Establish a Cyprus Ltd (5-7 working days, approximately EUR 2,100)

Apply for Cyprus tax residency (60-day or 183-day rule)

Register as Non-Dom at the Cyprus Tax Department

Obtain your Yellow Slip

Open a Cyprus bank account

If moving from Estonia: address accumulated retained earnings in any Estonian OÜ (plan distribution or company transfer carefully)

Deregister from Estonian tax residency (submit Form R2 to Maksu- ja Tolliamet)

Set up Cyprus payroll structure

Register for GHS healthcare contributions

Frequently Asked Questions

Does Estonian e-Residency give me tax benefits?+

If Estonia has 0% tax on retained profits, why switch to Cyprus?+

What happens to accumulated Estonian retained earnings if I move?+

Can I use both Estonia and Cyprus in my structure?+

How does Estonia's tech scene compare to Cyprus?+

What is the VAT rate in Estonia vs Cyprus?+

Sources and References

Tax data: PwC Worldwide Tax Summaries, KPMG Tax Guides (2025/2026), Big Four country guides, government tax authority publications. Effective rates are approximations for entrepreneur structures (company + low salary + dividends). Consult a qualified tax advisor before making decisions.

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Related Articles

![Best Holding Company [2026]: Cyprus vs 4 Rivals](https://cdn.sanity.io/images/glqahhks/production/9ec5328706d63fc458c40c9b2e7d80c38816e68f-1678x937.jpg?w=700&q=75&auto=format)

Compare Cyprus, Luxembourg, Netherlands and Malta as holding jurisdictions. Cyprus: 3% effective on dividends, 0% CGT, under EUR 7,000/year to maintain.

Miriam Alonso

Miriam Alonso- Company & Accounting

![Cyprus Withholding Tax on Dividends [2026]: 0% Guide](https://cdn.sanity.io/images/glqahhks/production/d06fdbecc2a60a7a2c152fdeaa9dc27d4c596810-1679x937.jpg?w=700&q=75&auto=format)

Learn why Cyprus charges 0% withholding on dividends to non-residents. SDC at 5% applies only to Cyprus-domiciled recipients. Includes treaty rates table.

Miriam Alonso- Tax Planning

![Cyprus Ltd vs UK Ltd [2026]: 5 Key Differences](https://cdn.sanity.io/images/glqahhks/production/e89433a9e5baf35b8c64e7bf69af332c4dce01c2-1679x937.jpg?w=700&q=75&auto=format)

Compare Cyprus Ltd vs UK Ltd: 15% vs 25% corp tax, 2.65% vs 39.35% dividend tax, and full EU access. Complete guide for British entrepreneurs in 2026.

Miriam Alonso- Company & Accounting