Moving from Norway to Cyprus

Quick Answer

Moving from Norway to Cyprus with Non-Dom status reduces your effective tax rate from ~42-48% to approximately 5%. Cyprus applies 0% Special Defence Contribution on foreign dividends, a flat 15% corporate tax, and offers tax residency with just 60 days of physical presence per year under the 60-day rule. A double tax treaty between Norway and Cyprus prevents double taxation during the transition.

Last updated: 2026-05-29

Why Norway Professionals Consider Cyprus

Norway offers one of the highest standards of living in the world, but this comes at a significant tax cost. The income tax system combines a flat tax on general income (22%) with a progressive bracket tax (trinnskatt) that adds 1.7% to 17.4% on higher incomes. The maximum combined marginal rate reaches 46.4%.

For entrepreneurs, Norway presents a particularly challenging tax environment. The corporate tax rate is 22%. Dividends received by individual shareholders are taxed through the "shareholder model" (aksjonarmodellen), which applies a 1.72 uplift factor to the base 22% rate, resulting in an effective dividend tax rate of 37.84% on amounts exceeding a risk-free return allowance.

Norway is also one of the few countries that still levies a wealth tax (formueskatt). The rate is 1% on net wealth above NOK 1,700,000 (approximately EUR 145,000) and 1.1% above NOK 20,000,000, with municipalities adding approximately 0.7%. This applies to worldwide assets for Norwegian tax residents, including shares, property, bank deposits, and other investments.

The combined effect is punishing for successful entrepreneurs. On NOK 1,000,000 of company profit, after corporate tax (NOK 220,000) and dividend tax on the remaining NOK 780,000 (approximately NOK 295,000), the total tax bill reaches approximately NOK 515,000, an effective rate of 51.5%.

Additionally, Norway taxes petroleum income at an extraordinary rate (78% combined), which affects the broader economy and cost structure. While entrepreneurs outside the oil sector do not pay this directly, the high-cost environment it creates affects everyone.

Norway Tax Burden at a Glance

| Tax type | 🇳🇴 Norway |

|---|---|

| Income tax | Up to 46.4% (including bracket tax) |

| Corporate tax | 22% |

| Capital gains tax | 37.84% (22% x 1.72 uplift factor) |

| Dividend tax | 37.84% (22% x 1.72 uplift factor) |

| Social contributions | ~8.2% employee + ~14.1% employer |

| Effective rate | ~42-48% |

Tax Comparison: Norway vs Cyprus

Moving to Cyprus transforms the tax equation for Norwegian entrepreneurs:

On EUR 100,000 of business revenue: Norway (AS + salary/dividends): ~EUR 48,000 total tax (48% effective) Cyprus (Ltd + Non-Dom): ~EUR 5,000 total tax (5% effective)

Annual savings: approximately EUR 43,000

But the savings go further because Norway imposes a wealth tax on worldwide assets. An entrepreneur with EUR 1,000,000 in net assets pays approximately EUR 10,000-11,000 annually in Norwegian wealth tax alone. Cyprus has no wealth tax whatsoever.

Over 5 years, a Norwegian entrepreneur with EUR 100,000 annual revenue and EUR 1,000,000 in assets would save approximately EUR 270,000 in total taxes by moving to Cyprus.

The Cyprus Non-Dom structure is simple: a Ltd company paying 15% corporate tax, a low salary within the tax-exempt threshold, and the remainder as dividends with 0% income tax plus 2.65% GHS contribution. No bracket tax, no uplift factors, no wealth tax, no complexity.

Interactive Tax Calculator

Norway

Effective rate

46%

Est. tax: €46,000

Cyprus (Non-Dom)

Effective rate

5%

Est. tax: €5,000

Annual savings by moving to Cyprus

€41,000

Estimates based on effective rates. Consult a tax advisor for your specific situation.

Cyprus Non-Dom: ~5% effective tax

The alternative most entrepreneurs do not know about

- ✓15% corporate tax (flat, no surcharges)

- ✓0% dividend income tax (Non-Dom)

- ✓2.65% GHS on all income

- ✓No wealth tax, no inheritance tax

- ✓60-day rule for flexible tax residency

- ✓Full EU membership and treaty network

Double Tax Treaty: Norway - Cyprus

Norway and Cyprus have a double tax treaty in force. Key provisions: dividends 0-15% withholding (0% if the beneficial owner holds at least 10% of capital), interest 0%, royalties 0%. The treaty provides clear tie-breaker rules for dual residency based on permanent home, center of vital interests, habitual abode, and nationality. Norwegian pensions paid to Cyprus residents are generally taxable in the state of residence (Cyprus). Capital gains on share disposals are taxable only in the state of residence. Norway has a 5-year extended tax liability rule that may apply to certain Norwegian-source income even after emigration. Professional advice is recommended.

Leaving Norway: Exit Process

Norway does not have a traditional exit tax on emigration, but has other important rules:

Extended tax liability: Norway maintains a 5-year rule where former residents who were taxed in Norway for at least 10 of the last 13 years remain liable for Norwegian tax on certain Norwegian-source income (capital gains on Norwegian shares, dividends from Norwegian companies) for 5 years after departure. This can be overridden by a tax treaty if the treaty allocates taxing rights to the new state of residence.

Deregistration: You must notify the National Population Register (Folkeregisteret) of your emigration. If you intend to stay abroad for at least 6 months, you are required to report your departure.

Final tax return: You must file a Norwegian tax return for the year of departure. Income earned in Norway up to the departure date is taxable.

Wealth tax: You stop paying Norwegian wealth tax on worldwide assets from the date you cease to be a Norwegian tax resident. However, Norwegian real estate remains subject to wealth tax regardless of residency.

National Insurance (Folketrygden): You can voluntarily maintain membership for up to 3 years while abroad, or you will be covered by the Cyprus social insurance system under EU coordination rules.

Bank accounts and investments: Norwegian banks require updated tax residency information. Some investment platforms (e.g., ASK - aksjesparekonto) may need restructuring as they are designed for Norwegian tax residents.

Norwegian Wealth Tax and the 2024 Exit Tax: What Changes When You Move to Cyprus

Norway is one of the very few OECD countries that still levies an annual wealth tax on worldwide assets. The formueskat applies to Norwegian tax residents at 1.0% on net taxable wealth above NOK 1,700,000 (approximately EUR 147,000 at 2026 exchange rates). Above NOK 20,000,000, the rate increases to 1.1%. The tax is split between the municipality (0.7%) and the central government (0.3% standard rate, 0.4% on wealth exceeding NOK 20M as of the 2024 reform).

The asset base includes virtually all worldwide wealth: bank accounts, listed shares (valued at 80% of market value), unlisted shares (valued at 100% of their patrimonial value, i.e. the company's net asset value), real estate, vehicles, and other assets. Debts are deducted from the total. The result is an annual tax on wealth that accumulates year after year regardless of whether any income or gains are realized.

For a Norwegian entrepreneur with EUR 1,000,000 in net assets - say, EUR 200,000 in an apartment in Cyprus, EUR 600,000 in shares in a private company, and EUR 200,000 in bank deposits - the full EUR 1,000,000 is subject to Norwegian formueskat (assuming Norwegian tax residency). After subtracting the NOK 1,700,000 exempt floor (approximately EUR 147,000), the taxable base is approximately EUR 853,000. At 1.0%, the annual wealth tax is approximately EUR 8,530. In Cyprus: zero. No wealth tax of any kind exists in Cypriot law.

Over 10 years, that is EUR 85,000 in avoided wealth tax on a EUR 1,000,000 asset base - before accounting for any growth in the asset value.

The 2024 utflyttingsskatt reform is a separate and critically important development. Prior to 2024, Norway did not have a true exit tax on shares. The 5-year extended tax liability rule could impose Norwegian tax on dividends and gains from Norwegian shares for 5 years post-departure, but this was limited in scope. In 2024, Norway fundamentally changed its approach and introduced a genuine exit tax on unrealized capital gains in shares and participations when a taxpayer emigrates.

How the 2024 utflyttingsskatt works: on the date of emigration, the Norwegian Tax Administration (Skatteetaten) calculates the unrealized gain on all shares and participations held by the departing taxpayer. The gain is the difference between market value at departure and the acquisition cost (justert inngangsverdi). The applicable tax rate is 37.84% (the standard shareholder model rate for individual shareholders). If the total unrealized gain across all affected assets is below NOK 500,000, the exit tax does not apply.

For moves to EU or EEA member states - including Cyprus - the 2024 rules allow deferral of the exit tax without interest, provided the taxpayer maintains the shares and complies with annual reporting requirements to Skatteetaten. If the shares are sold within 12 years of emigration, the deferred exit tax becomes payable to Norway at that point. If the shares are not sold within 12 years and the taxpayer has not moved to a non-EU/EEA country in the interim, the deferred exit tax is cancelled.

This 12-year deferral-and-forgiveness structure means that Norwegian entrepreneurs who plan to hold their company for more than 12 years after moving to Cyprus can potentially escape the Norwegian exit tax entirely on those assets. However, any sale within the 12-year window triggers the deferred Norwegian tax in addition to any Cyprus tax on the gain realized post-departure. The interaction between the Norwegian deferred exit tax and the Norway-Cyprus double tax treaty requires careful professional analysis before any asset sale.

Cost of Living: Norway vs Cyprus

Norway is one of the most expensive countries in Europe, and the contrast with Cyprus is dramatic:

Housing: Oslo EUR 1,800-2,800 vs Larnaca EUR 550-750 (savings: 65-75%) Groceries: Norway EUR 500-650 vs Cyprus EUR 250-350 (savings: 45-50%) Dining out: Norway EUR 400-600 vs Cyprus EUR 150-200 (savings: 60-70%) Transport: Norway EUR 100-150 vs Cyprus EUR 100-150 (similar, but cars are much cheaper to buy in Cyprus) Healthcare: Norway (free via tax) vs Cyprus (2.65% GHS) Utilities: Norway EUR 200-300 vs Cyprus EUR 100-150

Total monthly: Norway EUR 3,200-4,500 vs Cyprus EUR 1,400-1,900

The biggest savings for Norwegians are in housing and dining. A quality restaurant meal for two costs EUR 80-120 in Oslo versus EUR 30-40 in Cyprus. Alcohol prices are dramatically lower in Cyprus (no state monopoly like Vinmonopolet). The warmer climate eliminates heating costs that can be substantial in Norwegian winters.

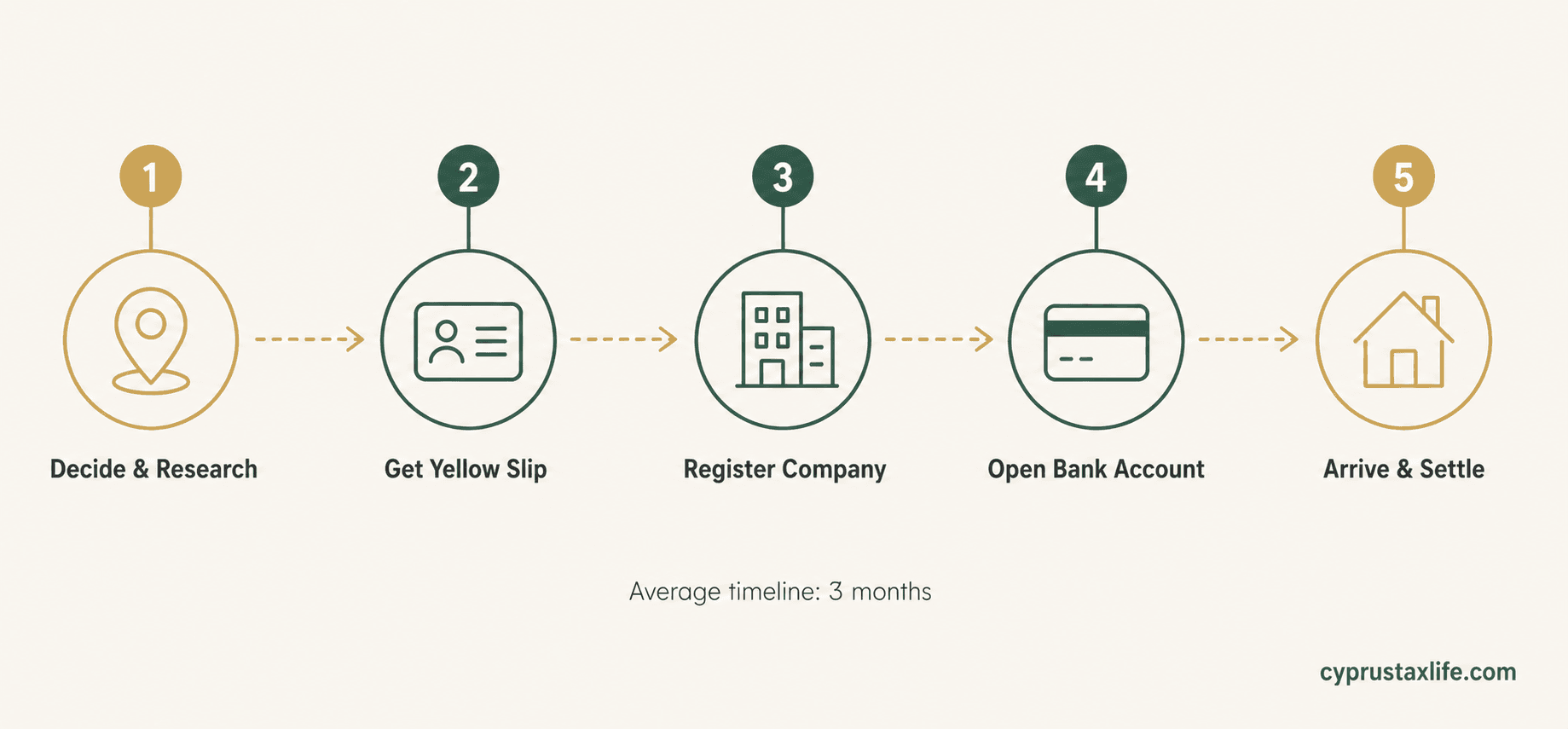

Step-by-Step Relocation Checklist

Research and select your Cyprus location

Establish a Cyprus Ltd company (5-7 working days, approximately EUR 2,100)

Find accommodation in Cyprus

Notify the National Population Register (Folkeregisteret) of your departure

File your final Norwegian tax return (selvangivelse)

Decide on voluntary Folketrygden membership or transition to Cyprus social insurance

Apply for Cyprus tax residency (60-day or 183-day rule)

Register for Non-Dom status

Obtain your Yellow Slip (EEA citizen registration)

Open a Cyprus bank account

Register for GHS healthcare

Restructure Norwegian investment accounts if needed (ASK, BSU)

Set up payroll structure in Cyprus (low salary + dividends)

Inform Norwegian banks and brokers of new tax residency

Frequently Asked Questions

Does Norway have an exit tax?+

Will I still pay Norwegian wealth tax after moving?+

Can I keep my Norwegian AS after moving?+

What about my Norwegian pension (Folketrygden)?+

How much can I save annually by moving from Norway to Cyprus?+

Is there a Scandinavian community in Cyprus?+

How does the 2024 exit tax affect assets held in an ASK (aksjesparekonto)?+

I am keeping my Norwegian property after moving. How much wealth tax will I still owe?+

My Norwegian AS holds foreign assets. How are those valued for the formueskat?+

Sources and References

- PwC Worldwide Tax Summaries — Cyprus

- KPMG Cyprus — Tax and Advisory

- EY Cyprus — Tax Services

- Cyprus Ministry of Finance (mof.gov.cy)

Effective rates are approximations for entrepreneur structures (company + low salary + dividends). Consult a qualified tax advisor before making decisions.

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Related Articles

![Best Holding Company [2026]: Cyprus vs 4 Rivals](https://cdn.sanity.io/images/glqahhks/production/9ec5328706d63fc458c40c9b2e7d80c38816e68f-1678x937.jpg?w=700&q=75&auto=format)

Compare Cyprus, Luxembourg, Netherlands and Malta as holding jurisdictions. Cyprus: 3% effective on dividends, 0% CGT, under EUR 7,000/year to maintain.

Miriam Alonso

Miriam Alonso- Company & Accounting

![Cyprus Withholding Tax on Dividends [2026]: 0% Guide](https://cdn.sanity.io/images/glqahhks/production/d06fdbecc2a60a7a2c152fdeaa9dc27d4c596810-1679x937.jpg?w=700&q=75&auto=format)

Learn why Cyprus charges 0% withholding on dividends to non-residents. SDC at 5% applies only to Cyprus-domiciled recipients. Includes treaty rates table.

Miriam Alonso- Tax Planning

![Cyprus Ltd vs UK Ltd [2026]: 5 Key Differences](https://cdn.sanity.io/images/glqahhks/production/e89433a9e5baf35b8c64e7bf69af332c4dce01c2-1679x937.jpg?w=700&q=75&auto=format)

Compare Cyprus Ltd vs UK Ltd: 15% vs 25% corp tax, 2.65% vs 39.35% dividend tax, and full EU access. Complete guide for British entrepreneurs in 2026.

Miriam Alonso- Company & Accounting