Moving from Finland to Cyprus

Quick Answer

Moving from Finland to Cyprus with Non-Dom status reduces your effective tax rate from ~38-46% to approximately 5%. Cyprus applies 0% Special Defence Contribution on foreign dividends, a flat 15% corporate tax, and offers tax residency with just 60 days of physical presence per year under the 60-day rule. A double tax treaty between Finland and Cyprus prevents double taxation during the transition.

Last updated: 2026-05-29

Why Finland Professionals Consider Cyprus

Finland combines high taxes with a dual income tax system that creates a complex burden for entrepreneurs. Earned income is taxed progressively at rates from 12.64% to 44% (combining state income tax at up to 31.25% and municipal tax at 7.5-10.5%). Capital income is taxed at a flat 30% up to EUR 30,000 and 34% above.

For entrepreneurs operating through an Oy (the Finnish limited company), the corporate tax rate is 20%. Dividend taxation depends on the company's net assets. Dividends from unlisted companies up to 8% of the company's mathematical value are classified as capital income, with 25% taxable (effective rate ~7.5%). Above that threshold, 85% of dividends are taxable as earned income, which can push the effective rate above 35%.

The YEL (self-employed pension insurance) system is mandatory for self-employed individuals and requires contributions based on declared earned income, typically 24-25% of declared income. This is in addition to income taxes.

Finland also taxes foreign-source income worldwide, and the tax authority (Vero) actively monitors international structures. The general anti-avoidance rule (VML 28) and CFC legislation can challenge arrangements that lack substance.

The cost of living in Helsinki is high by European standards, and the long, dark winters (with just 6 hours of daylight in December) push many internationally-minded professionals to seek warmer, more tax-friendly alternatives.

Finland Tax Burden at a Glance

| Tax type | 🇫🇮 Finland |

|---|---|

| Income tax | Up to 44% (state + municipal) |

| Corporate tax | 20% |

| Capital gains tax | 30-34% |

| Dividend tax | 25.5-28.9% effective (partial exemptions) |

| Social contributions | ~10% employee + ~20% employer (YEL for self-employed) |

| Effective rate | ~38-46% |

Tax Comparison: Finland vs Cyprus

The move from Finland to Cyprus delivers significant tax savings:

On EUR 100,000 of business revenue: Finland (Oy + salary/dividends): ~EUR 42,000 total tax (42% effective) Cyprus (Ltd + Non-Dom): ~EUR 5,000 total tax (5% effective)

Annual savings: approximately EUR 37,000

The savings become even more dramatic for higher earners. On EUR 200,000: Finland: ~EUR 92,000 (46% effective) Cyprus: ~EUR 10,000 (5% effective) Savings: EUR 82,000 per year

Additionally, Finnish entrepreneurs who are self-employed must pay YEL contributions of 24-25% on declared earned income. In Cyprus, social insurance contributions are capped at a much lower level and are based on a lower salary component.

There is no wealth tax in either country (Finland abolished its wealth tax in 2006), but the ongoing capital income tax savings in Cyprus are substantial.

Interactive Tax Calculator

Finland

Effective rate

42%

Est. tax: €42,000

Cyprus (Non-Dom)

Effective rate

5%

Est. tax: €5,000

Annual savings by moving to Cyprus

€37,000

Estimates based on effective rates. Consult a tax advisor for your specific situation.

Cyprus Non-Dom: ~5% effective tax

The alternative most entrepreneurs do not know about

- ✓15% corporate tax (flat, no surcharges)

- ✓0% dividend income tax (Non-Dom)

- ✓2.65% GHS on all income

- ✓No wealth tax, no inheritance tax

- ✓60-day rule for flexible tax residency

- ✓Full EU membership and treaty network

Double Tax Treaty: Finland - Cyprus

Finland and Cyprus have a double tax treaty in force since 2013 (replacing an older treaty). Key provisions: dividends 5% (if the beneficial owner holds at least 10% of capital) or 15% otherwise, interest 0%, royalties 0%. The treaty follows the OECD model and includes comprehensive anti-abuse provisions. Finnish pensions paid to Cyprus residents are taxable in both states, but Finland may not tax the pension at more than 15% under the treaty. Capital gains on shares are taxable only in the state of residence. The treaty includes an exchange of information clause, so transparency is maintained between the two countries.

Leaving Finland: Exit Process

Finland has specific rules regarding emigration and continued tax liability:

Three-year rule: Finland can maintain full tax liability for 3 years after emigration if you were a Finnish resident for at least 4 years during the 10 years preceding departure, unless you can demonstrate that you have no essential ties to Finland. "Essential ties" include a home available for your use, family remaining in Finland, or a business in Finland.

Deregistration: Notify the Digital and Population Data Services Agency (DVV) of your departure. This can be done online through the Muuttoilmoitus service.

Final tax return: File a Finnish tax return for the year of departure. Income earned in Finland during the year is taxable.

No formal exit tax: Finland does not impose an explicit exit tax on unrealized gains upon emigration. However, the 3-year rule effectively extends your tax liability.

YEL insurance: Your YEL obligation ends when you cease self-employment in Finland. Your accrued pension rights are preserved under EU coordination rules.

Kela benefits: Your entitlement to Kela (social insurance) benefits typically ends 1 year after departure from Finland if you are covered by the social security system of another EU country.

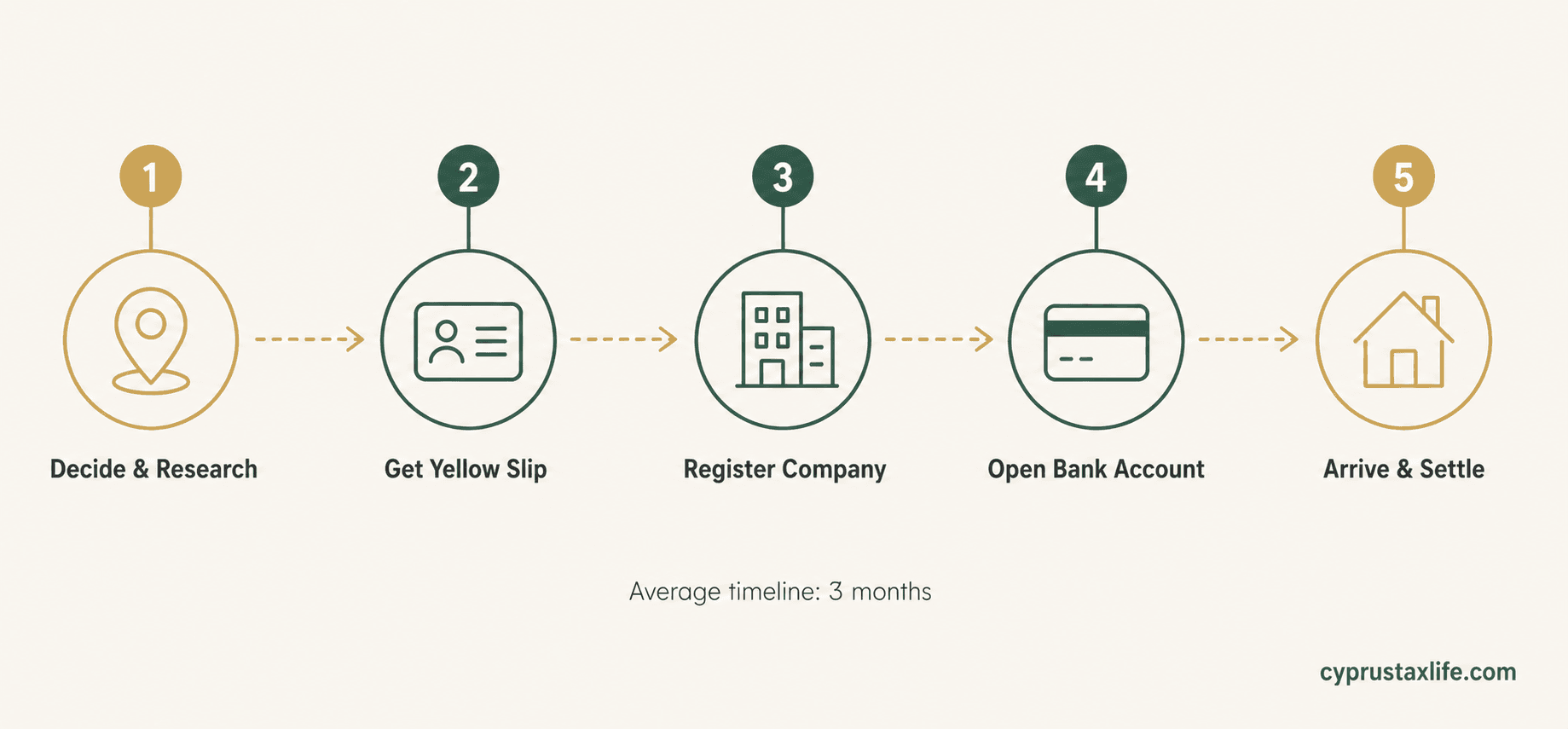

Timeline: Moving from Finland to Cyprus Month by Month

Month 0-1 (decision and planning): Consult a Finnish tax advisor (veroasiantuntija) to assess whether the 3-year rule will apply to you. If you have lived in Finland for at least 4 of the past 10 years, you are in scope. Identify and begin severing "essential ties": arrange the sale or arm's-length rental of your Finnish property, plan family relocation if applicable, begin winding down or restructuring Finnish business activities. Research Cyprus cities — Limassol is popular with Nordic expats, Larnaca is quieter and cheaper.

Month 1-2: Incorporate your Cyprus Ltd (5-7 working days once documents are submitted, total approximately EUR 2,100 in incorporation and registered office fees). Sign a rental contract in Cyprus. Open a Cyprus bank account — bring your EU passport, rental contract, company documents, and proof of source of income/funds. Notify DVV (Digital and Population Data Services Agency) of your move via the Muuttoilmoitus service online.

Month 2-3: Notify Vero Skatt (Finnish Tax Administration) of your new foreign address through the OmaVero portal. File any cessation notifications with YEL insurance provider (if self-employed). Apply for your Yellow Slip at the Cyprus Migration Department — you will need passport/EU ID, rental contract, proof of employment or sufficient means, and GHS health coverage or private insurance.

Month 3-4: Register for Cyprus tax residency at the Tax Department (bring TIC application, passport, rental contract). Apply for Non-Dom status simultaneously. Register for GHS healthcare. Set up your Cyprus Ltd payroll: low salary (below EUR 22,000 annual threshold) plus dividends. Begin living and working primarily from Cyprus.

Month 4-6: Ensure you have physically spent the majority of your time in Cyprus (more days in Cyprus than anywhere else). Keep records of all Cyprus presence: flight tickets, accommodation receipts, bank statements showing Cyprus activity. Your permanent home and center of vital interests must demonstrably be in Cyprus.

Year 1-3: File Finnish tax returns for each year during the 3-year rule period, asserting that essential ties have been severed. If Vero challenges, invoke the Finland-Cyprus double tax treaty Article 4 tie-breaker. Maintain documentary evidence of genuine Cyprus residence throughout. From year 4 onward, the Finnish extended tax liability period ends automatically.

Finnish Three-Year Rule: A Detailed Timeline and How to Break It Cleanly

Finland's three-year rule is one of the most important - and most misunderstood - aspects of Finnish tax exit planning. Under Finnish Income Tax Act section 11, a Finnish national or person who has been resident in Finland is considered to maintain full Finnish tax liability for three years after emigration, unless they can prove that no essential ties to Finland remain. This rule applies if you were resident in Finland for at least 4 of the 10 years preceding your departure.

What this means in practice is illustrated by a concrete timeline. If you leave Finland on 1 January 2026 and had lived in Finland for 4 or more of the preceding 10 years, Finland can assert tax jurisdiction over your worldwide income until 31 December 2028 - a full three years - unless you successfully demonstrate the absence of essential ties. From 1 January 2029, the extended liability period expires automatically, regardless of ties.

The key concept in the three-year rule is "essential ties" (olennainen side). Finnish tax law and Vero's practice identify three primary categories. First, a home available for your use in Finland: this includes not just a property you own but any property you can use freely, including one rented to family members at below-market rates or made available informally. The test is whether the property is functionally available to you. Renting your Finnish apartment or house to an unrelated third party at arm's length is the standard way to sever this tie. Second, close family remaining in Finland: if your spouse or minor children stay in Finland while you move to Cyprus, Vero will typically treat this as a persistent essential tie. The cleanest break involves the entire family relocating together. Third, active business operations in Finland: if you continue to manage or operate a Finnish company from Cyprus - even as a remote shareholder-director - Vero may treat the business connection as an essential tie.

Cases where taxpayers lost three-year rule disputes typically involve situations where one or more of these ties appeared formally severed but the practical reality was different. Examples include renting the Finnish apartment to a sibling at reduced rent (treated as still available for personal use), maintaining director roles in Finnish companies with active Finnish clients, or having minor children who remained in Finnish schools. In each category, Vero looks at the substance of the situation rather than the formal legal structure.

The Finland-Cyprus double tax treaty (in force since 2013) provides an important additional tool: the tie-breaker rules in Article 4. If both Finland and Cyprus assert tax residency during the three-year period, Article 4 requires the two states to apply a sequential test: permanent home, center of vital interests, habitual abode, and nationality. A taxpayer who maintains a genuine permanent home in Cyprus (rented or owned), whose center of vital interests is Cyprus (economic and personal activities), and who spends the majority of their time in Cyprus, can invoke the Article 4 tie-breaker to have Cyprus recognized as the sole state of residence for treaty purposes. This does not eliminate the Finnish three-year rule under domestic law, but it prevents double taxation by requiring Finland to exempt income that the treaty allocates to Cyprus. In practice, invoking the treaty tie-breaker requires active engagement with Vero and possibly a ruling request (ennakkoratkaisu). Professional Finnish tax counsel is essential for this process.

Cost of Living: Finland vs Cyprus

The cost of living comparison strongly favors Cyprus:

Housing: Helsinki EUR 1,200-1,800 vs Larnaca EUR 550-750 (savings: 50-60%) Groceries: Finland EUR 350-450 vs Cyprus EUR 250-350 (savings: 20-30%) Dining out: Finland EUR 250-350 vs Cyprus EUR 150-200 (savings: 40-45%) Transport: Finland EUR 80-120 vs Cyprus EUR 100-150 (comparable) Utilities: Finland EUR 150-250 vs Cyprus EUR 100-150 (less heating needed in Cyprus) Healthcare: Finland (Kela + municipal) vs Cyprus (2.65% GHS)

Total monthly: Finland EUR 2,300-3,200 vs Cyprus EUR 1,400-1,900

The climate difference is perhaps the biggest quality-of-life improvement. Finland receives approximately 1,800 hours of sunshine per year, while Cyprus gets over 3,400 hours. The long Finnish winter, with its impact on mental health and energy costs, is replaced by mild Mediterranean winters with temperatures rarely dropping below 10C.

Step-by-Step Relocation Checklist

Choose your Cyprus city and research housing options

Set up a Cyprus Ltd company

Find accommodation and sign a rental agreement

Notify DVV (Digital and Population Data Services Agency) of your move

File your final Finnish tax return with Vero

End YEL insurance (if self-employed)

Apply for Cyprus tax residency

Register for Non-Dom status

Obtain your Yellow Slip

Open a Cyprus bank account

Register for GHS healthcare

Set up payroll (low salary + dividends)

Inform Finnish banks of new tax residency

Consider maintaining voluntary Kela membership for the first year

Frequently Asked Questions

Does Finland have an exit tax?+

What happens to my Finnish pension (YEL, TyEL)?+

Can I keep my Finnish Oy after moving?+

How does Finnish CFC legislation affect a Cyprus company?+

What about healthcare in Cyprus compared to Finland?+

Is there a Finnish community in Cyprus?+

How does the Finnish YEL pension insurance affect my pension situation in Cyprus?+

Do Finnish CFC rules apply if my Finnish Oy remains active after I move to Cyprus?+

How do I correctly notify Vero of my change of tax residency when moving to Cyprus?+

Sources and References

- PwC Worldwide Tax Summaries — Cyprus

- KPMG Cyprus — Tax and Advisory

- EY Cyprus — Tax Services

- Cyprus Ministry of Finance (mof.gov.cy)

Effective rates are approximations for entrepreneur structures (company + low salary + dividends). Consult a qualified tax advisor before making decisions.

Free, no commitment

Does this apply to your situation?

Tell us your situation and we'll connect you with our specialist expat advisory firm in Cyprus. They have years of experience managing relocations like yours.

Related Articles

![Best Holding Company [2026]: Cyprus vs 4 Rivals](https://cdn.sanity.io/images/glqahhks/production/9ec5328706d63fc458c40c9b2e7d80c38816e68f-1678x937.jpg?w=700&q=75&auto=format)

Compare Cyprus, Luxembourg, Netherlands and Malta as holding jurisdictions. Cyprus: 3% effective on dividends, 0% CGT, under EUR 7,000/year to maintain.

Miriam Alonso

Miriam Alonso- Company & Accounting

![Cyprus Withholding Tax on Dividends [2026]: 0% Guide](https://cdn.sanity.io/images/glqahhks/production/d06fdbecc2a60a7a2c152fdeaa9dc27d4c596810-1679x937.jpg?w=700&q=75&auto=format)

Learn why Cyprus charges 0% withholding on dividends to non-residents. SDC at 5% applies only to Cyprus-domiciled recipients. Includes treaty rates table.

Miriam Alonso- Tax Planning

![Cyprus Ltd vs UK Ltd [2026]: 5 Key Differences](https://cdn.sanity.io/images/glqahhks/production/e89433a9e5baf35b8c64e7bf69af332c4dce01c2-1679x937.jpg?w=700&q=75&auto=format)

Compare Cyprus Ltd vs UK Ltd: 15% vs 25% corp tax, 2.65% vs 39.35% dividend tax, and full EU access. Complete guide for British entrepreneurs in 2026.

Miriam Alonso- Company & Accounting