Moving from Denmark to Cyprus

Quick Answer

Moving from Denmark to Cyprus with Non-Dom status reduces your effective tax rate from ~45-52% to approximately 5%. Cyprus applies 0% Special Defence Contribution on foreign dividends, a flat 15% corporate tax, and offers tax residency with just 60 days of physical presence per year under the 60-day rule. A double tax treaty between Denmark and Cyprus prevents double taxation during the transition.

Last updated: 2026-05-29

Why Denmark Professionals Consider Cyprus

Denmark consistently ranks among the highest-taxed countries in the world. While the public services are excellent, the tax burden on entrepreneurs and high earners is crushing. The top marginal income tax rate reaches 55.9% when combining state tax (15%), municipal tax (~25%), church tax (~0.7%), and the AM-bidrag (labor market contribution of 8%).

For entrepreneurs running an ApS (the Danish equivalent of a Ltd), the corporate tax rate is 22%. Dividend distributions are then taxed at 27% on the first DKK 61,000 and 42% above that threshold. This double layer means that on DKK 1,000,000 of profit, you keep approximately DKK 450,000 after all taxes.

Denmark also applies share income taxation at 27% (up to DKK 61,000) and 42% (above), making capital gains on business exits extremely expensive.

The cost of living in Copenhagen and major Danish cities is among the highest in Europe. A 2-bedroom apartment in Copenhagen costs DKK 12,000-18,000 (EUR 1,600-2,400) per month in rent alone. Add to that among the highest grocery prices in the EU, expensive restaurants, and high car ownership costs (registration tax up to 150%), and the total financial picture pushes many entrepreneurs to consider alternatives.

The Danish work culture, while admirable in many ways, can also feel restrictive for internationally-minded entrepreneurs who want more flexibility in how they structure their time and business.

Denmark Tax Burden at a Glance

| Tax type | 🇩🇰 Denmark |

|---|---|

| Income tax | Up to 55.9% (including AM-bidrag) |

| Corporate tax | 22% |

| Capital gains tax | 27-42% on shares |

| Dividend tax | 27% up to DKK 61,000, then 42% |

| Social contributions | 8% AM-bidrag + employer contributions |

| Effective rate | ~45-52% |

Tax Comparison: Denmark vs Cyprus

The tax savings from moving to Cyprus are dramatic for Danish entrepreneurs. Under the Cyprus Non-Dom regime, the effective tax rate drops from approximately 45-52% to just ~5%.

Here is a concrete comparison on EUR 100,000 of business revenue:

In Denmark (ApS + salary/dividends): Corporate tax at 22% on profit = EUR 22,000. Remaining EUR 78,000 distributed as dividends, taxed at ~35% blended rate = EUR 27,300. Total tax: approximately EUR 49,300 (49.3% effective).

In Cyprus (Ltd + Non-Dom): Corporate tax at 15% = EUR 15,000. Low salary (within exempt threshold) plus dividends at 0% income tax + 2.65% GHS. Total tax: approximately EUR 5,000 (5% effective).

Annual savings: approximately EUR 44,300 on EUR 100,000 revenue. Over five years, that represents EUR 221,500 in additional retained earnings.

Beyond the tax rate, Cyprus offers simplicity. No church tax, no AM-bidrag, no progressive dividend brackets, no municipality-dependent tax rates. One flat corporate rate, zero dividend income tax, one simple healthcare contribution.

Interactive Tax Calculator

Denmark

Effective rate

48%

Est. tax: €48,000

Cyprus (Non-Dom)

Effective rate

5%

Est. tax: €5,000

Annual savings by moving to Cyprus

€43,000

Estimates based on effective rates. Consult a tax advisor for your specific situation.

Cyprus Non-Dom: ~5% effective tax

The alternative most entrepreneurs do not know about

- ✓15% corporate tax (flat, no surcharges)

- ✓0% dividend income tax (Non-Dom)

- ✓2.65% GHS on all income

- ✓No wealth tax, no inheritance tax

- ✓60-day rule for flexible tax residency

- ✓Full EU membership and treaty network

Double Tax Treaty: Denmark - Cyprus

Denmark and Cyprus have a double tax treaty in force. Withholding tax rates: dividends 0-15% (0% if the beneficial owner is a company holding at least 10% of capital), interest 0%, royalties 0%. Pensions paid from Danish sources to Cyprus residents are generally taxable only in Cyprus under the treaty (though Denmark may retain taxing rights on government pensions). Capital gains on shares are taxable only in the state of residence of the seller. Danish entrepreneurs should note that Denmark has strong substance requirements and may challenge arrangements that lack genuine business purpose.

Leaving Denmark: Exit Process

Denmark has a relatively straightforward exit process, but with important requirements:

Deregistration: You must deregister from the CPR (Civil Registration System) by notifying your municipality at least 5 days before departure. This involves visiting your local Borgerservice office.

Final tax return: You must file a final Danish tax return covering the year of departure. Income earned up to the date of departure remains taxable in Denmark.

Exit taxation on shares: Denmark can impose exit tax (fraflytningsbeskatning) on unrealized gains on shares worth more than DKK 100,000 when the shareholder emigrates. For moves within the EU, the payment can be deferred with annual reporting. The deferral is interest-free but requires filing annual returns with SKAT (Danish tax authority).

Pension: Your ATP (labor market pension) and any private pension contributions are preserved. Danish state pension eligibility depends on years of residence (minimum 3 years, full pension at 40 years). Moving to an EU country does not forfeit accrued rights.

Healthcare: Your Danish health card (Sundhedskort) expires upon deregistration. You will transition to the Cyprus GHS system upon establishing residency.

Bank accounts: Most Danish banks will allow you to keep your account after emigration, but you must update your tax residency information. Some banks may request additional documentation.

Fraflytningsbeskatning: The Danish Exit Tax on Shares Explained

Denmark's exit tax on shares, known as fraflytningsbeskatning, is one of the most detailed in Europe. It applies when a Danish tax resident emigrates and holds shares or participations with a total market value exceeding DKK 100,000 on the date of departure. The tax is calculated on unrealized capital gains - the difference between the market value at departure and the original acquisition cost.

How it works in practice: when you emigrate, you must include the exit tax calculation in your final Danish tax return (slutsopgorelse). SKAT will assess the unrealized gain and calculate the tax due. The applicable rate is 27% on the first DKK 61,000 of gain and 42% on amounts above that threshold (the standard share income rates).

For moves within the European Union - including to Cyprus - Danish law provides an automatic deferral (henstand) without interest charges. You do not pay the tax on the day you leave. Instead, you report annually to SKAT using form 02.029, confirming that you still hold the shares and have not disposed of them. As long as the deferral conditions are met, no cash payment is required.

The deferral immediately ceases and the full deferred tax becomes payable if: you sell or transfer the shares, you cease to be a resident of an EU or EEA member state (for example, if you later move to a non-EU country), the company whose shares are held is no longer resident in Denmark or another EU/EEA state, or you fail to submit the required annual declaration to SKAT.

Numerical example: a Danish entrepreneur owns an ApS with a total value of DKK 1,000,000. The shares were acquired for DKK 200,000. The unrealized gain is DKK 800,000. At the 42% rate (above the DKK 61,000 threshold), the exit tax assessed is approximately DKK 336,000. Moving to Cyprus and deferring under the EU provisions means zero cash outflow at departure. If the entrepreneur spends 5 years in Cyprus without selling the ApS, zero tax is paid during that period. If in year 5 the ApS is sold for DKK 1,200,000, the gain realized from the sale date is a new capital event - potentially taxable in Cyprus under the Denmark-Cyprus double tax treaty, which allocates capital gains on shares to the state of residence (Cyprus). The pre-departure deferred gain of DKK 800,000 then becomes exigible to SKAT. The interaction between the deferred Danish gain and the treaty allocation requires careful professional analysis, as the outcome depends on the structure and timing of the transaction.

Cost of Living: Denmark vs Cyprus

The cost of living difference between Denmark and Cyprus is substantial. Monthly comparison for a single professional:

Housing: Copenhagen EUR 1,600-2,400 vs Larnaca EUR 550-750 (savings: 55-70%) Groceries: Denmark EUR 400-500 vs Cyprus EUR 250-350 (savings: 30-40%) Dining out: Denmark EUR 300-400 vs Cyprus EUR 150-200 (savings: 50%) Transport: Denmark EUR 80-100 (public) vs Cyprus EUR 100-150 (car-based, but no registration tax) Healthcare: Denmark (free via tax) vs Cyprus (2.65% GHS contribution, approximately EUR 200-300/month) Utilities: Denmark EUR 200-250 vs Cyprus EUR 100-150 (less heating needed)

Total monthly: Denmark EUR 2,800-3,700 vs Cyprus EUR 1,400-1,900

The savings are particularly notable for car owners. Denmark's infamous car registration tax (up to 150%) makes vehicle ownership extremely expensive. In Cyprus, there is no equivalent surcharge, and a quality used car costs approximately EUR 10,000-20,000.

The climate difference alone is worth noting: 1,800 hours of sunshine annually in Copenhagen versus 3,400 in Cyprus.

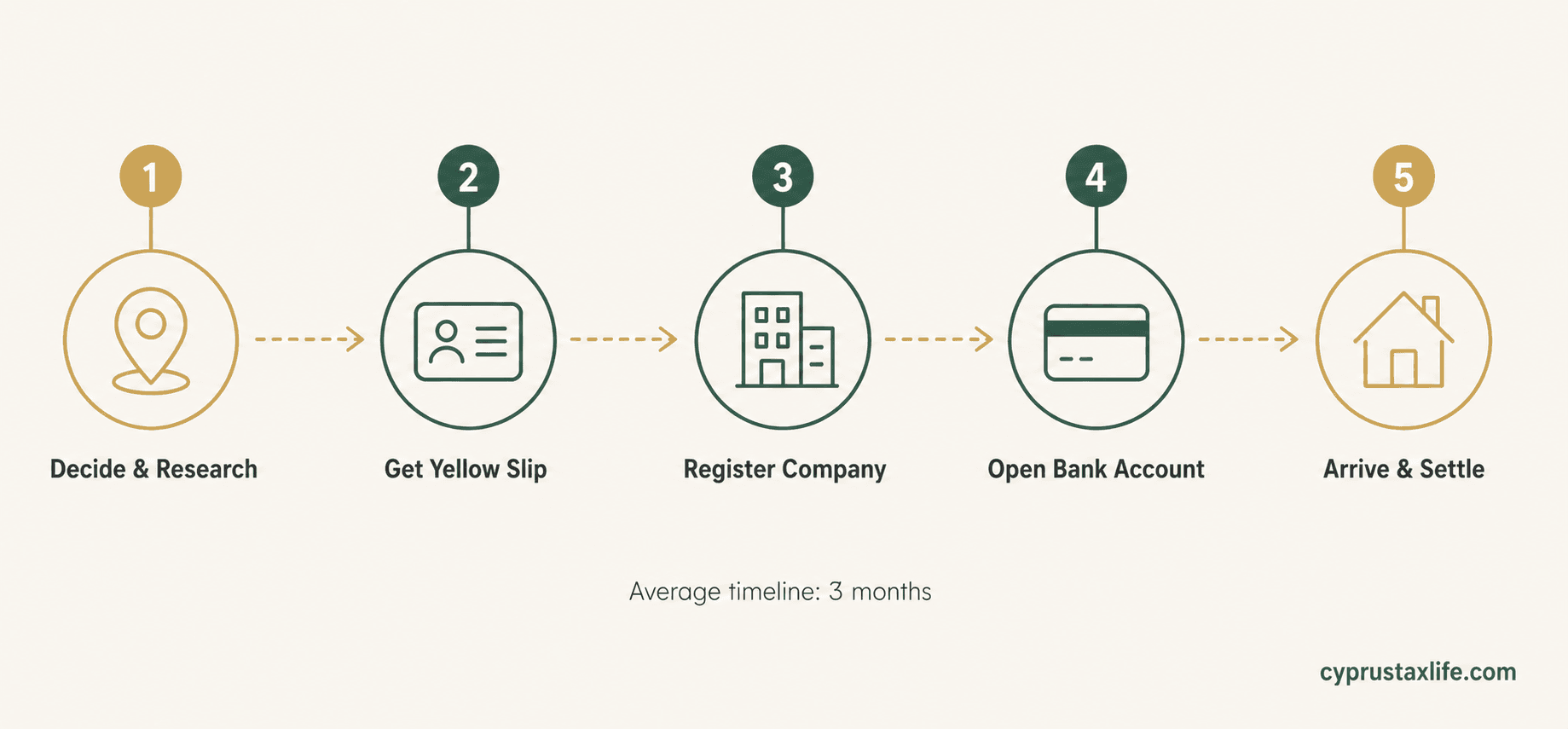

Step-by-Step Relocation Checklist

Research and choose your Cyprus city (Larnaca, Limassol, Paphos, or Nicosia)

Set up a Cyprus Ltd company (5-7 working days, approximately EUR 2,100)

Find accommodation in Cyprus and sign a rental contract

Deregister from CPR at your local Borgerservice

Notify SKAT (Danish tax authority) of your emigration

File your final Danish tax return

Address exit tax on shares if applicable (fraflytningsbeskatning)

Apply for Cyprus tax residency (60-day or 183-day rule)

Register for Non-Dom status at the Cyprus Tax Department

Obtain your Yellow Slip (EU citizen registration)

Open a Cyprus bank account

Register for GHS healthcare

Set up your payroll structure (low salary + dividends)

Transfer relevant pension information to your new advisor

Frequently Asked Questions

Do I still need to pay Danish taxes after moving to Cyprus?+

What happens to my Danish pension (ATP) when I move?+

Can I use the Cyprus 60-day rule as a Danish citizen?+

How much can I save by moving from Denmark to Cyprus?+

Is there a Danish community in Cyprus?+

What about schooling for children in Cyprus?+

If an ApS has multiple shareholders, does the exit tax apply to each one separately?+

I have Danish ratepension or livsvarig pension accounts. How do they work after I move?+

Sources and References

- PwC Worldwide Tax Summaries — Cyprus

- KPMG Cyprus — Tax and Advisory

- EY Cyprus — Tax Services

- Cyprus Ministry of Finance (mof.gov.cy)

Effective rates are approximations for entrepreneur structures (company + low salary + dividends). Consult a qualified tax advisor before making decisions.

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Related Articles

![Best Holding Company [2026]: Cyprus vs 4 Rivals](https://cdn.sanity.io/images/glqahhks/production/9ec5328706d63fc458c40c9b2e7d80c38816e68f-1678x937.jpg?w=700&q=75&auto=format)

Compare Cyprus, Luxembourg, Netherlands and Malta as holding jurisdictions. Cyprus: 3% effective on dividends, 0% CGT, under EUR 7,000/year to maintain.

Miriam Alonso

Miriam Alonso- Company & Accounting

![Cyprus Withholding Tax on Dividends [2026]: 0% Guide](https://cdn.sanity.io/images/glqahhks/production/d06fdbecc2a60a7a2c152fdeaa9dc27d4c596810-1679x937.jpg?w=700&q=75&auto=format)

Learn why Cyprus charges 0% withholding on dividends to non-residents. SDC at 5% applies only to Cyprus-domiciled recipients. Includes treaty rates table.

Miriam Alonso- Tax Planning

![Cyprus Ltd vs UK Ltd [2026]: 5 Key Differences](https://cdn.sanity.io/images/glqahhks/production/e89433a9e5baf35b8c64e7bf69af332c4dce01c2-1679x937.jpg?w=700&q=75&auto=format)

Compare Cyprus Ltd vs UK Ltd: 15% vs 25% corp tax, 2.65% vs 39.35% dividend tax, and full EU access. Complete guide for British entrepreneurs in 2026.

Miriam Alonso- Company & Accounting